One & one Green Technologies Expands Recycling Footprint with Robust 2025 Growth

The company’s latest filings reveal significant revenue and net income growth driven by proprietary eco-efficient technology, regulatory licensing, and strategic expansion efforts.

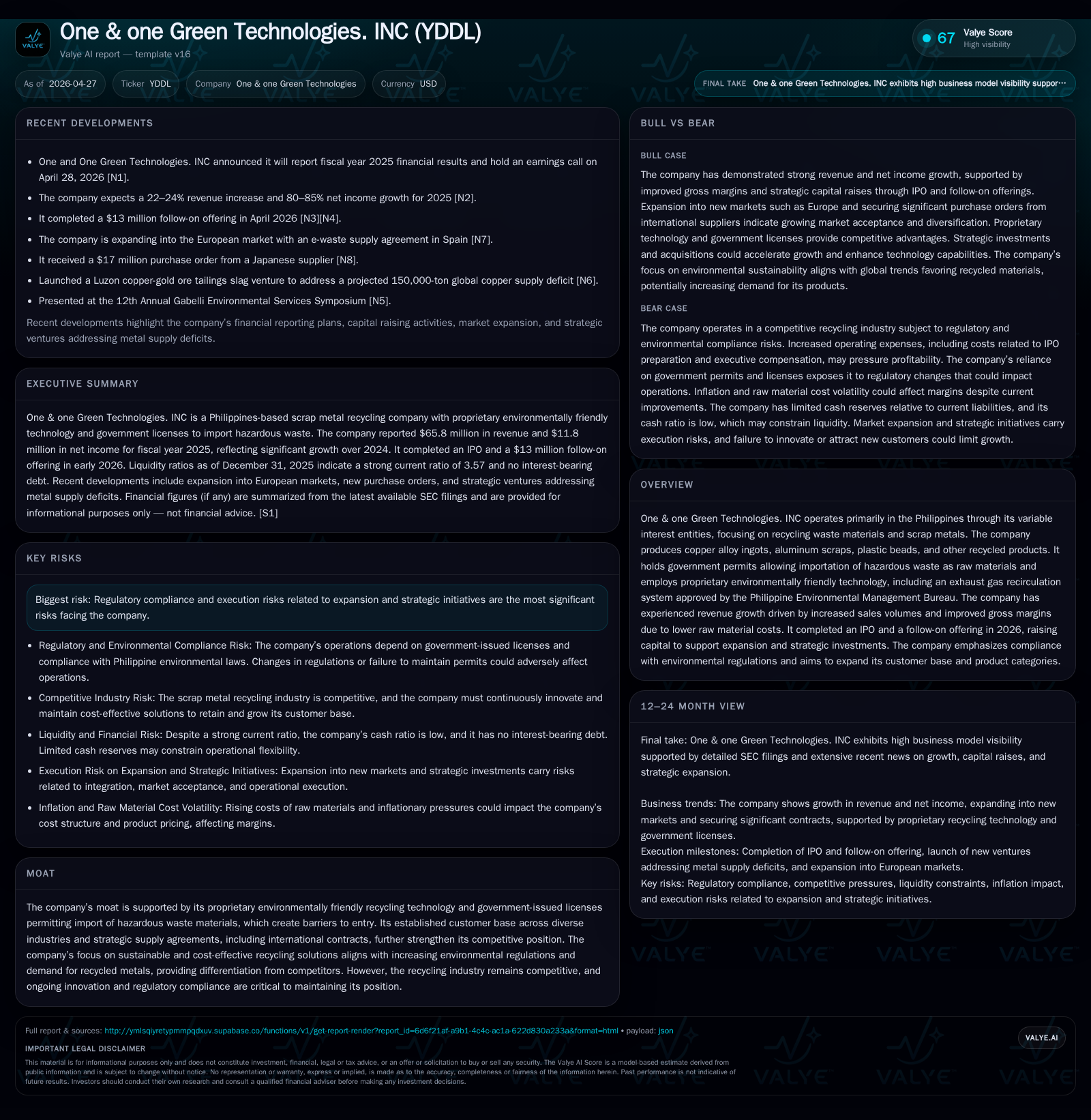

One & one Green Technologies posted a substantial 23% revenue increase and an over 80% rise in net income for fiscal year 2025, as disclosed in recent SEC filings. The company’s business model leverages government permits to import hazardous waste and proprietary environmentally friendly recycling technology, granting notable competitive advantages. Positioned within Southeast Asia’s growing metal recycling market, One & one is focusing on geographic expansion and secure raw material sourcing to sustain growth amid inflationary and regulatory pressures. Upcoming investor milestones include the April 28 earnings call that should shed further light on operational momentum.

Latest Quarterly Operating Update: Strong Growth and Confirmed Guidance

One & one Green Technologies’ most recent SEC disclosures via their two April 6-K filings ([S2], [S3]) set the tone for a year of pronounced expansion in fiscal 2025. The announcement on April 15 projected revenue growth between 22% to 24%, alongside an even more impressive net income surge of approximately 80–85%. These projections were anchored on actual revenue reaching $65.8 million for FY2025, representing a robust 23.1% increase compared to $53.5 million in FY2024 [S10]. Net income nearly doubled from $6.48 million in FY2024 to $11.8 million in FY2025 [S20]. The company also confirmed an upcoming earnings call on April 28 to discuss these results in detail [S2], marking an important event for investors and stakeholders to assess ongoing momentum.

This growth is supported by operational leverage gained through expanded processing capacity, optimized product mix shifting towards higher-margin copper ingots, and improved gross margins—rising from 19.77% in FY2024 to nearly 24% in FY2025 due primarily to lower raw material input costs [S10]. Additionally, selling expenses decreased slightly due to shipment mix changes, while general & administrative expenses rose moderately from IPO-related costs and staffing investments signaling readiness for scaling [S10].

Concurrent with these financial gains, One & one completed a significant $13 million follow-on equity offering early in April 2026 [N3], reinforcing its financial flexibility without incurring interest-bearing debt ([S4]). This capital infusion is earmarked for expanding production facilities, technological upgrades, and strategic acquisitions within the metal recycling ecosystem.

Business Model: Economical, Environmentally Focused Recycling Solutions

Operating primarily through its variable interest entities (VIEs) Yoda Metal and DL Metal based in the Philippines, One & one Green Technologies focuses on sustainable recycling of electronic waste, scrap metals, and industrial residues to produce copper alloy ingots, aluminum scraps, plastic beads, among other recyclable materials [S1]. The firm benefits from an annually reviewed government license that uniquely authorizes it to import hazardous waste under Basel Convention guidelines—an often challenging regulatory barrier restricting competition.

The company emphasizes economizing waste processing through proprietary technologies targeting process efficiency improvement coupled with pollution reduction. Key among these is their patented exhaust gas recirculation system that captures emissions ash and slag for secondary metal recovery before emission release—meeting stringent standards set by the Philippine Environmental Management Bureau (EMB) [S1]. This eco-efficient system contrasts with conventional table concentrators used by competitors which allow pollution during final processing stages.

Such technological innovations underpin a value proposition that not only reduces environmental impact but also improves yield recovery rates while lowering operating costs—balancing eco-consciousness with profitability critical for sustainability-focused customers across manufacturing sectors such as casting foundries, automotive parts makers, and heavy equipment manufacturers [S1], [S6].

Proprietary Technology and Compliance as Competitive Moats

One & one’s proprietary recycling technology suite effectively functions as a moat. Its exhaust gas recirculation technology is validated annually by Philippine regulators ensuring compliance with emissions standards—a critical credential increasingly demanded globally as governments stiffen environmental regulation [S1].

Equally important is the company’s fully authorized government permit system enabling hazardous waste import which is essential given local scrap supply limitations relative to processing capacity. Compliance compliance extends across comprehensive environmental clearances including ECCs (environmental compliance certificates), discharge permits, as well as export/import permits underscoring regulatory discipline necessary for long-term operation stability [S1].

This dual advantage of licensed hazardous material access plus superior eco-friendly recycling tech restricts new entrants substantially since replicating such licenses requires navigating complex international agreements (Basel Convention) and extensive governmental scrutiny while developing similar technology demands significant R&D investment.

Industry Context: Competitive Pressures and Regulatory Trends in Southeast Asia

The Southeast Asian scrap metal recycling industry is fragmented yet competitive with many local players lacking the sophisticated technological capabilities or legal permissions enjoyed by One & one Green Technologies. Commodity pricing volatility heavily influences margins given metal inputs are price sensitive; however recent raw material cost reductions contributed favorably to the company's margin expansion in FY2025 [S10].

Moreover, regional governments have been progressively tightening environmental rules spurred by global climate agendas which favor certified sustainable recycling operators able to demonstrate pollutant containment—traits aligning well with One & one's documented processes. This regulatory trend acts as both an enabler by limiting non-compliant competitors while imposing execution discipline requiring ongoing capital reinvestment into cleaner technologies.

Growth Catalysts: Geographic Expansion and Raw Material Sourcing

Reflecting its long-term ambition stated in the latest Annual Report ([S1]), One & one aims to expand beyond national borders into broader Southeast Asian markets supported by securing stable raw material supplies primarily from Japan and Korea—markets known for stringent e-waste handling regulations creating outbound flows of recyclable metals. The company is building an international business development team skilled in multiple languages to enhance cross-border sales operations covering Europe, America, and Asia regions [N7], [N8].

Operational KPIs likely linked directly include processing tonnage growth beyond its estimated annual capacity of approximately 300,000 tons alongside increasing penetration into new geographies characterized by rising industrialization thus elevating demand for recycled metal feedstocks [S1]. Diversifying into adjacent product categories such as e-waste stream recovery services marks additional growth avenues targeting Metro Manila’s billion-dollar market segment recently secured via strategic supply partnerships [N8].

Operational Risks: Regulatory Compliance and Execution Challenges

Key risks remain evident particularly around maintaining compliance amid evolving environmental regulations potentially impacting operating cost structures or permitted activity scopes in the Philippines—a country historically prone to political instability that could affect day-to-day operations or longer-term policy certainty [S1]. Inflationary trends threaten margin stability through upward pressure on labor, energy costs while potentially eroding purchasing power testing pricing power resilience [S1], [S8].

The execution risk dimension concerns scaling operations geographically while preserving customer service quality; entering new jurisdictions demands understanding diverse regulatory regimes plus establishing local supplier networks without diluting efficiency gains acquired domestically. Failure to innovate or maintain technology leadership may also weaken positioning versus emerging competitors investing in green technologies.

Upcoming Milestones and Investor Considerations

Investors should focus closely on the scheduled earnings call set for April 28, 2026 ([S2], [N1]) which will offer management commentary on full-year final results including realized pricing vs forecasts along with updated guidance reflecting macroeconomic factors or expansion progress. Monitoring backlog buildup or bookings from new geographic markets will provide early indication if strategic ambitions translate into tangible revenue streams.

Additionally, watch for potential announcements regarding selective acquisitions or investments hinted at aimed at further improving technology capabilities or capturing market share within Asia’s recycling sector—these could drive accelerated scale economies or broaden product portfolios per company statements ([S6], [S23]).

Financial Position and Capital Deployment Strategy

The company maintains a conservative capital structure devoid of interest-bearing debt providing a clean financial runway ([F1], [S4]). Cash holdings stood at roughly $0.96 million as of December 31, 2025 coupled with a strong current ratio of approximately 3.57 indicating healthy near-term liquidity ([F1]). Operating cash flow showed volatility due mainly to working capital changes but overall supports ongoing operations without strained funding needs ([S21]).

Capital expenditures totaled $0.7 million in FY2025 emphasizing asset acquisition aligned with capacity expansion plans ([S4]). Equity capital raised through IPO followed by a $13 million follow-on offering has been designated primarily toward boosting plant capacity upgrades as well as augmenting research capabilities enhancing product recovery yields ([N3], [N4]). This prudent deployment reflects management’s balanced approach toward growth investment while controlling operational leverage.

Disclaimer: This analysis is based exclusively on publicly available SEC filings dated through April 27, 2026 and associated news disclosures without any non-public information or forward-looking investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments