Evotec SE's Shift to Asset-Light Model Accelerates Innovation and Revenue Streams

Evotec’s strategic divestment of manufacturing assets complements its integrated drug discovery platform, enhancing financial flexibility and future revenue streams.

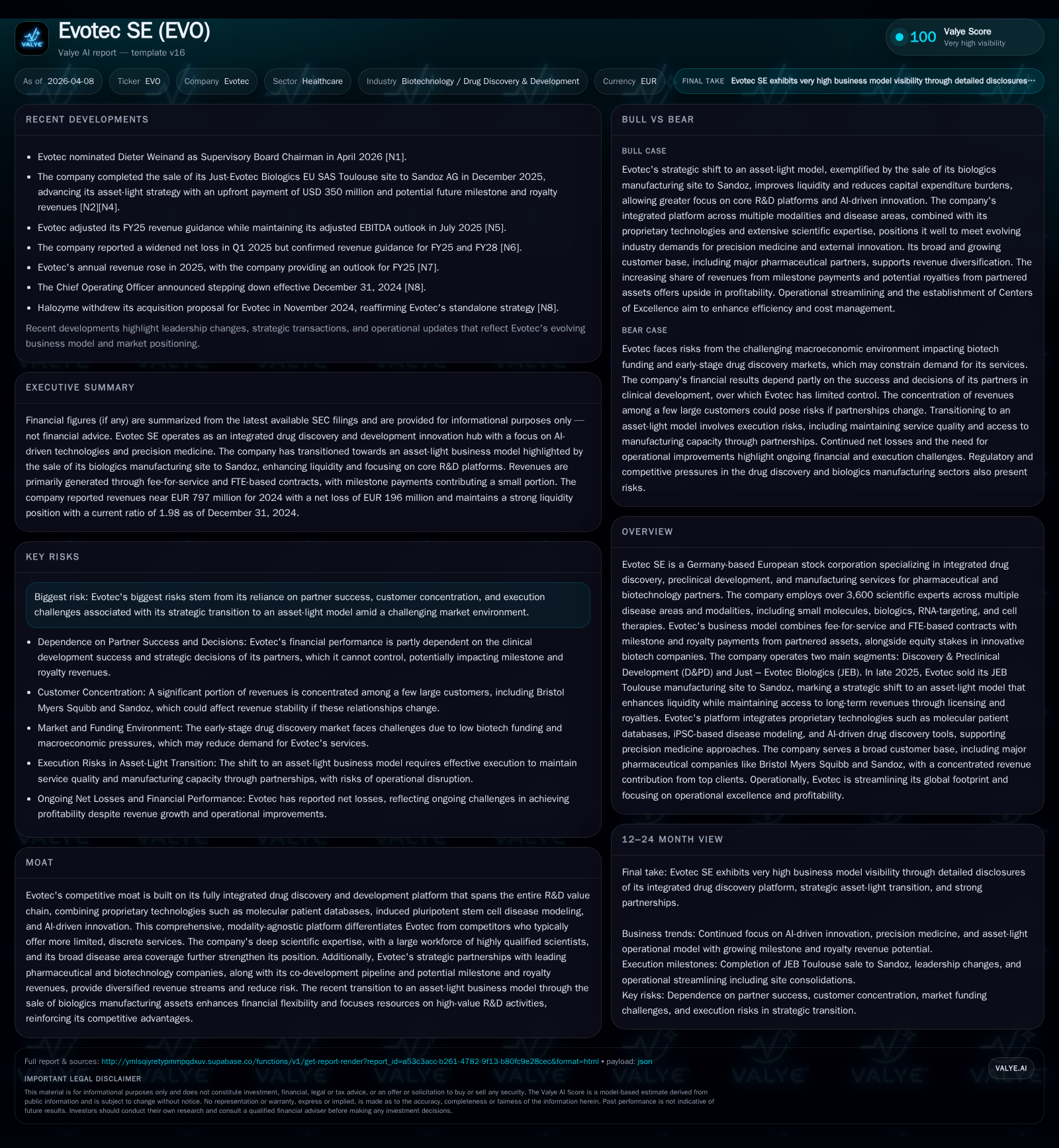

Evotec SE, a leading integrated drug discovery and development player, marked a pivotal shift in late 2025 by selling its Just – Evotec Biologics Toulouse manufacturing site to Sandoz, transitioning toward an asset-light model. This move strengthens liquidity and preserves long-term licensing and royalty income, underscoring a new phase emphasizing operational excellence alongside platform innovation across modalities such as small molecules and cell therapies. While revenue growth has moderated with challenges in net profitability driven by elevated R&D investment and restructuring costs, the company’s integrated technology stack and broad partnership ecosystem position it well for selective growth. Key risks remain partner dependency and execution as Evotec balances innovation investments with capital discipline.

Historical Growth: Revenue Expansion and Shifting Profitability Landscape

Evotec SE’s top-line trajectory from fiscal 2021 through 2024 reveals gradual but steady revenue growth with notable shifts in profitability profile. Revenues expanded from €618 million in 2021 to €797 million in 2024, representing a compound annual growth rate (CAGR) approximating 8% over this period but a more modest 2% increase from 2023 to 2024 alone [F1]. Despite growing sales, net income has swung sharply into deeper losses: a positive net income of €216 million in 2021 gave way to recurring net losses reaching nearly €196 million by end-2024 [F1]. Profitability pressures stem largely from sustained elevated R&D expenditures necessary for platform expansion alongside impairments tied to evolving partnership assets.

This mismatch reflects the company’s deliberate investment posture supporting technology enhancement across multiple modalities while negotiating a complex portfolio of collaborations and early clinical-stage projects. The return on equity correspondingly declined from positive levels above 15% in 2021 to –20.6% at the end of 2024 [F1], highlighting margin compression amid reinvestment cycles.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 797 | -196 | +2.0% | -133.7% |

| 2023 | 781 | -84 | +4.0% | +52.2% |

| 2022 | 751 | -176 | +21.6% | -181.5% |

| 2021 | 618 | 216 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | -20.6 |

| 2023 | -7.5 |

| 2022 | -14.8 |

| 2021 | 15.6 |

Source: SEC companyfacts cache [F1].

The Two Pillars: Discovery & Preclinical Development and Just – Evotec Biologics

Evotec operates two core segments illustrating complementary parts of the drug development continuum. The Discovery & Preclinical Development (D&PD) segment centers on integrated drug discovery services that combine fee-for-service contracts with full-time-equivalent (FTE)-based engagements alongside milestone and royalty income derived from asset partnerships [N/A]. This segment spans diverse modalities including small molecules, biologics candidates, RNA-targeting approaches, and cell therapies.

Unlike typical discovery service providers that often focus narrowly on discrete technologies or modalities, Evotec’s modality-agnostic platform leverages induced pluripotent stem cell (iPSC)-based disease modeling jointly with advanced molecular patient databases. Complemented by artificial intelligence-driven computational innovation tools, this provides a seamless capacity for target validation through lead optimization up to investigational new drug (IND) enabling activities. This breadth equips Evotec to customize partnerships ranging from straightforward service delivery agreements to collaborative pipeline co-development ventures.

Just – Evotec Biologics (JEB), formerly responsible for advanced biologics manufacturing infrastructure including continuous processing capacity within facilities such as the Toulouse site, represents the production arm backing later-stage translational activities [N/A]. The operational focus bifurcates between standard CDMO manufacturing services supplemented by proprietary technology assets within continuous manufacturing.

Strategic Shift: Impact of the JEB Toulouse Site Sale on Business Model

In December of 2025, Evotec completed the sale of its JEB Toulouse manufacturing operation to Sandoz AG marking a definitive strategic pivot towards an asset-light model [N1][S2]. This deal involved full divestiture of the physical facility alongside connected agreements ensuring continued technology licensing rights for Evotec that allow royalty participation over a biosimilar portfolio expanding over originator drugs worth more than $90 billion globally [S24].

Financially, the transaction was transformative — generating upfront cash proceeds estimated near $350 million which bolstered liquidity immediately post-closing [S7][S24]. Operationally this divestment reduces capital intensity significantly by unloading fixed asset burden while preserving scalable long-term revenue streams through licenses and royalties rather than purely manufacturing fee-for-service margins.

From a margin perspective, although direct revenues derived from manufacturing activities now decline correspondingly—which accounted for approximately one-third of group revenues pre-sale—the overall gross margin improves due to reduced operational cost base offsetting raw manufacturing overheads [S9]. The shift also enhances strategic flexibility allowing reinvestment focused on platform innovation rather than facility expansion amid persistent macroeconomic cost pressures.

Innovation Edge: Platform Capabilities and Portfolio Diversification

Central to Evotec’s moat is its industry-leading scientific infrastructure combining proprietary molecular patient databases along with disease models rooted in induced pluripotent stem cells (iPSC). This unique integration fosters unprecedented biological insights supporting target identification across oncology, CNS disorders, cardiovascular-renal conditions, immune/inflammation diseases among others .

Complementing these biological tools is Evotec’s active application of AI-driven algorithms that accelerate lead generation cycles far beyond traditional methods [S11]. Such multi-modal integration is relatively rare among contract research organizations that typically specialize either in computational approaches or discrete wet lab experimental platforms alone.

The company’s diversified portfolio includes assets in co-development partnering arrangements where milestone success can generate non-linear revenue uplifts beyond pure service fees. This diversification partially mitigates risk inherent in any single project’s clinical or regulatory outcome [S13]. Additionally, equity stakes in select innovative biotech companies related to its pipeline foster potential upside returns beyond conventional contract revenue streams.

2026 Outlook: Forecast Drivers, Partnership Milestones, and Macroeconomic Context

While no explicit quantitative guidance was released for full-year 2026 within filings inspected [N2][S4], management commentary highlights balancing aggressive R&D investment — particularly targeting strategic platforms such as E.MPD (multi-parameter diagnostics), PanOmics comprehensive profiling suites, iPSC-based cell therapy origination, targeted protein degradation modalities — against prudent financial stewardship under ongoing economic headwinds [S4][S23].

A salient near-term catalyst is the projected receipt of approximately $100 million related to the Tubulis acquisition consortium closing scheduled during early-to-mid-2026 [N1][N2], which will bolster working capital availability further facilitating pipeline advancement activities.

Sector-wide challenges affecting precise investment include inflationary cost environments impacting labor and consumables alongside heightened competition for high-caliber scientific talent especially within biotech hubs across Europe and North America . Nonetheless, increasing demand for external innovation supports sustained outsourcing levels providing tailwinds to the integrated service model deployed by Evotec.

Capital Allocation Strategy: Balancing R&D Investments, Cash Flow, and Shareholder Returns

Evotec’s capital allocation priorities reflect its strategic emphasis on sustaining technology platform advancement while transitioning towards financial discipline catalyzed by operational restructuring initiatives.

On a balance sheet basis at December 31, 2024, liquid assets including cash equivalents stood at roughly €306 million—highlighting improved liquidity reserves after conclude of asset disposals—and current ratio of about 1.98 indicating adequate short-term solvency [F1][S7].

Capital expenditures dropped substantially in fiscal year 2025 chiefly due to reduced biologics plant capex following Toulouse facility completion coupled with divestment effects; total capex was €72.5 million down from €117.5 million year prior [S22]. Meanwhile unpartnered R&D expenses decreased meaningfully from €50.9 million in 2024 to about €37.5 million in 2025 signaling tighter control albeit continuing commitment towards enhancing integrated platforms [S23].

Despite these measures net loss persisted near –€103 million range for last reported period reflecting absorptions related to restructuring charges plus residual impairments though showing clear improvement vs prior year – suggesting trajectory toward normalization if operational efficiencies are realized fully [F1][S6].

No dividends or share buyback programs are currently disclosed evidencing reinvestment focus rather than capital return initiation at this stage given ongoing transformation efforts [F1].

Governance and Leadership Transition: New Supervisory Board Chairman Appointment

On April 7th, 2026 Evotec announced the nomination of Dieter Weinand as the new Supervisory Board Chairman—effective immediately—following board approval steps outlined under corporate governance frameworks governing German Societas Europaea listed companies [N1][S2].

Weinand brings extensive leadership experience with established expertise steering complex biopharmaceutical enterprises through phases of strategic realignment [N1]. His appointment signals reinforcement at governance level aimed at overseeing execution risks linked with the company’s multi-year transformation including asset-light strategy adoption alongside focused platform expansion.

Risk Profile: Partner Dependency and Execution Challenges Amid Market Changes

Evotec faces notable risk factors inherent in its highly collaborative operating model where financial outcomes depend significantly on partner progress along clinical pipelines as well as regulatory approval attainment—outcomes largely outside direct corporate control [S13].

Customer concentration is increasing; top ten clients accounted for about 61% of revenues in 2025 up from around half just two years prior—concentration risks primarily tied to Bristol Myers Squibb (BMS) and Sandoz each exceeding individual revenue contributions over ten percent annually [S11][S16]. This heightens vulnerability should partnership dynamics shift unexpectedly.

Transitioning business models away from capital-intensive biologics manufacturing entails execution risks particularly involving integration complexity post-Toulouse divestiture plus calibration of internal cost structures consistent with leaner asset footprint amidst macroeconomic uncertainty including inflationary wage pressures and supply chain volatility [S8][S19].

Mitigation strategies encompass diversification via multiple contract types (fee-for-service/FTE engagements), broad disease area coverage limiting over-reliance on singular therapeutic focus areas, continual reinvestment into proprietary platforms strengthening competitive differentiation plus close partner relationship management fostering repeat business (~90% annual repeat rates noted recently) [S10][S21]. Nonetheless vigilance remains imperative as evolving marketplace conditions may challenge forecast reliability.

This analysis is based solely on publicly available information up to April 8th, 2026 without insider knowledge or predictive judgments beyond disclosed facts. It is intended purely for informed internal reference regarding Evotec SE’s recent strategic initiatives and operational performance trends without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments