Evogene Ltd. Navigates Revenue Volatility and Regulatory Complexities Amid Platform Innovation

The Israeli biotechnology firm leverages its proprietary CPB platform and licensing agreements for growth, balancing ongoing net losses with a strong liquidity position.

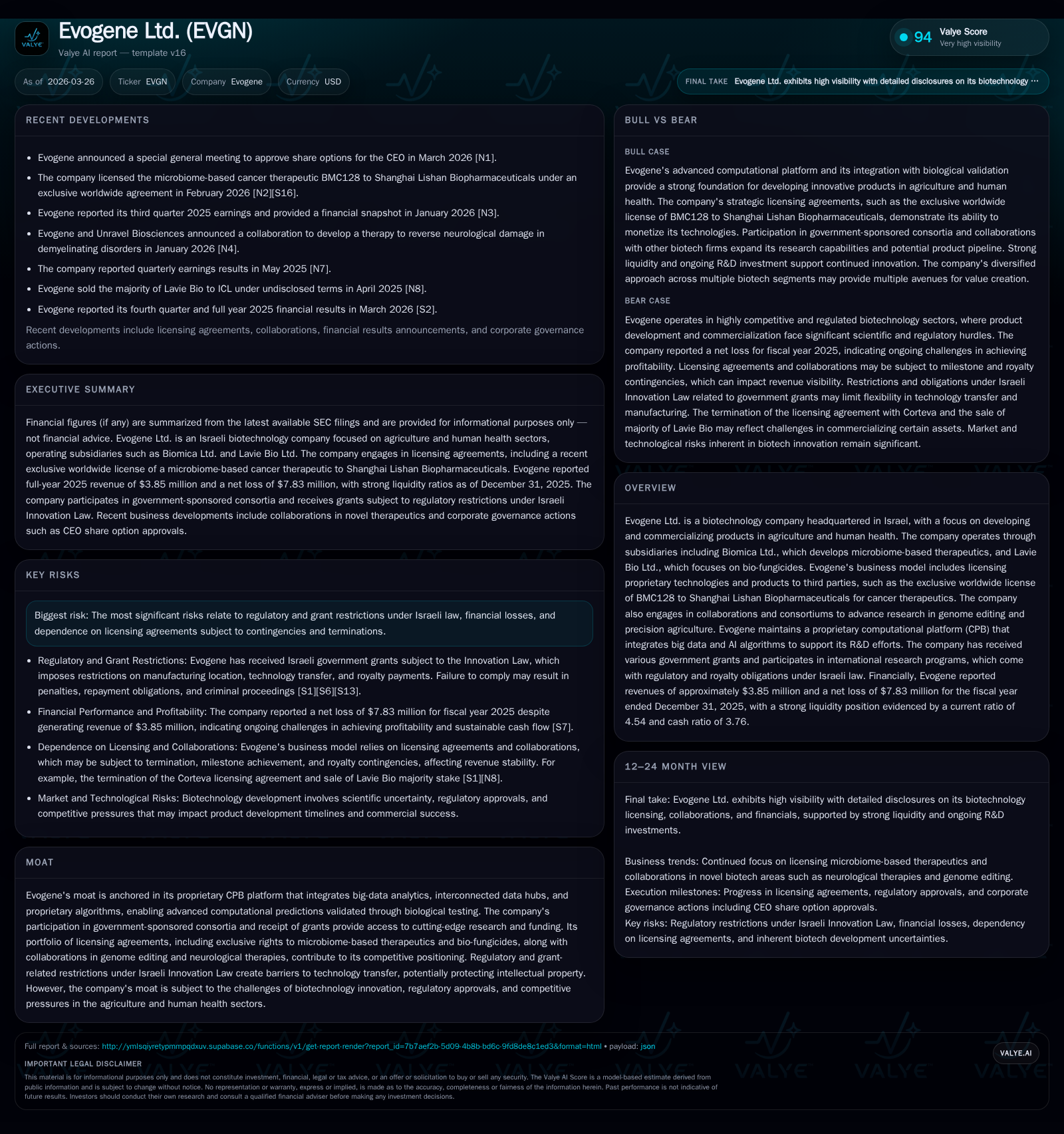

Evogene Ltd., an Israel-based biotech company specializing in agriculture and human health, reported a 54.7% revenue decline in 2025 to $3.85 million from $8.51 million in 2024, reflecting shifts in licensing arrangements including the termination of Lavie Bio's bio-fungicide license with Corteva Agriscience. Despite continued net losses, which narrowed to $7.83 million in 2025, the company maintains a solid cash position of $12.96 million supporting ongoing R&D investments. Key growth drivers include the exclusive license of microbiome therapeutic BMC128 to Shanghai Lishan Biopharmaceuticals and government-sponsored research consortia, while regulatory constraints under Israeli Innovation Law present operational challenges. Capital raised through warrant exercises in early 2026 strengthens the balance sheet for future initiatives.

Company Overview

Evogene Ltd., headquartered in Israel, operates within biotechnology sectors focusing on agricultural traits and human health therapeutics. Its competitive advantage derives from a proprietary Computational Predictive Biology (CPB) platform integrating big data and AI algorithms to discover novel biological targets and products. Subsidiaries such as Biomica Ltd. specialize in microbiome-based therapeutics while Lavie Bio Ltd. focuses on bio-fungicides for crop protection [S1][S11].

The company’s business model relies heavily on licensing agreements that grant third parties rights to its technologies—exemplified by the exclusive worldwide license of BMC128 to Shanghai Lishan Biopharmaceuticals—which includes milestone payments linked to clinical progress and sales royalties [S1][S11][S14]. Additionally, Evogene participates in government-sponsored consortia advancing genome-editing technologies and precision agriculture tools [S14].

Historical Performance

Evogene’s revenue has experienced significant fluctuations tied to licensing dynamics and R&D investment cycles. Revenues increased from approximately $1.68 million in FY2022 to $8.51 million in FY2024 before declining sharply by nearly 55% to $3.85 million in FY2025. This drop primarily reflects the November 2024 termination of Lavie Bio’s bio-fungicide license with Corteva Agriscience; however, Evogene retained the initial $5 million payment from Corteva and regained full rights to the associated intellectual property [F1][S1][S4].

Net losses have decreased progressively over this period, narrowing from -$29.84 million in FY2022 to -$7.83 million in FY2025, indicating improved expense management despite ongoing high levels of R&D spending [F1]. Equity has also declined over these years.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 4 | -8 | -54.7% | +56.6% |

| 2024 | 9 | -18 | +50.9% | +30.4% |

| 2023 | 6 | -26 | +236.7% | +13.0% |

| 2022 | 2 | -30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -65.4 |

| 2024 | -121.7 |

| 2023 | -90.5 |

| 2022 | -85.8 |

Source: SEC companyfacts cache [F1].

Growth Outlook

Evogene’s growth strategy centers on leveraging its CPB platform for discovery of new traits and therapeutics across agriculture and human health markets supported by licensing deals [S1][S14]. The recent exclusive license granted for BMC128 positions Biomica-derived microbiome therapeutics for clinical development milestones that could generate future payments and royalties [S11].

Despite these opportunities, risks remain related to dependence on external partners’ clinical progress and regulatory approvals inherent in biotech innovation [S5][S7]. The reacquisition of bio-fungicide rights previously licensed to Corteva offers potential re-commercialization pathways but will require additional capital or partnerships.

Government grants foster innovation through consortium programs but impose compliance requirements that may constrain certain operational flexibilities, particularly regarding technology transfer outside Israel [S5][S6][S14].

Milestones & Expectations

While no formal guidance was provided for near-term financial metrics [N1][S2], anticipated milestones include:

- Clinical trial progression of BMC128 under Lishan Biopharmaceuticals potentially triggering development milestones;

- Potential announcements related to bio-fungicide product redeployment or new collaborations;

- Enhancements of the CPB platform leading to novel discoveries and licensing opportunities. Monitoring these developments will be key indicators of financial inflection points.

Capital Allocation & Returns

Evogene’s return on equity remains negative at approximately -65%, reflecting net losses against declining equity [F1]. The company does not pay dividends nor conduct share buybacks, instead allocating capital primarily toward research activities and platform advancement supported by governmental grants [S20][S23].

Liquidity is robust with cash and equivalents totaling $12.96 million at year-end 2025 and a current ratio around 4.54, underpinned by recently completed warrant exercises which raised an estimated $3-4 million in early 2026 at favorable exercise prices [F1][S16][S20]. This capital infusion enhances financial flexibility for continued investment.

Competitive Advantages & Risks

Evogene’s core competitive moat is its CPB platform combining computational biology with experimental validation capabilities—a technology asset strengthened by participation in government-funded consortia providing funding support and collaborative synergies [S14]. However, regulatory constraints under Israeli Innovation Law require local manufacturing of grant-supported products, mandate royalties on income generated globally from funded technologies, and restrict transferability without prior approvals—factors complicating international commercialization efforts [S5][S6][S7].

Additionally, revenue volatility driven by milestone-dependent licensing agreements introduces uncertainty while long biotech development timelines elevate execution risk.

Summary

Evogene Ltd.’s profile illustrates a biotechnology innovator balancing volatile revenues tied to licensing dynamics against improving net loss trends supported by strategic R&D investments via its proprietary CPB platform amid complex regulatory frameworks centered in Israel.

Revenue contraction following license terminations contrasts with capital raises via warrant exercises strengthening liquidity for ongoing initiatives focused on clinical advancement of out-licensed therapeutics such as BMC128 alongside potential redeployment of regained bio-fungicide assets.

Investors should monitor clinical milestones under licensees, partnership developments related to re-commercialized products, and regulatory approvals affecting technology transfer given their significant impact on Evogene’s commercial trajectory.

This analysis is based solely on reported financial data, SEC filings, news releases, and company disclosures without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments