DAQO New Energy's Recovery Challenge Amid Solar Industry Fluctuations

Latest quarterly results reveal a significant revenue decline yet improving operating loss trends amid volatile polysilicon market conditions.

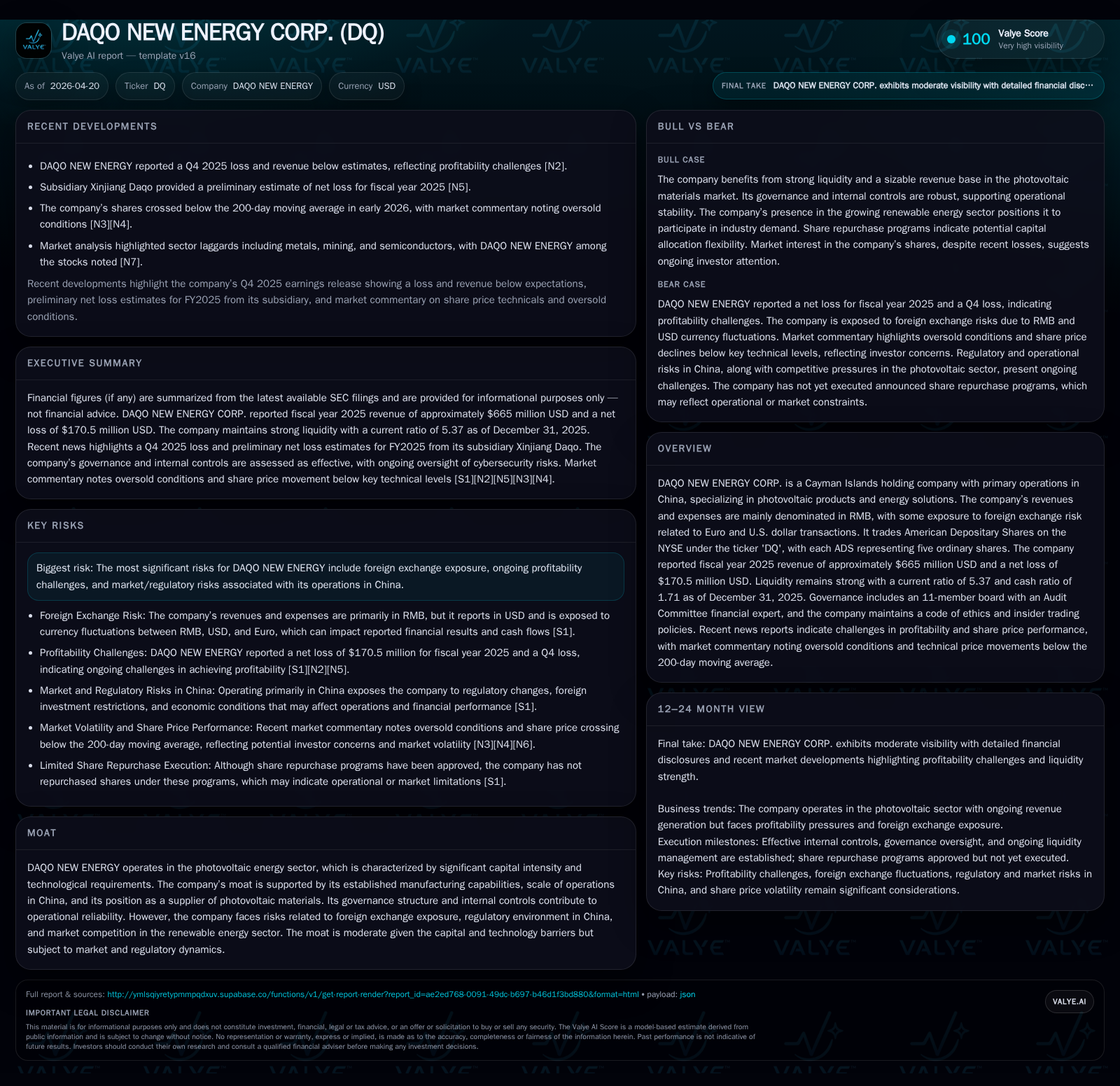

DAQO New Energy Corp. reported a substantial year-over-year revenue decline of approximately 35% in Q1 2026 alongside a narrowing of operating losses, signaling potential stabilization after extended solar market headwinds. The company remains a key polysilicon producer within China’s capital-intensive photovoltaic materials industry, facing structural challenges including foreign exchange exposure, regulatory constraints on dividend repatriation, and sustained profitability pressures. Capacity expansion and technology upgrades underpin growth prospects, although global solar demand volatility and pricing competition temper near-term outlooks. DAQO’s strong liquidity position affords operational flexibility while ongoing execution of cost controls and market navigation will be critical.

Q1 2026 Operating Update: Revenue Deterioration and Margin Trends

DAQO New Energy's most recent quarterly filing on April 15, 2026 [S2] continues to reflect challenges faced by the company during a turbulent photovoltaic materials market. The company reported a year-over-year drop in revenues to approximately $170 million in the quarter—a roughly 35% decline consistent with broader industry contraction evidenced also in fiscal year results [F1]. However, the operating loss narrowed relative to prior periods, suggesting some progress in cost control efforts and operational efficiency gains despite top-line pressures. Early indicators from March filings [S3] were similar, underscoring a trend of volume softness offset partially by margin stabilization.

This combination underlines DAQO's current phase: combatting solar polysilicon price depressions and fluctuating demand while aiming to improve earnings quality through disciplined manufacturing practices.

Business Model and Product Quality: The Photovoltaic Materials Value Chain

DAQO earns its revenues predominantly through the production and sale of high-purity polysilicon — a critical raw material for photovoltaic cells — mainly operating within its large-scale facilities located in China. Revenues and expenses are primarily transacted in RMB; the company acts as a supplier within China's vertically integrated solar energy ecosystem [S1]. Meeting stringent purity standards is imperative to maintain product relevance as cell manufacturers increasingly demand materials that enhance module conversion efficiency.

Capital intensity is pronounced given the large investments required in silicon purification plants and continuous technological innovation to reduce costs per kg of output [F1]. DAQO's scale in Xinjiang provides it a competitive advantage against smaller entities but still exposes it to cyclical swings in polysilicon pricing driven by global solar module demand dynamics.

Industry Dynamics: Competition, Pricing, and Regulatory Influences in China

Within China's photovoltaic materials sector, DAQO contends with major domestic competitors alongside global suppliers, each navigating intensified pricing pressures during global oversupply episodes [S1]. These dynamics stem from shifting government subsidies for renewables and periodic demand fluctuations linked to policy-driven installation spurts or slowdowns.

Regulatory oversight is another variable influencing DAQO’s operations — notably PRC restrictions limiting upstream subsidiaries' ability to remit dividends to the Cayman-listed holding entity inhibit free cash flow mobility [S13]. This structural constraint impacts capital allocation decisions at the parent level, complicating shareholder returns despite adequate internal cash generation capacity.

Furthermore, currency risk adds complexity; although operating predominantly in RMB reduces transactional forex exposure, profits reported in USD can be materially affected by fluctuations between RMB and USD values [S17]. Currently, DAQO does not engage in active hedging against such currency headwinds.

Growth Drivers: Capacity Expansion, Technology, and Market Demand

Despite recent volatility, global trajectories for renewable energy adoption suggest structural growth potential for quality polysilicon producers like DAQO. Management outlined intentions to continue scaling installed capacities selectively while prioritizing technological advances aimed at reducing production costs and enhancing wafer compatibility [S1].

Annual capex has moderated from previous peaks—down approximately 50% year-over-year—to just over $170 million [F1], reflecting cautious investment pacing amid uncertain market conditions but maintaining foundational infrastructure upgrades expected to pay dividends as sector recovery materializes.

Demand drivers remain linked to accelerating solar module installations worldwide despite intermittent policy-induced slowdowns within China. Long-term clean energy commitments bolster DAQO’s strategic rationale albeit shadowed by near-term headwinds.

Limitations to Growth: Profitability Challenges and Foreign Exchange Exposure

A persistent obstacle for DAQO resides in its inability thus far to consistently generate net profits despite improved operational results; fiscal year 2025 ended with a net loss of approximately $170 million though ameliorated versus prior years [F1]. Structural cost bases compounded by cyclical price weakness weigh heavily.

Foreign exchange adds an additional layer of complexity as earnings reported in USD vary significantly relative to RMB movements; appreciation or depreciation impacts financial statement translation without changing operational performance per se [S17].

Moreover, PRC dividend remittance restrictions create impediments for transferring subsidiary cash up the chain potentially limiting parent company liquidity deployment flexibility [S13]. This restricts DAQO’s ability to return capital via dividends or aggressively pursue share repurchases beyond token amounts authorized but unexecuted as of end-2025 [S4][F1]. These factors collectively constrain free cash flow availability—the approximate free cash flow negative $123 million figure underscores ongoing reinvestment needs over shareholder return priorities [F1].

Capital Allocation and Liquidity Position

Despite operational challenges, DAQO maintains a conservative balance sheet stance marked by strong liquidity ratios: current ratio stands at about 5.37x supported by cash equivalents upwards of $850 million as of end-2025 [F1]. This cushion provides runway for weathering continued market softness while preserving investment optionality.

The board has authorized multiple share repurchase programs totaling $100 million across overlapping periods; however actual execution lags with no significant repurchases completed thus far [S4][S5]. Dividend payments have been withheld primarily due to regulatory uncertainties regarding subsidiary distributions [S11]. These decisions reflect prudent capital stewardship prioritizing operational recovery before shareholder yield enhancements.

Financial Summary: Recent Fiscal Year Performance and Balance Sheet Strength

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0.7 | -171 | 0.0 | -0.3 | -35.3% | +50.6% |

| 2024 | 1.0 | -345 | -0.4 | -0.6 | -55.4% | -180.4% |

| 2023 | 2.3 | 430 | 1.6 | 0.8 | -49.9% | -76.4% |

| 2022 | 4.6 | 1820 | 2.5 | 3.0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 5 | -123 | -3.9 |

| 2024 | 5 | -794 | -7.9 |

| 2023 | 486 | 505 | 9.0 |

| 2022 | 125 | 1257 | 37.9 |

Source: SEC companyfacts cache [F1].

Fiscal year 2025 revenue contracted sharply by over 35% compared to 2024 levels reaching approximately $665 million alongside a halving of operating losses (about -$270 million) evidencing cost discipline progression yet underscoring profit challenges remain acute [F1]. Net income losses narrowed correspondingly but remain negative (-$170 million), manifesting ongoing pressure.

Operating cash flow swung positive reaching nearly $50 million after prior years’ outflows indicating incremental improvement in working capital management or operational cash generation efficacy [F1]. Capital expenditures tapered meaningfully reflecting restrained expansion capex choices aligned with uncertain sector trends.

Equity base remains stable near $4.4 billion supporting solvency although return metrics remain negative consistent with net loss persistence [F1]. Overall financial posture is robust yet profitability has yet to sustainably rebound.

Key Milestones and Watchpoints for Investors

Future investor focus should calibrate around:

- Upcoming Q2-Q4 quarterly reports for confirmation of revenue trajectory stability or further deterioration,

- Margins trends reflecting successful cost control or resumption of pricing power after recent softness,

- Changes in PRC regulatory environment notably regarding dividend policy which could unlock holding-level cash deployment flexibility,

- Currency exchange rate movements versus dollar given sizable RMB-denominated operations but USD-reporting currency,

- Execution progress on capacity expansions or technological innovations lowering unit costs,

- Management commentary on evolving competitive landscape domestically and internationally.

Continued improvements or failures across these dimensions will be pivotal in determining DAQO’s path from recovery toward sustainable profitability within the cyclically challenged yet structurally promising solar polysilicon segment.

This analysis is based solely on information available through SEC filings as of April 20, 2026 ([F1], [S1]–[S29]) without incorporating external data sources or providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments