Citius Pharmaceuticals Reassesses Growth Amid Early-Stage Commercialization Pressure

Recent quarterly filings reveal stalled revenue generation and liquidity restraints, underscoring challenges in scaling LYMPHIR™ commercialization.

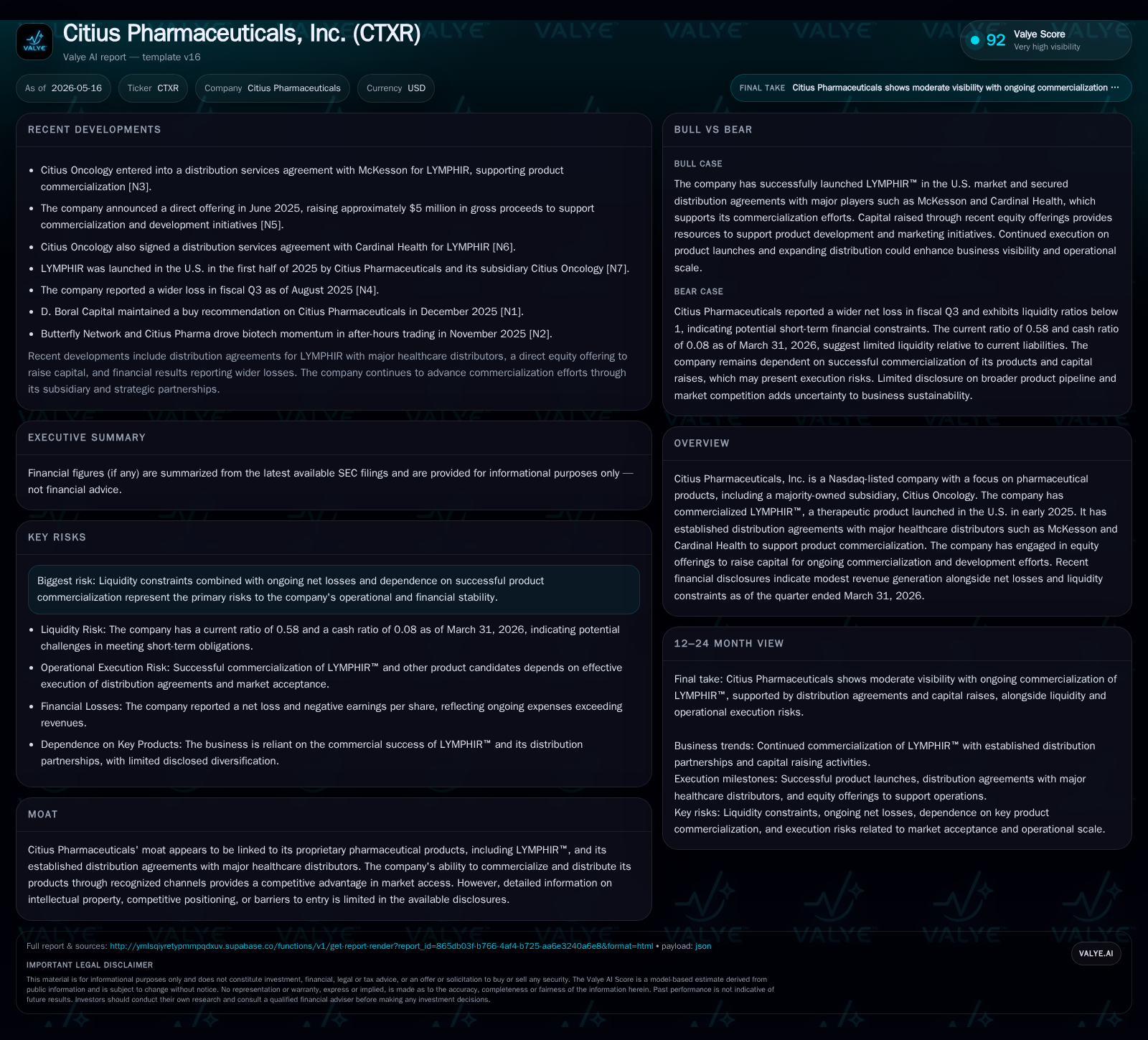

Citius Pharmaceuticals’ latest quarterly disclosure for Q2 fiscal 2026 underscores a revenue plateau despite launching LYMPHIR™ in early 2025. The company continues to grapple with net losses and a strained liquidity position as it activates distribution agreements with major healthcare distributors such as McKesson and Cardinal Health. Its business model hinges on proprietary pharmaceutical products and strong distribution partnerships, but near-term growth remains contingent on improved market adoption and capital access. With no material change in risk factors, financial sustainability and execution efficiency are key watchpoints going forward.

Latest Quarterly Operating Update: Realities of Commercial Execution

The most recent quarterly filing ending March 31, 2026, presents a cautious operating picture for Citius Pharmaceuticals. Despite having launched LYMPHIR™—a proprietary therapeutic product—in early 2025, the company’s reported revenue remains effectively nil [F1], highlighting the slow initial ramp typical of specialty pharmaceutical launches driven by complex payer arrangements and prescriber adoption cycles. Concurrently, net losses continue unabated with no indication of narrowing in the short term [S2].

The May 15, 2026 event filing reiterates these trends and confirms no material changes in risk factors from the prior annual report [S2][S3]. Notably, the company has executed strategic distribution agreements with recognized healthcare distributors such as McKesson and Cardinal Health to underpin product availability across U.S. markets. However, these distribution activations have not yet translated into measurable sales momentum.

Liquidity remains strained: cash and equivalents totaled around $4.6 million at quarter-end against a large current liabilities base exceeding $55 million, resulting in a low current ratio of approximately 0.58—which signals potential near-term funding pressure unless offset by operational improvement or capital inflows [F1]. This financial snapshot signals an essential focus on cash conservation and raising new capital to sustain commercialization efforts without widening losses.

Business Model Overview: Proprietary Pharmaceuticals and Distribution Leverage

Citius Pharmaceuticals operates principally through development and commercialization of proprietary pharmaceutical products. The crown jewel is LYMPHIR™, commercialized primarily via its majority-owned subsidiary Citius Oncology. This biologic therapeutic targets niche patient populations requiring specialized treatment modalities—a segment known for slow but potentially durable uptake that depends heavily on prescriber education and insurance reimbursement pathways [S1].

The business model leverages established contracts with major U.S. pharmaceutical distributors—specifically McKesson and Cardinal Health—to facilitate market reach at scale despite limited internal commercial infrastructure. These relationships form critical conduits enabling product accessibility to hospitals, clinics, and specialty pharmacies nationwide.

From an economic standpoint typical of specialty drug launches, upfront costs are front-loaded into regulatory compliance, marketing outreach to clinicians, inventory buildup at distributors, and establishing payer contracts—all before revenue scales meaningfully. This explains the current situation where expenses outpace revenues significantly during early commercialization phases.

LYMPHIR™’s formulation exclusivity provides differentiation relative to generic alternatives or competitor treatments; however, switching costs remain modest given specialty therapy dynamics where multiple options exist based on specific patient needs. Thus, sustained physician adoption and formulary inclusion will be paramount for future revenue sustainability.

Competitive Environment: Positioning and Moat Considerations

The competitive landscape situates Citius within the specialized pharmaceutical arena focused on immunotherapy-related oncology treatments facilitated by its product LYMPHIR™ (denileukin diftitox-cxdl). Competitors typically include biotech firms developing targeted biologics or novel checkpoint inhibitors addressing similar patient cohorts.

While detailed intellectual property disclosures are limited publicly—restricting a full evaluation of exclusivity breadth—distribution agreements act as tactical moats by granting priority access to broad market channels otherwise difficult for smaller firms to secure. This positioning alleviates some traditional barriers to entry found in specialty pharma such as payor negotiation complexities and supply chain challenges.

Brand trust among prescribing oncologists combined with payer reimbursement policies will influence competitiveness profoundly; because CYTXR’s offerings focus narrowly on select indications, differentiation quality resides more in clinical efficacy signals from ongoing trials orchestrated through its majority-owned subsidiary than sheer commercial scale alone [S1].

Growth Drivers and Fundamental Catalysts

Primary demand expansion catalysts hinge on accelerating physician prescribing behavior for LYMPHIR™ bolstered by positive clinical outcomes data—including investigator-initiated Phase 1 trial results reported earlier this year combining LYMPHIR™ with checkpoint inhibitors like pembrolizumab—potentially driving broader therapeutic adoption in gynecologic cancers [S9].

Formulary inclusions within insurance networks—and subsequently reimbursement approvals—constitute critical commercial gating items requiring continued focus. Geographic expansion moves evidenced by initial shipments to Europe via regional distribution partners reflect strategic attempts to diversify markets beyond the U.S., adding incremental revenue pathways [S17].

Capital deployment from recent equity offerings completed in April 2026 aims expressly at supporting these commercialization milestones along with pipeline advancement across all product candidates under development [S19]. Enhanced liquidity could enable more aggressive marketing campaigns or expanded clinical collaborations necessary for deeper market infiltration.

Risks and Constraints: Funding, Market Penetration, and Operational Execution

Liquidity positions raise immediate concerns; the imbalance between cash reserves ($4.6 million) versus current liabilities ($55 million) constrains operational flexibility under current burn rates without supplementary financing rounds or cost rationalization strategies [F1].

Net losses persist systematically as upfront expenses related to marketing infrastructure establishment, clinical trial investment through subsidiaries, and regulatory obligations outpace minimal current revenues. Failure to expedite market penetration or broaden prescriber adoption could exacerbate financial pressures leading to dilution risks or insolvency threats absent corrective actions [S2].

Execution risks also extend into payer environments where negotiation delays or restrictive formulary decisions may stifle widespread product utilization—especially pertinent given product-specific competitive dynamics prevalent among immunotherapy drugs targeting oncology sectors.

Successful execution on these fronts will be imperative for stabilizing operations while laying foundation for longer-term structural growth.

Financial Snapshot: Liquidity and Expense Profile

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $4.6mm | |

| 2026-03-31 | ||

| Current assets | $31.7mm | |

| 2026-03-31 | ||

| Current liabilities | $55.0mm | |

| 2026-03-31 | ||

| Current ratio | 0.58x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) |

|---|---|

| Cash & Equivalents | 4,590,174 |

| Current Assets | 31,685,701 |

| Current Liabilities | 55,015,569 |

| Current Ratio | 0.58 |

This financial snapshot captures the core challenge confronting Citius Pharmaceuticals: a modest cash buffer juxtaposed against substantial short-term obligations culminating in a working capital deficit. While total debt levels appear negligible comparatively (~$600k as last estimated), acute liquidity pressure emanates predominantly from operational liabilities incurred during commercial buildout phases rather than leverage burdens [F1]. The absence of meaningful revenues accentuates dependency on external capital infusions.

This analysis synthesizes recent SEC disclosures through Q2 fiscal year 2026 emphasizing that Citius Pharmaceuticals remains at an inflection point characterized by early-stage commercialization headwinds typical within specialty biopharma launches. Its proprietary asset LYMPHIR™ enjoys distribution support forming foundational moat components but has yet to generate substantive top-line traction amidst constrained liquidity profiles requiring vigilant monitoring of execution outcomes.

Any use of this report should be confined to informational purposes only; it does not constitute investment advice or recommendations regarding securities of Citius Pharmaceuticals or any entity discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments