Envirotech Vehicles Faces Nasdaq Equity Compliance Hurdle While Diversifying Hardware Ventures

Nasdaq compliance issues spotlight financial pressures as Envirotech expands from EVs into medical manufacturing, drones, and AI infrastructure.

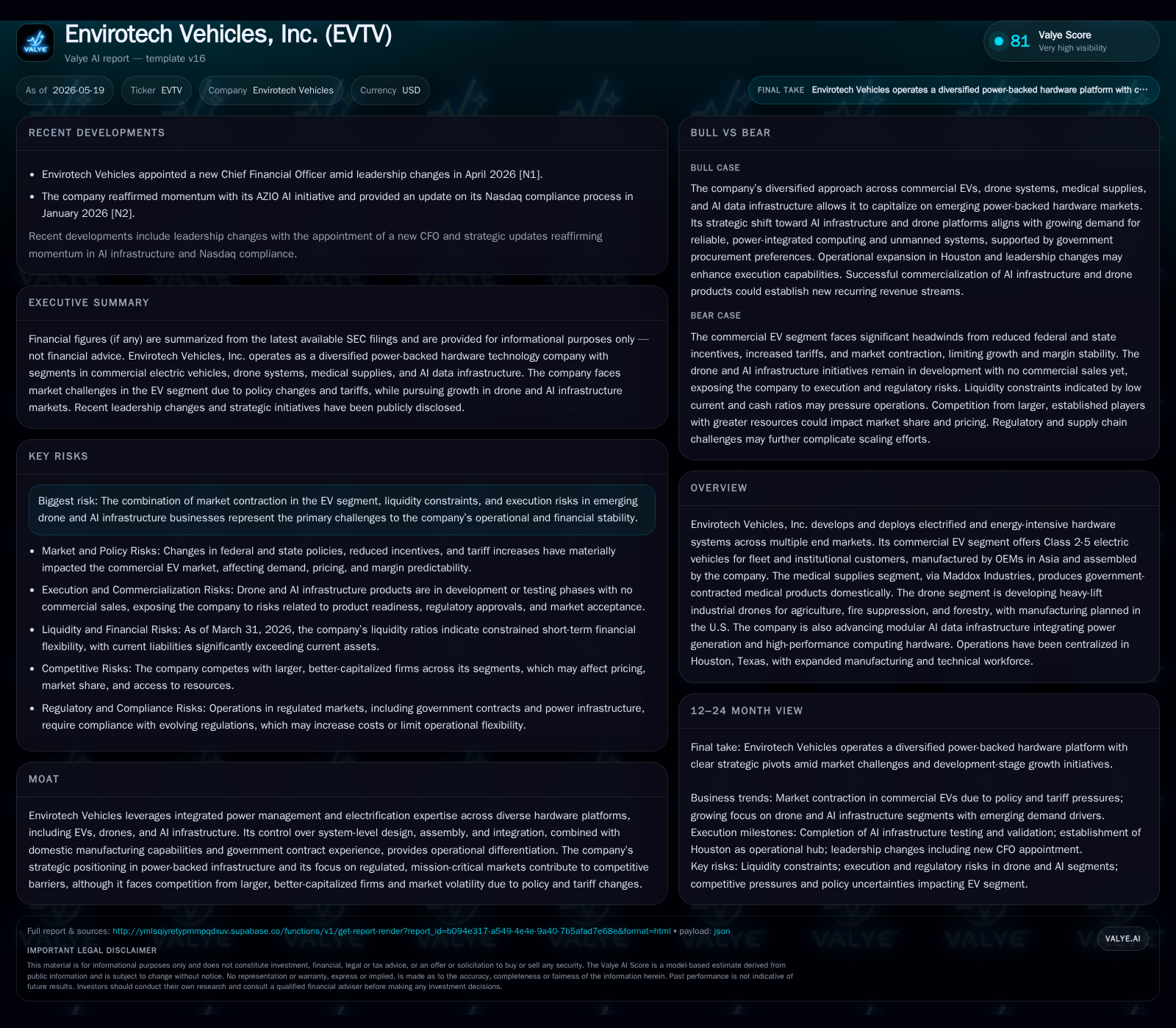

Envirotech Vehicles, Inc. recently received a Nasdaq notice for failing to meet the minimum shareholders’ equity requirement amid ongoing financial strain and market headwinds in its core commercial EV segment. The company is actively pivoting toward diversification through domestic medical supplies manufacturing, heavy-lift industrial drones, and modular AI data infrastructure development, leveraging its electrification and power management expertise. These strategic shifts aim to mitigate margin pressure and capitalize on higher-margin, recurring revenue opportunities while contending with liquidity constraints and execution risks inherent in scaling emerging businesses.

April Executive Summary: Nasdaq Notice and Strategic Implications

On April 29, 2026, Envirotech Vehicles received a formal notice from Nasdaq citing non-compliance with the minimum stockholders’ equity requirement of $2.5 million reported at fiscal year-end 2025 [S3]. The company has until June 13 to submit a compliance plan with potential extension to October 26 if accepted by Nasdaq. This event underscores financial challenges amid operational headwinds and intensifies the need for disciplined capital management highlighted in the May quarterly filing [S2]. Maintaining listing status is critical for investor confidence and access to public markets.

Business Model: Integrated Power-Backed Hardware Across Multiple Verticals

Envirotech operates a diversified hardware technology platform focused on power management and electrification across commercial electric vehicles (EVs), medical supplies manufacturing through Maddox Industries, heavy-lift industrial drones, and emerging modular AI data infrastructure [S1].

The commercial EV segment targets fleet customers with Class 2–5 vehicles assembled domestically via a semi-knocked-down (SKD) model. Key vehicle components—including chassis and subassemblies—are sourced from OEMs in China, Taiwan, and Malaysia then integrated in Houston under proprietary specifications covering battery systems, telematics, and electrical architectures [S1,S24,S27].

The medical supplies segment leverages Maddox Industries’ semi-automated domestic manufacturing capabilities producing PPE and related products for government contracts supporting federal agencies. This unit validates Envirotech’s ability to operate regulated U.S.-based production environments [S1]

The drone initiative focuses on developing heavy-lift platforms for agriculture, forestry management, fire suppression—with emphasis on payload capacity, durability, regulatory compliance favoring U.S.-manufactured unmanned systems—and remains pre-commercial but engaged with refundable deposits from prospective customers [S1,S12,S19]

AI data infrastructure development launched in early 2026 aims at modular containerized compute systems combining localized power generation (including natural gas-based sources), thermal management technologies like liquid immersion cooling, and high-performance computing hardware tailored for grid-constrained or specialized industrial sites such as South Texas energy corridors [S1,S9,S26]

Revenue streams vary by segment: commercial sales plus service contracts in EVs; government subcontract fulfillment in medical supplies; future leasing or joint ventures anticipated for AI infrastructure; drone sales pending regulatory approvals [S1,S19]

Manufacturing Footprint Centralized in Houston

Since mid-2025 Envirotech consolidated operations into an approximately 86,000 square foot leased facility in Houston encompassing corporate headquarters alongside EV assembly lines, Maddox Industries’ medical supply production facilities, drone testing sites, logistics hubs, and warehousing [S16]. This geographic concentration enhances quality control over complex supply chains involving imported components balanced by domestic integration.

The SKD assembly strategy enables specification enforcement aligned with customer use cases controlling battery integration standards and software configurations—key differentiators against competitors relying solely on third-party imports without localized customization or integration oversight [S24,S27]. Medical supplies benefit from federal procurement standards mandating strict regulatory compliance that strengthens domestic sourcing credentials amid supply chain resilience priorities [S10].

Customer switching costs are supported by direct or qualified third-party maintenance networks critical for fleet uptime reliability.

Competitive Landscape: Commercial EV Challenges Amid Emerging Growth Areas

Commercial EV demand faces contraction driven by waning federal incentives post-2024 executive orders pausing Inflation Reduction Act programs supporting charging infrastructure coupled with sharply increased U.S. tariffs raising component costs (up to 100% tariff on Chinese EV parts) [S1,S5,S7]. These factors raise total cost of ownership adversely affecting price-sensitive institutional buyers such as fleets or municipalities historically reliant on subsidies.

Many smaller EV manufacturers have exited or downsized reflecting capital scarcity amid margin compression; market dynamics now favor selective use case deployments prioritizing ROI over broad electrification initiatives [S8]

Conversely, Envirotech’s drone systems target less saturated industrial niches requiring heavy payload capacities unmet by smaller foreign-dominated agricultural drones. Regulatory trends favoring domestic sourcing enhance competitive positioning alongside rugged design targeting fire suppression and forestry applications with advanced payload deployment capabilities [S8,S12].

The AI data infrastructure segment competes against large technology incumbents but benefits from structural bottlenecks around power availability and deployment speed demanding integrated solutions combining power generation with compute clusters—a niche aligning well with Envirotech’s hardware expertise though scale-up challenges remain significant [S26,S27].

Growth Drivers: Diversification into Medical Supplies, Drones, and AI Infrastructure

Maddox Industries offers revenue stability backed by ongoing government contracts serving as proof points for domestic manufacturing capabilities mitigating policy volatility risks seen elsewhere [S1,S10]. Contract renewals remain critical KPIs.

The drone program has secured refundable deposits signaling initial customer interest ahead of planned commercial production subject to regulatory clearances [S19,S23]. While opportunity exists in sizable addressable markets like agriculture and fire suppression, execution risk remains given undeveloped sales pipelines early in 2026

AI infrastructure development launched in early 2026 targets accelerating demand for power-backed modular data centers addressing energy-hungry workloads constrained by traditional grid expansion timelines—particularly in regions like South Texas where site evaluations have commenced [S26,S9]. Key performance indicators include demonstration project success validating cooling technologies (e.g., liquid immersion) alongside partnerships securing supply chains within capital discipline frameworks

Risks: Financial Constraints and Execution Uncertainties

Policy uncertainties around EV incentives combined with sustained high tariffs inflate input costs eroding margins within the commercial EV segment where competition persists but scale advantages favor larger players likely maintaining margin pressure [S7,S11]

Liquidity constraints are notable: as of March 31 cash & equivalents were approximately $2 million against total debt near $4.5 million yielding net debt about $2.5 million; current assets of $6.8 million versus current liabilities exceeding $18.3 million produce a low current ratio (0.37) indicating working capital stress risking covenant breaches absent improved cash flow or refinancing options [F1]

Execution risks accompany nascent ventures into drone manufacturing/sales and AI infrastructure development given capital intensity combined with long sales cycles typical of government contracts limiting near-term return visibility [S10,S11,F1]. Dependence on Maddox Medical contracts adds customer concentration risk plus regulatory audit exposure potentially causing revenue volatility or contract modifications impacting margins unpredictably

Failure to regain Nasdaq compliance risks delisting with reputational damage possibly constraining access to public capital critical for strategic pivots.

Upcoming Milestones & Watchpoints

- Nasdaq compliance plan submission due June 13 with potential extension through October pivotal for listing continuity and financing access [S3]

- Completion of operational consolidation into Houston by mid-2026 enhancing production efficiencies including medical supply ramp-up status [S1,S16]

- Progression through drone platform testing/validation including regulatory approvals enabling commercial manufacture aligned with refundable deposit conversion rates signaling market traction [S9,S12]

- Early validation milestones for modular AI compute prototypes focusing on power integration efficacy informing scaled rollout decisions [S26]

- Quarterly reviews of Maddox contract health emphasizing renewal status amid evolving federal procurement priorities determining base revenue stability.

These milestones frame the balance between urgent financial compliance needs versus strategic diversification execution.

Financial Position Brief: Liquidity and Capital Allocation Priorities

As of March 31, Envirotech held roughly $2 million cash against $4.5 million total debt resulting in net debt near $2.5 million; current assets stood at about $6.8 million compared to current liabilities exceeding $18.3 million yielding a constrained liquidity position reflected by a low current ratio (0.37) [F1]. This profile highlights working capital pressures limiting short-term financial flexibility.

Capital allocation is focused on stabilizing higher-margin segments such as medical supplies backed by government contracts while pursuing phased investments validating drone commercialization pathways and controlled modular AI compute system development rather than aggressive expansion within the contracting commercial EV sector facing tariff-driven margin compression [F1,S2,S7]. This approach supports diversification while managing solvency risks critical for sustained market presence.

Financial position in context

As of 2026-03-31, companyfacts shows $2mm in cash and equivalents and $5mm of total debt [F1]. The same snapshot implies net debt of roughly $3mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $7mm and current liabilities of $18mm imply a current ratio near 0.37x for 2026-03-31 [F1].

Disclaimer: This analysis reflects publicly available filings up to May 19, 2026 ([S1]-[S29], [F1]) without extrapolation beyond provided data or forward-looking forecasts. It is not investment advice.

Comments