Cheche Group Advances SaaS and Insurance Platforms En Route to Break-Even

Cheche Group’s latest quarterly results reveal significant progress toward profitability by leveraging its core insurance transaction services and scalable SaaS solutions amidst evolving market and regulatory dynamics in China.

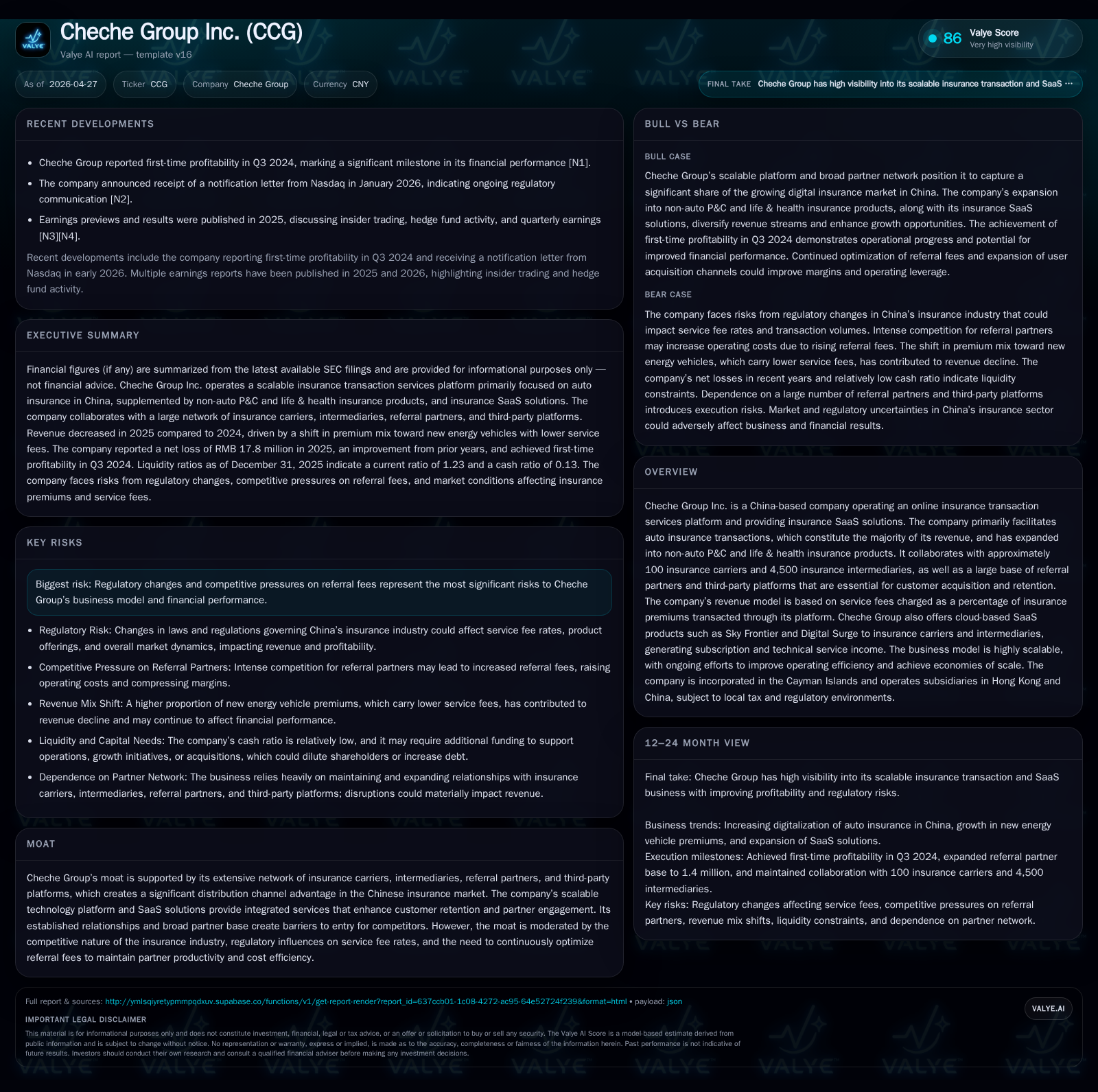

In the latest quarter ending early 2026, Cheche Group reported a historic narrowing of net losses and improving operating leverage, driven by calibrated marketing expenses and enhanced platform efficiencies. The company’s dual revenue streams—from auto-focused insurance transaction fees and growing SaaS offerings—capitalize on China’s expanding automobile ownership and digital insurance penetration. Despite regulatory limits on service fee rates and competitive pressures on referral fees, Cheche’s broad ecosystem of insurers, intermediaries, and referral partners creates a defensible distribution moat. Going forward, execution milestones include deepening SaaS adoption among carriers and intermediaries, optimizing referral fees, and navigating regulatory shifts.

Latest Quarterly Operating Update Highlights Profitability Trajectory

Cheche Group’s most recent quarterly disclosures culminating in its FY2025 annual report showcase pronounced operational advancement on the path to profitability. The company posted a net loss of RMB17.8 million in 2025 compared to RMB61.2 million in the prior year—a nearly threefold reduction—reflecting improved operational efficiency and tighter cost controls [S3][F1]. This marks an inflection point following years of steep losses amid initial investment into platform infrastructure and user acquisition.

Gross profit marginally grew to RMB160 million (5.3% gross margin), reflecting a strategic shift to higher-margin new energy vehicle (NEV) insurance premiums despite overall revenue contraction from RMB3.47 billion in 2024 to RMB3 billion in 2025 [S4][F1]. Marketing spend decreased by approximately 14%, accompanied by lower share-based compensation expenses integral to R&D and administrative costs, signaling disciplined expense management.[S3]

Interest expense also declined significantly by over 40%, aided by partial debt repayment which moderated financial charges [S3]. Collectively these factors underpin a leaner cost structure enabling gains in operating leverage as Cheche pursues break-even.

Core Business Model: Insurance Transactions Meet SaaS Solutions

Cheche earns the majority of its revenue through transaction service fees assessed as a fixed percentage of insurance premiums processed predominantly on its digital platform [S1][F1]. Auto insurance transactions represent more than 99% of this revenue stream with auto owners mandated by Chinese regulations to purchase statutory liability coverage annually—ensuring recurring volume inflows [S1]. Leveraging an extensive ecosystem connecting approximately 100 insurance carriers with over 4,500 intermediaries plus thousands of third-party platform partners creates robust network effects that facilitate both customer acquisition and retention.

Complementing transaction fees is the company’s growing SaaS business offering cloud-based solutions (notably Sky Frontier and Digital Surge) that provide carriers and intermediaries with digital tools enhancing underwriting, policy management, and distribution capabilities [S16]. These subscription-based revenues contribute incremental income while deepening customer stickiness through integration within insurer operations.

This dual-revenue model embodies scalability: transaction volumes drive service fee income that scales with premium growth while SaaS subscriptions yield recurring fees aligned with customer base expansion. The mix is gradually shifting as SaaS adoption expands but remains small relative to transaction fees today.

Market Positioning Within China’s Digital Insurance Ecosystem

Cheche occupies a strategic position at the nexus of China’s fast-evolving digital insurance market where distribution reach plus integrated technology capability determine success barriers. Its vast partner network spanning insurers and intermediaries forms a formidable distribution moat that is hard for new entrants to replicate quickly given entrenched relationships critical for policy sales flows [S1].

The company's technology stack underpins seamless interface for multi-product insurance transactions including embedded offerings co-developed with carrier partners fostering innovation tailored for Chinese customers’ evolving preferences especially towards NEVs [S1]. By integrating technology directly into carrier workflows via its SaaS tools, Cheche strengthens switching costs that enhance partner retention.

While competitors exist within China’s insurance tech sector, Cheche’s combination of extensive channel breadth plus proprietary cloud solutions provides differentiated value versus stand-alone software or fragmented platforms. However, regulatory constraints limiting allowable service fee percentages create commercial tension necessitating continuous operational efficiency optimization.

Drivers Behind Growth: Auto Insurance, Non-Auto Expansion, and Digitalization

China’s auto market growth remains robust—projected vehicle sales climbing from approximately 26 million units in 2021 to roughly 33 million by 2026—fueled notably by government incentives promoting NEV adoption [S1]. Statutory liability requirements ensure persistent demand for auto insurance renewal cycles providing steady premium flows that Cheche facilitates digitally.

Digital penetration in auto insurance underwriting and sales processes has escalated rapidly from around 10% industry penetration in 2018 to expected levels approaching 73% by 2026 for digital transactions [S1], underscoring structural secular tailwinds favoring Cheche’s platform offerings.

Beyond auto lines, expansion into non-auto Property & Casualty (P&C) including life & health products enlarges addressable markets substantially—the non-auto premium pool is forecasted to grow at over 9% CAGR reaching RMB5.8 trillion by 2026 [S1]. Cheche leverages its referral partner ecosystem to cross-sell diversified products while tailoring SaaS modules suited for these segments' operational nuances.

Challenges and Risks: Regulatory Pressures and Competitive Fee Dynamics

The sustainability of Cheche's unit economics increasingly hinges on navigating regulatory ceilings imposed on service fee rates charged to insurers which can compress margins if premiums shift disproportionately toward lower-fee NEV policies [S1]. Additionally, substantial referral fees paid out to partners constitute the largest cost bucket requiring ongoing optimization amid intense competition for customer attention across digital platforms.

Management highlights initiatives focusing on broadening acquisition channels beyond traditional referrals to collaboration with high-influence third-party platforms aimed at improved conversion efficiency per marketing yuan spent [S13]. Simultaneously balancing incentives between referral partners without escalating costs remains critical.

Cybersecurity risk mitigation is addressed via a board-level governance framework actively overseeing evolving threats aligned with industry best practices—an essential underpinning fostering trust among partners handling sensitive customer data [S1].

Key Metrics and Financial Snapshot: Navigating Toward Positive Earnings

At year-end 2025, Cheche held RMB144.5 million in cash versus total debt approximating RMB90.3 million resulting in estimated net cash status supportive of near-term liquidity needs amidst ongoing investments [F1].

Revenue contraction reflected deliberate repositioning toward NEV-heavy segments but was partly offset by improved gross margin uptrend from cost efficiencies realized across channel-related expenses and tighter overhead control [F1][S4]. Operating losses narrowed substantially facilitated by R&D expense reductions exceeding one-third year-over-year largely attributable to non-cash share-based compensation adjustments alongside realigned personnel costs [S3].

These financial dynamics demonstrate maturation effects where scale economies begin offsetting fixed cost bases particularly as SaaS subscription revenues scale amortizing technical service platform costs more effectively [S16].

Milestones to Monitor: Customer Acquisition, Technology Adoption, and Margin Improvements

Future performance hinges on multiple execution vectors including:

- Accelerating adoption of SaaS offerings among both insurer and intermediary customers through targeted marketing campaigns aiming at upselling existing relationships while attracting new clients.

- Refining referral fee structures ensuring competitive yet sustainable cost ratios enabling scalable user acquisition without margin erosion.

- Tracking expansion into non-auto P&C product transactions improving top-line diversity reducing concentration risk tied predominantly to auto lines.

- Continued improvement in operating leverage illustrated through declining R&D intensity (% of revenues) and tighter general/admin expense containment post-share-based comp normalization.

- Regulatory landscape vigilance relating to potential changes affecting permissible service fee ceilings or assessment bases which could materially impact economics.

- Cybersecurity incident reporting metrics maintaining zero breaches or rapid resolution times preserving platform integrity essential for partner confidence.

KPIs spotlighted by management such as transaction volume growth per segment along with incremental SaaS monthly recurring revenue will be key gauges assessing momentum sustainability across core business pillars.

This analysis synthesizes Cheche Group Inc.’s latest SEC filings up to April 27, 2026 considering operational updates through early April quarters supported by validated financial metrics without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments