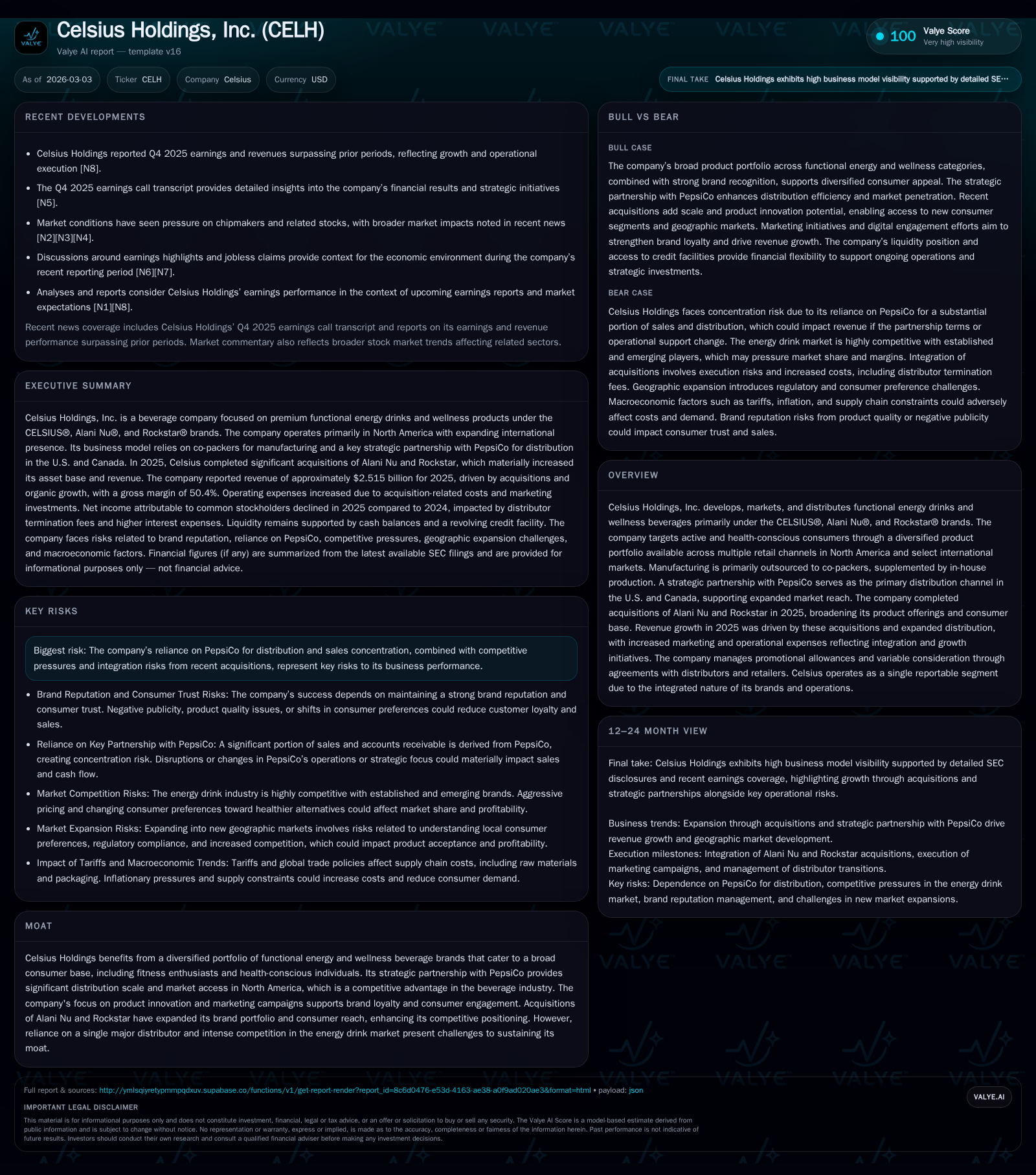

Celsius Holdings Expands Portfolio and Market Reach with Strategic Acquisitions and PepsiCo Partnership

Acquisitions of Alani Nu and Rockstar in 2025 alongside a deepened PepsiCo alliance underpin Celsius Holdings' growth trajectory and operational dynamics.

Celsius Holdings, Inc. has achieved rapid revenue growth driven by the 2025 acquisitions of Alani Nu and Rockstar brands, significantly broadening its consumer base and product portfolio in the functional energy drink market. The company leverages a close strategic distribution partnership with PepsiCo, which expands its North American footprint but concentrates risk around this single major channel. While operating income declined slightly year-over-year reflecting integration costs and elevated marketing expenses, strong cash flow generation supports ongoing investments and capital returns. Key risks include competitive pressures, reliance on PepsiCo’s distribution, and complexities integrating acquisitions.

Historical Performance and Growth Drivers

Celsius Holdings has demonstrated striking top-line growth over recent years, evolving from niche functional beverage maker into a multi-brand portfolio operator leveraging acquisitions and strategic partnerships. Revenue surged from $130.7 million in FY2020 to approximately $654 million in FY2022 — a nearly fivefold increase over two years — driven primarily by organic brand momentum of CELSIUS® as well as expanded retail penetration [F1]. This growth accelerated further with record revenue of over $1.3 billion reported for FY2023, representing a doubling from the prior year.

Operating income mirrored this trajectory but showed volatility reflective of investments and scaling challenges. Following an operating loss of approximately $158 million in FY2022 linked to expansion investments, the company swung to a strong operating profit of $266 million in FY2023 [F1]. However, operating income declined modestly to $141 million in FY2025 despite integration of accretive acquisitions. This suggests increased expenses related to business combination costs, elevated sales & marketing outlays including campaigns for newly acquired brands Alani Nu and Rockstar, as well as amortization and administrative costs.

Net income similarly recovered from losses reported through fiscal 2022 into substantial profitability; net income peaked at roughly $227 million in FY2023 before normalizing at $108 million in FY2025 [F1]. The decline reflects one-time financial effects alongside continued reinvestment behind growth efforts.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 108 | 359 | 141 | -25.6% | ||

| 2024 | 145 | 263 | 156 | -36.0% | ||

| 2023 | 1318 | 227 | 141 | 266 | +101.7% | +221.1% |

| 2022 | 654 | -187 | 108 | -158 | +108.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 6 | 323 | 9.1 |

| 2024 | 2 | 240 | 36.3 |

| 2023 | 124 | 85.9 | |

| 2022 | 100 | -467.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not explicitly available for FY2024-25; focus is on operating metrics excerpted from filings [F1]

Cash flow from operations expanded strongly amid the growing revenue base despite increased working capital demands related to acquisition integrations and receivable build-up. Capital expenditures jumped over 50% year-over-year in FY2025 as Celsius invested more heavily in owned manufacturing assets alongside reliance on co-packers [F1]. Share repurchases resumed with modest buybacks amounting to nearly $6 million executed during the year against an authorized program worth up to $300 million as of late 2025 [S5].

Future Growth Prospects

Growth going forward is closely tied to leveraging recently acquired brands Alani Nu and Rockstar that combined broaden Celsius’ consumer target segments beyond the core CELSIUS brand's active lifestyle focus into wellness supplements and traditional energy drink consumers respectively [S1]. Both brands have existing loyal customer bases — notably Alani Nu resonates strongly with Gen Z demographics especially females — offering immediate opportunities for cross-selling, product innovation, and expanded retail footprint.

The strategic alliance with PepsiCo forms another cornerstone of future expansion plans given its vast North American distribution infrastructure and expertise. This partnership was deepened substantially accompanying the acquisitions closed during FY2025 providing streamlined logistics, enhanced shelf presence across channels like grocery stores, mass merchandisers, convenience outlets, fitness centers, and e-commerce platforms [S1].

Product innovation is expected to remain a key driver as Celsius continues rolling out new formulations such as the non-caffeinated CELSIUS Hydration powders launched recently emphasizing sugar-free electrolyte solutions for health-conscious consumers [S1]. The company’s mix of ready-to-drink beverages and on-the-go powders supports broader consumption occasions.

International market penetration remains incremental but holds potential notably across Europe, Middle East, Asia-Pacific regions where selective launches continue under all three brands though these markets still comprise relatively small shares [S1].

Risks tempering growth include heavy dependency on PepsiCo whose decisions can materially influence order volumes; fluctuations in this single distributor’s inventory management could impact sales abruptly [S25]. Additionally, effective integration of acquisitions amid heightened competition particularly from other energy drink giants such as Monster Beverage requires sustained marketing effectiveness and operational excellence.

Forecasts / Milestones / Expectations

While official guidance or forward-looking financial targets were not publicly disclosed for post-FY2025 periods within the sourced filings or earnings transcripts [N3], key indicators to monitor include:

- Sales ramp-up velocity for Alani Nu and Rockstar relative to original acquisition case assumptions,

- Synergies realization pace including estimated distributor termination fees recognized during transition,

- Continued gross margin trends post-integration,

- Evolution of dependence on PepsiCo’s network balancing potential diversification opportunities,

- Progress on new product launches especially wellness-focused innovations. Considering the aforementioned factors along with healthy operating cash flows suggests planned reinvestments will persist while managing cost discipline to drive incremental bottom-line improvements.

Returns / Capital Allocation

Based on latest findings:

- Return on equity stood near an estimated ~9.1% based on net income relative to shareholder equity positioning following large equity issuance connected to acquisitive activity [F1].

- Cash flows from operations grew strongly from $263 million in FY2024 to $359 million in FY2025 supporting sizeable free cash flow after capital spending totaling around $36 million within the same period [F1].

- Share repurchases have recommenced following paused activity during more aggressive investment years; approximately $6 million deployed versus authorizations enabling up to $300 million illustrates measured capital return approach aimed at balancing growth funding needs against shareholder value enhancement [S9][F1].

- No dividend payments were reported; management appears focused on accelerating scale via reinvestment.

Debt refinancings took place during mid-to-late 2025 lowering interest rate margins modestly while extending maturities with a sizable term loan balance around $700 million secured against company assets reflecting substantial leverage related partially to acquisition funding [S6][S10]. Liquidity remains ample with cash & equivalents approximating $399 million as year-end coupled with undrawn revolving credit facilities signaling no imminent refinancing concerns [S18][F1].

Industry Positioning and Risks

Celsius’s differentiated product portfolio spanning active lifestyle-focused energy drinks alongside wellness-oriented nutritionals plus mainstream Rockstar Energy products provides exposure across overlapping markets within the crowded energy beverage category. The company relies heavily on innovative formulations emphasizing better-for-you attributes like zero sugar, natural ingredients, amino acids enrichment, hydration properties which align well with evolving consumer preferences toward health consciousness while sustaining performance appeal [S1].

The distribution agreement with PepsiCo anchors many advantages including access to an entrenched national distribution network capable of delivering scale while mitigating logistical complexities typical for mid-sized branded beverage companies. However, this arrangement amplifies concentration risk; any strategic retrenchment or operational shift by Pepsi could disrupt Celsius’s sale cycle or cash conversion timing noticeably given over half of receivables stem from this partnership [S19][S25].

Competitive pressures stem from both entrenched global multinationals like Red Bull and Monster Beverage plus nimble emerging entrants targeting niche wellness segments or regional markets with novel blends or natural ingredient emphasis requiring continuous consumer engagement through marketing innovation especially on social media platforms favored by younger demographics.

Regulatory scrutiny exists around claims related to health effects of caffeinated energy drinks alongside growing litigations including derivative lawsuits centered on alleged disclosures about distribution agreements—settlements agreed upon recently aim to limit prolonged legal distractions but require ongoing governance vigilance [S14][S15][S24].

Supply chain optimization remains crucial since outsourced manufacturing via co-packers supports flexible scaling but necessitates stringent quality controls complemented by owned facility investments enabling rapid responsiveness under volatile demand scenarios.

Final Observations

Celsius Holdings stands at a pivotal stage transitioning from high-growth standalone brand status into diversified multi-brand beverage player backed by a powerhouse distributor partner. Execution success will depend on synergistic management of recent acquisitions combined with maintaining brand cachet amid escalating sector choices faced by consumers prioritizing health benefits alongside energy needs. Robust cash flow generation projects financial flexibility while measured share buybacks indicate commitment toward shareholder value balancing growth imperatives. Nonetheless, reliance on a few significant partners introduces sensitivity toward external operational decisions requiring proactive risk mitigation strategies behind supply chain resilience plus market innovation agility. Stakeholders should monitor key performance indicators emanating from new brand integrations alongside evolving competitive dynamics shaping fundaments underpinning future revenue momentum.

This report is prepared solely for informational purposes based on publicly available data including SEC filings dated up to March 3, 2026 without solicitation or recommendation regarding investments. It does not constitute investment advice or endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments