Lakewood-Amedex Confronts Capital Constraints While Advancing Nu-3 Therapeutic Development

Latest quarterly update highlights liquidity challenges amid early-stage pipeline progress and strategic board reinforcement.

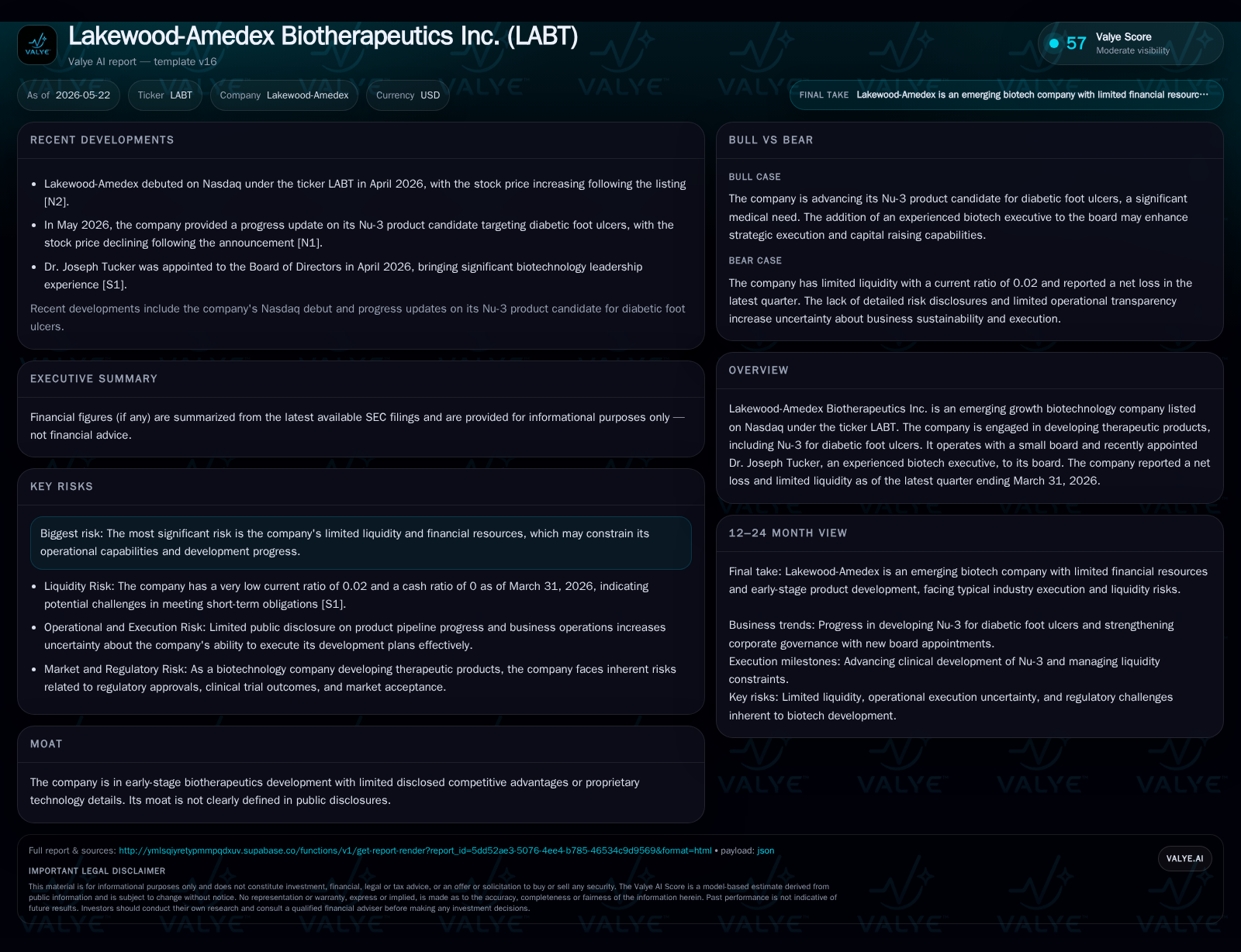

Lakewood-Amedex Biotherapeutics Inc. reported operational continuity alongside severe liquidity shortfalls in its latest quarter ending March 31, 2026. The company focuses on developing Nu-3, targeting diabetic foot ulcers, an area with significant unmet clinical need but intense competition and regulatory complexity. Recent board appointment of seasoned biotech executive Dr. Joseph Tucker potentially strengthens governance and capital-raising capabilities. However, constrained current assets relative to liabilities underscore the critical need for funding to sustain development activities.

Recent Operating Update

Lakewood-Amedex Biotherapeutics Inc. disclosed its latest quarterly results in the 10-Q filed May 22, 2026 [S2], revealing a challenging financial position characterized by a net loss nearing $0.9 million for the quarter ended March 31, 2026 [F1]. Cash and equivalents stood critically low at approximately $11,700 against current liabilities exceeding $3 million, producing an alarming current ratio of just 0.02 [F1]. This acute liquidity distress signals immediate funding needs to sustain operations. Despite the fiscal strain, the company continues advancing its lead therapeutic candidate, Nu-3, aimed at treating diabetic foot ulcers.

Complementing this financial snapshot was the appointment of Dr. Joseph Tucker to the Board of Directors in late April 2026 [S3]. Dr. Tucker’s extensive biotech industry executive background includes CEO roles at public biotechs and expertise in capital raises surpassing $100 million. His onboarding ostensibly intends to bolster Lakewood-Amedex’s strategic leadership and fundraising capabilities during this liquidity-constrained phase.

Business Model

Lakewood-Amedex operates as a development-stage biotechnology company primarily engaged in advancing proprietary therapeutics through research and clinical trials. Its revenue model currently depends entirely on external financing and potential licensing or partnership deals rather than product sales or commercial revenues.

The company's flagship product candidate, Nu-3, targets diabetic foot ulcers—a chronic complication afflicting patients with diabetes that causes high morbidity. The drug seeks to improve wound healing outcomes where existing treatments often fall short.

Revenue mechanics hinge on successfully progressing Nu-3 through costly phased clinical trials aligned with regulatory requirements set by agencies like the FDA. Upon receiving approval, potential revenues would derive from licensing fees or direct sales from proprietary formulations. However, until late-stage clinical validation occurs, expenses primarily represent R&D outlays covered by equity raises or collaborations.

Margins remain negative at this juncture due to substantial upfront investments without offsetting sales streams. Moreover, the pipeline's narrow breadth concentrates developmental focus—and corresponding risk—on Nu-3 while necessitating broader asset diversification long term to support growth.

Industry Structure and Competitive Position

The wound care market is both sizable and competitive with entrenched pharmaceutical players providing standard-of-care products while numerous smaller biotechs innovate in advanced biologics or regenerative medicine approaches.

In this ecosystem, Lakewood-Amedex’s competitive stance reflects an early-stage entrant reliant principally on one lead candidate without publicly disclosed proprietary platform or diversified therapeutics portfolio [N1]. They must navigate not only scientific complexities but also regulatory standards demanding rigorous safety and efficacy evidentiary thresholds.

Unlike larger peers possessing robust commercialization infrastructure or multi-product pipelines offering diversified revenue flow stability, Lakewood-Amedex currently occupies a high-risk position dependent on successful single-product development amid a capital-intensive landscape.

Growth Drivers

The primary growth vector is clinical advancement of Nu-3 through progressive trial phases validating efficacy for diabetic foot ulcer treatment [N1]. Positive clinical outcomes would enable regulatory submissions likely leading to commercial launch rights or partnership deals that introduce revenue streams.

Additional prospective catalysts encompass:

- Leveraging strategic alliances or licensing arrangements which could provide funding infusions critical for later-stage development or marketing support.

- Expanding therapeutic indications or augmenting product candidates via platform technologies if developed internally or via M&A.

- Effective capital structure management guided by experienced board members such as Dr. Tucker aimed at securing requisite financing under favorable terms.

Sustained investor confidence tied to these milestones can improve access to capital markets essential for growth bridging pre-commercial phases.

Risks and Growth Constraints

Liquidity risk stands foremost given current cash levels relative to obligations—failing timely fundraising could halt ongoing programs jeopardizing value creation [F1]

Regulatory risk inherent in biotherapeutics is substantial; unexpected trial failures or adverse data could derail timelines or termination outright.

Market adoption challenges post-launch depend heavily on differentiated therapeutic benefit versus established alternatives as well as market acceptance dynamics within provider reimbursement frameworks.

Operationally, limited scale constrains rapid expansion capabilities absent significant capital commitments or partnerships; as an emerging firm with modest infrastructure, execution risk remains elevated.

The highly competitive wound care segment's saturation means clear clinical superiority or unique therapy mechanism is vital to carving sustainable market share—details around Nu-3’s comparative profile are yet sparse.

What to Watch Next

Key short-to-medium term indicators include:

- Clinical trial progress reports on Nu-3 efficacy/safety endpoints potentially announced via press releases or SEC filings [N1].

- Developments in capital raising initiatives led by management and bolstered by new board expertise, crucial for alleviating liquidity constraints.

- Updates on strategic partnership discussions that may accelerate development timelines or provide non-dilutive funding channels.

- Regulatory feedback events impacting trial designs or approval probabilities informing investment risk assessments.

These milestones provide quantifiable signposts regarding operational execution velocity and financial sustainability.

Financial Profile Summary

Lakewood-Amedex displays financial characteristics typical among early-stage biotech developers: persistent operating losses aligned with R&D activities concentrated in product development without commercial revenues yet realized [F1].

The reported net loss approximated $923,000 in Q1 2026 while operating income was negative by about $887,000 [F1]. Cash reserves under $12,000 juxtaposed against roughly $3 million in current liabilities yield an extremely weak current ratio around 0.02 signaling urgent cash needs [F1]. This unsustainable working capital deficit necessitates imminent financing transactions to maintain research momentum and corporate viability.

Capital stewardship will be pivotal moving forward as continued top-line losses during developmental stages test investor patience before fruitful commercialization materializes.

This analysis is based solely on publicly available disclosures including recent SEC filings and news releases without forecasts or investment research views. It contextualizes Lakewood-Amedex Biotherapeutics Inc.'s current operational state within its developmental biotech framework highlighting critical business implications without projecting future outcomes.

Financial position in context

As of 2026-03-31, companyfacts shows $11709 in cash and equivalents [F1]. Current assets of $50626 and current liabilities of $3mm imply a current ratio near 0.02x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments