Canopy Growth Confronts Financial Controls and Compliance as Growth Strategy Evolves

The company addresses material financial restatements and internal control weaknesses while advancing growth initiatives amid regulatory challenges.

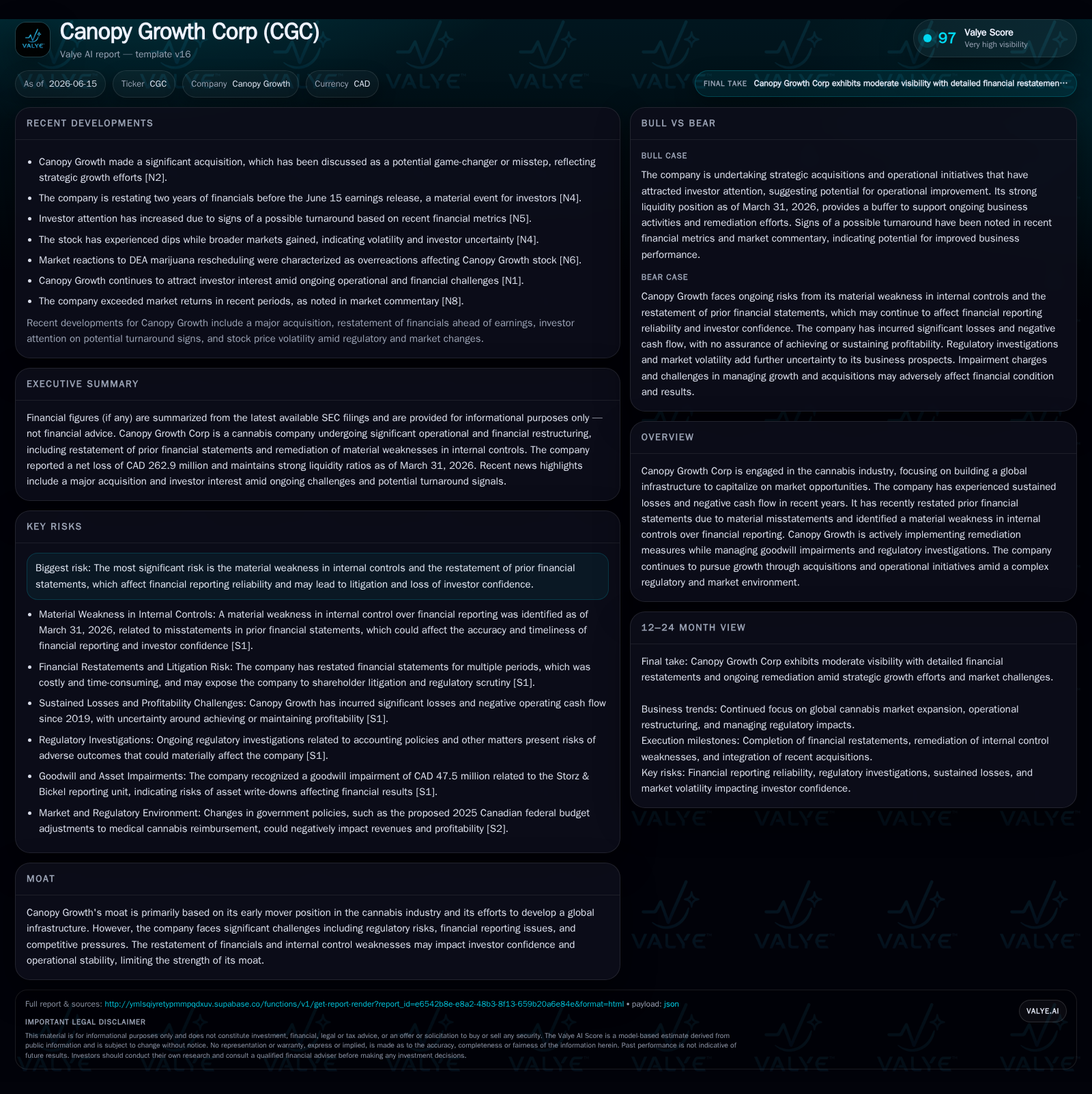

Canopy Growth Corp's June 15, 2026 8-K filing reveals a significant restatement of prior financial statements caused by material misstatements and a disclosed material weakness in internal controls over financial reporting. The remediation process is underway but has incurred notable costs, weighed down by ongoing litigation risk and impaired investor confidence. Operationally, Canopy continues to pursue growth through acquisitions, expanded cultivation capacity, and product diversification within medical and recreational cannabis segments, although reimbursement rate pressures and regulatory compliance remain key constraints. The latest quarter reflects sustained losses against a solid liquidity buffer, positioning the company to support remediation efforts while navigating competitive sector dynamics.

Recent Operating Update: Restatements and Internal Controls Impact

On June 15, 2026, Canopy Growth Corp filed an 8-K [S3] disclosing a significant restatement of its previously issued audited consolidated financial statements for fiscal years ended March 31, 2024 and 2025 along with interim quarters dating back to September 30, 2023 [S1]. This restatement stems from material misstatements tied to deficiencies in internal controls over financial reporting. The company acknowledged a material weakness in these controls which remains under active remediation via recommended actions detailed in the annual report [S1].

The restatement process has been both time-consuming and costly, resulting in substantial unexpected audit fees, legal expenses related to defending against putative class action lawsuits initiated between May and July 2023 alleging disclosure misrepresentations [S14][S20]. The reputational damage attached to these governance shortcomings poses ongoing risks to investor confidence and supplier or counterparty relationships [S1], complicating Canopy’s operational stability even as it attempts execution on growth strategies.

Business Model Outline: Licensed Producer Platform in Medical and Recreational Cannabis

Canopy operates primarily as a licensed producer within the cannabis industry value chain that spans cultivation facilities management, product processing - including dried flower, edibles, vaporizer devices - wholesale distribution channels supplying retail dispensaries, and selective direct-to-consumer engagement [S1]. Revenue generation is predominantly from bulk wholesale sales complemented by medical cannabis offerings subject to government reimbursement policies.

The company’s product portfolio targets both recreational cannabis users seeking diversified consumables such as edibles alongside medical patient populations whose prescriptions are historically supported via federal or provincial health plan reimbursements [S1]. These reimbursements are increasingly uncertain: proposals under Canada’s 2025 federal budget seek to reduce payment rates from $8.50 per gram to $6.00 per gram for specific government clients like the RCMP and veterans [S2]. Such downward pressure on reimbursement rates threatens medical segment revenue stability and compresses gross margin percentages.

Regulatory compliance constraints limit marketing aggressiveness especially in Canada where advertising remains tightly controlled by Health Canada regulations [S5]. The stringent regulatory backdrop shapes how Canopy prioritizes investments into cultivation capacity utilization increases and cautious expansion of product lines within allowable frameworks.

Industry Structure: Competitive Dynamics in North American Cannabis Markets

Within North America’s legal cannabis landscape, Canopy Growth faces competition from well-capitalized licensed producers that operate at scale or niche specialization levels. Aurora Cannabis serves as a comparison for extensive cultivation facilities enabling volume leadership across multiple jurisdictions. Tilray Brands exemplifies broad international distribution capabilities coupled with robust medical cannabis R&D initiatives. Curaleaf Holdings reflects strengths in extensive retail dispensary networks enhancing consumer access points.

Market pressures also arise from illicit operators who distort local pricing power but remain outside formal compliance structures. Such dynamics result in fluctuating sales volumes affecting production planning KPIs like cultivation output (kg produced) and inventory turnover rates that directly impact cash conversion cycles.

Growth Drivers: Acquisitions, Market Expansion, and Product Innovation

To offset inherent sector headwinds from regulation and cost pressures, Canopy Growth continues executing strategic acquisitions designed to increase geographic footprint reach as well as enhance its product innovation pipeline spanning recreational edibles formulations to advanced vaporizer devices targeting wellness markets [N4][S1].

These M&A activities signal a deliberate attempt to capture market share through inorganic growth avenues while incremental improvements in cultivation efficiency aim to boost gross margin percentages. However, integration complexity creates execution risk which management acknowledges could divert resources or delay expected synergies [S11]. New legalization developments across Canadian provinces or select U.S. states provide additional demand catalysts supporting these expansion endeavors.

Risks and Constraints: Regulatory Compliance, Financial Reporting, and Margin Pressures

Core risks entail ongoing regulatory compliance challenges that can potentially lead to license revocations or costly enforcement actions if failed inspections or audits uncover breaches [S6][S15]. The self-reporting of revenue recognition irregularities at BioSteel Sports Nutrition Inc., a former subsidiary involved in the BioSteel Review investigation by the U.S. SEC highlights multi-jurisdictional scrutiny details that have yet unresolved timing or outcome implications [S13].

Margin erosion risk is tangible given proposed reimbursement rate decreases for government-sponsored medical customers adversely impacting profitability within this crucial segment [S2]. Financial reporting lapses culminating in material restatements not only trigger expensive litigation but also burden operational focus on remediation rather than core business acceleration – amplifying sustainability concerns [S14][S16].

What to Watch Next: Regulatory Decisions, Integration Progress, Financial Remediation Milestones

Key upcoming milestones will include progress updates on effectiveness of newly implemented internal controls aimed at remedying the material weakness identified [S3], which is pivotal for reestablishing audit reliability standards. Regulatory approvals connected to recent acquisitions await clearance with timelines uncertain but critical for realizing anticipated growth benefits.

Litigation proceedings emerging from shareholder class actions remain active sources of possible future expense while new product launches within its edibles or vaporizer device categories could influence top-line momentum positively once commercialized successfully [N4][S1]. Monitoring quarterly disclosure on operational KPIs like cultivation volumes alongside margin trends will serve as proxies for underlying demand shifts.

Financial Snapshot: Latest Quarterly Results Highlighting Operating Challenges

For the fiscal fourth quarter ended March 31, 2026, Canopy reported an operating loss of approximately CAD -161.7 million with a net loss expanding to CAD -262.9 million reflecting ongoing expense burdens from remediation efforts and operational inefficiencies [F1]

Current assets standing at approximately CAD 529.5 million versus current liabilities of about CAD 158.4 million produce a healthy current ratio around 3.34 indicating strong short-term solvency fundamentals amidst resource-intensive cycle requirements [F1]. Sustaining this liquidity while improving revenue composition toward higher-margin products alongside resolving compliance issues constitutes the pressing near-term balance sheet challenge.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments