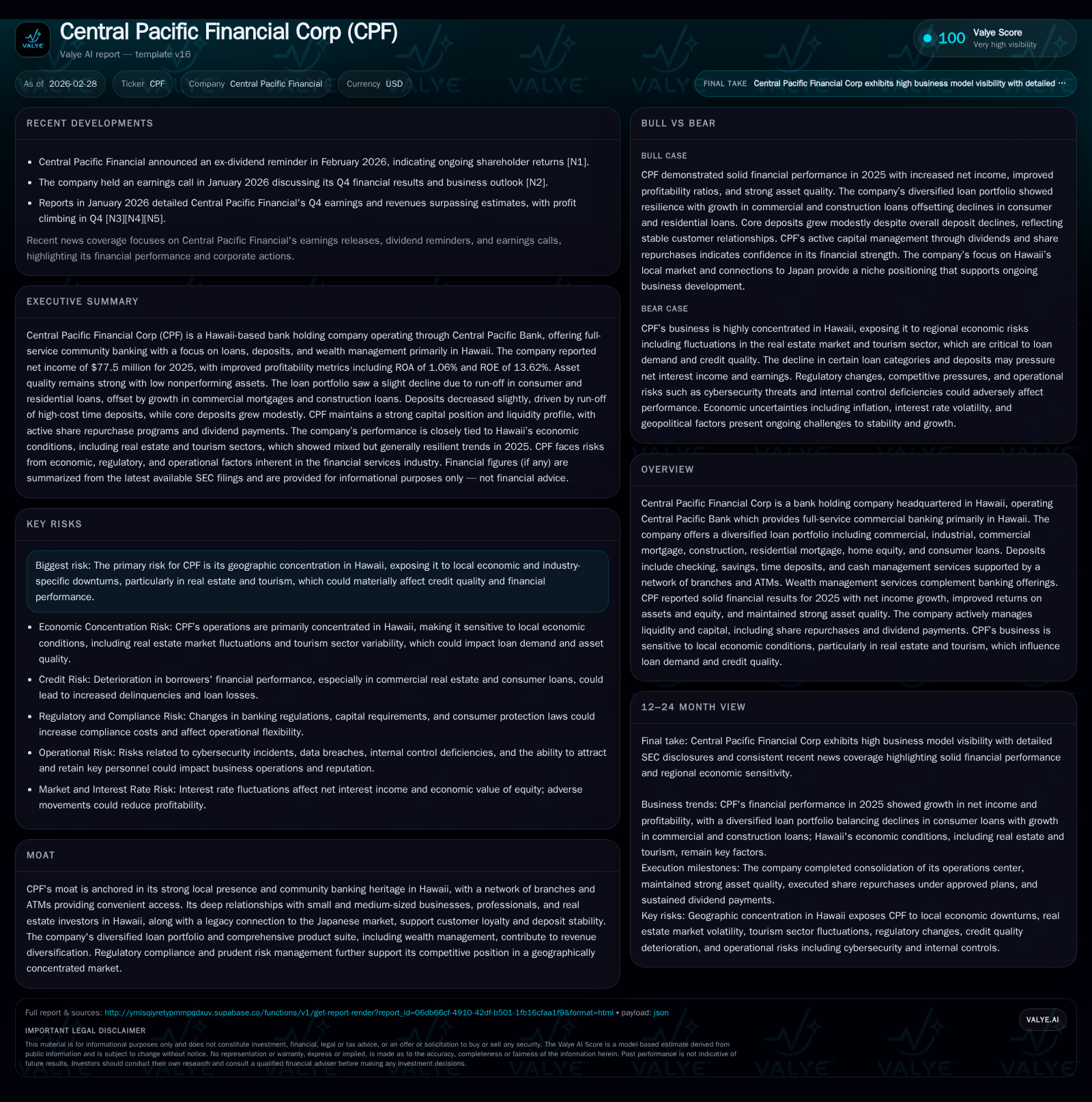

Local Footprint and Loan Mix Power Central Pacific Financial Corp’s Profit Surge

Central Pacific Financial leverages its Hawaii-centric banking model and diversified loan portfolio to deliver strong earnings growth while managing capital strategically.

Central Pacific Financial Corp demonstrated robust revenue growth of 33.8% and net income increase of 45.1% in fiscal 2025, driven by its strong local banking franchise in Hawaii and a diversified loan mix weighted toward commercial real estate, construction, and consumer loans. Asset quality remained sound with nonperforming assets at a low 0.19%, despite some runoff in the home equity segment. The company continued to strengthen shareholder returns through steady dividends and expanded share repurchase programs, supporting an approximate 13.1% return on equity. However, CPF remains exposed to local economic volatility tied to Hawaii’s tourism and real estate sectors, with risk management bolstered by regulatory oversight and capital adequacy.

Financial Journey: Revenue and Earnings Growth Trends

In fiscal year 2025, Central Pacific Financial Corp (CPF) posted a significant rebound with revenue reaching $51.8 million, up 33.8% from $38.7 million in 2024 [F1]. This surge was largely fueled by enhanced net interest income stemming from both a higher average loan portfolio yield and improved fee income linked to deposit accounts and mortgage banking services [S1],[N1]. The company reported net income of $77.5 million for the year, marking a striking 45.1% increase over the prior year's $53.4 million [F1]. Importantly, this improvement reflects operating profitability gains rather than one-time events — although results did factor in a $1.5 million pre-tax charge associated with consolidating operations centers during the third quarter of 2025 [S1],[N3]. Adjusted for this expense, CPF's non-GAAP net income stood at approximately $78.6 million.

Despite challenges faced in prior years due to repositioning losses on investment securities ($9.9 million pre-tax) and strategic assessment costs ($3.1 million pre-tax) in 2024, CPF managed to reverse those impacts effectively [S1]. Concurrently, returns strengthened: adjusted return on average assets climbed from approximately 0.86% in 2024 to about 1.07% in 2025, while adjusted return on equity rose notably from around 12.1% to roughly 13.8%, reflecting enhanced profitability coupled with equity growth [S1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 52 | 77 | 97 | 5 | +33.8% | +45.1% |

| 2024 | 39 | 53 | 91 | 15 | -17.0% | -9.0% |

| 2023 | 47 | 59 | 105 | 13 | -20.6% | |

| 2022 | 74 | 114 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 29 | 92 | 13.1 |

| 2024 | 28 | 75 | 9.9 |

| 2023 | 28 | 92 | 11.6 |

| 2022 | 29 | 96 | 16.3 |

Source: SEC companyfacts cache [F1].

Table highlights CPF's substantial revenue recovery following the prior year dip attributable mainly to repositioning losses.

Evolving Loan Portfolio: Composition and Impact on Income

CPF maintains a diversified loan portfolio focused predominantly on commercial real estate lending—including mortgages for small-to-medium businesses, investors, and developers—as well as construction loans and consumer credit products like residential mortgages and home equity loans [S1]. Although total loans declined marginally by approximately $43.8 million or about 0.8% year-over-year as of December 31, 2025, this decrease mainly reflects runoff within the home equity segment accounting for roughly $76.9 million of reductions [S1],[F1]. Commercial lending balances exhibited relative stability mitigating overall contraction.

Despite this slight shrinkage in loan balances, CPF's borrowers continue to display solid creditworthiness: nonperforming assets rose slightly but remain at an exceptionally low ratio of just about 0.19% of total assets compared with merely 0.15% at the end of fiscal year 2024 [S1]. This underscores effective underwriting protocols combined with disciplined credit risk management adapted for Hawaii’s unique economic environment.

The interplay between CPF's loan mix shift away from home equity loans—a segment typically sensitive to consumer credit cycles—and emphasis on commercial mortgages supported resilience amid fluctuating real estate conditions locally [S2]. This diversified exposure limits volatility in net interest income while safeguarding asset quality.

Strategic Capital Deployment: Dividends, Buybacks, and Returns Analysis

Central Pacific Financial delivered notable capital returns alongside earnings momentum through consistent dividend payments complemented by aggressive share repurchases . Dividend distributions slightly increased from approximately $28.1 million in both previous years (2023–24) to about $29.3 million paid out in fiscal year ending December 31, 2025 [F1]. These payouts remain subject to regulatory approval based on statutory retained earnings under Hawaiian law which stood robust at around $234 million at year-end [S7],[S23].

More dynamic has been CPF’s approach toward share repurchases: authorized initially for up to $30 million under the “2025 Repurchase Plan,” the company completed buybacks totaling $23.3 million during calendar year 2025 which involved repurchasing nearly 788 thousand shares across open markets [S5],[S6]. By December 31st, only approximately $6.7 million worth authorization remained available under this plan before its repeal.

Recognizing value accretion prospects amid stable fundamentals and market conditions, CPF’s Board approved an expanded “2026 Repurchase Plan” authorizing up to $55 million for common stock repurchases commencing January 27th 2026 [S5],[S6],[S7],[N8]. This signifies strategic intent toward enhancing shareholder value through capital return mechanisms backed by solid free cash flow generation estimated at approximately $92 million after capital expenditures lowered dramatically from previous years [F1].

Return metrics reflect these efforts: calculated ROE increased notably from close to ~10% levels during recent prior years to about ~13% for fiscal year 2025 largely driven by earnings leverage paired with efficient capital deployment strategies [F1],[S1].

Local Economic Exposure: Navigating Concentration Risks

CPF’s banking operations are heavily concentrated geographically within Hawaii and thus deeply intertwined with local economic conditions dominated by tourism and real estate activity [S14],[N7]. While its strong brand recognition and community bank status underpin durable customer relationships—particularly among small-medium enterprises, professionals, developers and island residents—this focus inevitably exposes CPF’s balance sheet performance to sector-specific cyclicality.

The company's loan book is closely tied to commercial real estate cycles that tend normal fluctuations linked with inventory levels, pricing trends, construction activity rates as well as demand dynamics shaped by tourism influxes—Hawaii being highly sensitive to external travel and hospitality industry shocks [N7],[S11],[S20]. Any downturn or sustained softness could lead to elevated delinquencies or tighter credit loss reserves impacting financial results.

CPF’s risk disclosures acknowledge this intrinsic concentration risk candidly while emphasizing mitigation through conservative underwriting standards along with vigilant ongoing monitoring performed internally as well as during regulatory examinations overseen separately by Hawaii Division of Financial Institutions alongside the Federal Reserve Board since early 2025 following CPF’s transition into Federal Reserve regulatory jurisdiction [S11],[S14],[S21].

Regulatory Landscape and Its Role in Operational Discipline

Shifts within CPF’s supervisory framework emerged notably when Central Pacific Bank became a Federal Reserve System member state-chartered bank effective January 24th 2025; the FRB assumed primary federal regulatory authority superseding FDIC oversight previously dominant since inception—imposing stricter supervisory expectations including periodic assessments targeting capital adequacy (leveraging Basel III guidelines), asset quality controls, liquidity sufficiency tests plus stress testing exercises encompassing interest rate risk models among others [S1],[S10],[S16],[S21].

As of December 31st 2025, CPF exceeded all minimum regulatory capital thresholds mandated under Basel III supplemented by a Capital Conservation Buffer requiring higher CET1 risk-based ratios ensuring no restrictions or limitations on dividends or bonus payments arise absent deterioration — highlighting balance sheet strength conducive for prudent growth funding [S16],[S22].

Regulatory compliance obligations also encompass areas beyond balance sheet metrics involving transaction risk controls related to internal systems integrity plus compliance training aimed at minimizing legal violations or reputational damage risks identified through annual audit plans spearheaded internally but supplemented by independent auditors mandated per Sarbanes-Oxley governance standards applicable for listed entities such as CPF trading on NYSE under ticker "CPF" [S11],[S14],[S21].

Outlook and Key Performance Indicators to Monitor

While explicit forward-looking guidance remains undisclosed officially per CFO statements or SEC filings available at this writing [N9], several key performance indicators warrant close attention given CPF’s operating profile:

- Loan portfolio growth trajectory particularly within commercial/industrial segments balanced against selective runoffs such as home equity loans which have dragged aggregate volumes recently.

- Asset quality metrics including nonperforming assets ratio trends indicating borrower repayment health amid evolving local economic cycles.

- Net interest margin developments responsive both to prevailing national interest rate environment shifts monitored vigilantly via ALCO simulations demonstrating relative resilience within ±300 basis points scenarios modeled gradually or instantaneously [S15].

- Share buyback execution pace relative to newlyexpanded repurchase authorization provides insight into management confidence regarding valuation support strategies alongside dividend sustainability linked directly with statutory retained earnings influenced also by Hawaii banking regulations.

- External macro factors range from potential Mainland U.S tariff adjustments impacting tourism indirectly through visitor spending power or disruption risks originating domestically including federal government shutdowns affecting overall economic confidence as cited explicitly among identified risk factors [S2],[N7].

Investors should monitor scheduled quarterly earnings releases complemented by investor conference calls where management elaborates operational details substantiating financial disclosures ensuring transparent communication around these critical focal points influencing near-term performance dynamics.

This analysis draws exclusively upon verified financial statements filed with the SEC and recent company announcements without speculative forecasting or investment advice regarding Central Pacific Financial Corp shares.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments