RRE Ventures Acquisition Corp. Faces Critical Balance Sheet Pressure after Fresh Public Offering

Following its May 2026 IPO, RREV reports severe liquidity imbalance with minimal operational detail, raising fundamental questions about its near-term viability and strategic clarity.

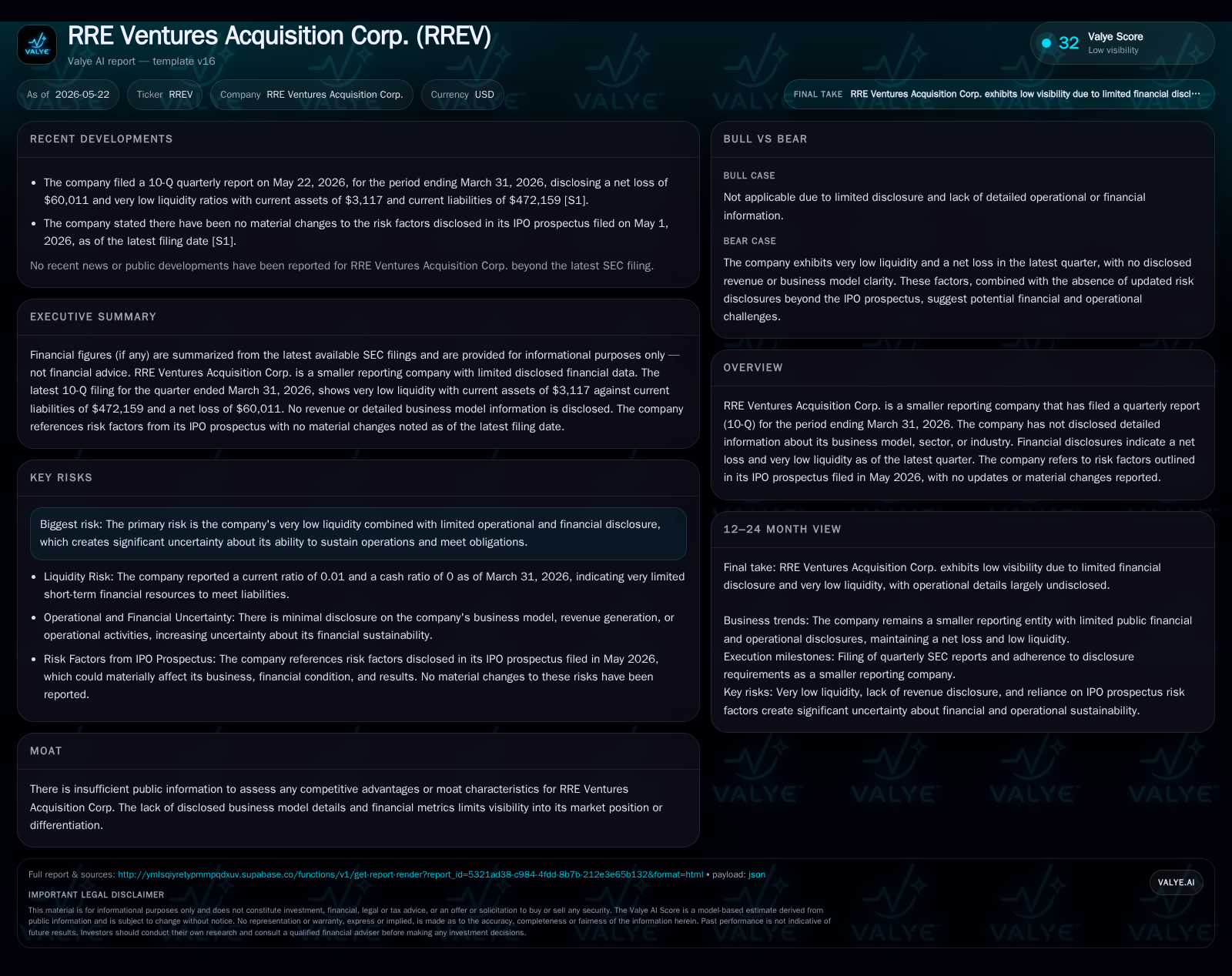

RRE Ventures Acquisition Corp., a special purpose acquisition company recently listed on Nasdaq, disclosed in its latest quarterly filing a stark liquidity shortfall paired with an ongoing net loss and sparse operational or business model disclosure. Despite raising $250 million in gross proceeds from its May 2026 IPO, the entity shows a current ratio of only 0.01 as of March-end, signaling critical balance sheet stress. The absence of concrete business updates or acquisition targets leaves the company’s growth trajectory and competitive positioning opaque, emphasizing the necessity for close monitoring of forthcoming material developments and capital deployment execution.

Latest Quarterly Operational Update and Its Significance

RRE Ventures Acquisition Corp.’s first quarterly report post-IPO (ending March 31, 2026) paints a precarious financial snapshot. Despite closing a $250 million IPO on May 1, 2026 [S9], as of quarter-end the company held current assets totaling a mere $3,117 against current liabilities of $472,159 — an extreme mismatch yielding a current ratio of approximately 0.01 [F1]. This indicates critical short-term liquidity pressure that is unusual even among blank check companies during their nascent phase.

Operationally, RREV recorded a net loss of $60,011 for Q1 2026 [F1], consistent with minimal expenses but no substantive revenue inflows. The filing reiterates previously disclosed risk factors from its IPO prospectus dated May 1, 2026 [S2], emphasizing that no material changes have occurred. Moreover, recent communications highlight the commencement of separate trading for Class A shares and warrants effective May 20, 2026 [S7], which may impact market dynamics for underlying securities but do not alter core cash constraints.

Overall, the lack of new operational disclosures beyond IPO closing formalities underscores continuing uncertainty regarding how RREV intends to deploy capital and progress toward revenue-generating transactions.

Business Model Ambiguity and Product/Service Overview

RRE Ventures Acquisition Corp. has not disclosed concrete elements of its business model or product/service offerings in filings through Q1 2026 [S2]. As a special purpose acquisition company (SPAC), it typically would serve as an investment vehicle designed exclusively to raise capital via an IPO for future acquisition(s) in unspecified sectors.

This absence of detail critically impairs traditional assessments of competitive advantages or unit economics since there are no customers generating revenue nor identifiable pricing mechanisms at this stage. The company neither reports segment information nor operational milestones beyond finance-raising events.

From an investor perspective accustomed to scrutinizing customer adoption patterns, pricing power, or regulatory moats in private equity-like structures, RREV’s nondisclosure translates into heightened reliance on sponsor credibility and deal flow quality projections rather than underlying operating metrics.

Competitive Landscape and Industry Positioning

Without disclosed business lines or portfolio companies under control, RRE Ventures Acquisition Corp.’s competitive context is best framed within the SPAC market ecosystem at large. This landscape is characterized by numerous publicly listed blank check vehicles seeking attractive private targets across sectors — often competing intensely for high-quality pipeline deals given limited sponsor capital availability.

Peers typically differentiate based on sponsor reputation, sector specialization (technology vs industrials), target geography focus, and transaction structuring expertise. However, RREV's lack of publicized strategic priorities or announced acquisitions means it currently holds little competitive positioning aside from being one among many newly launched SPACs post-IPO.

Its listing on Nasdaq alongside multiple warrant options aligns with standard SPAC issuance structures intended to provide investor optionality but does not confer distinct advantage absent clear execution signals.

Growth Drivers: Potential Catalysts and Assumptions

The primary growth vector for RRE Ventures Acquisition Corp., consistent with SPAC mechanics generally, hinges on successfully identifying and completing one or more acquisitions that create shareholder value post-combination. Progress toward such deals is critical:

- Deployment of IPO proceeds into target businesses offering scalable growth opportunities.

- Conversion of warrants lending potential capital influx upon exercise.

- Positive market reception post-share/warrant separation trading commencing May 20, which can enhance liquidity and valuation visibility [S7]

Absent explicit announcements about pipeline prospects as yet [S3], growth expectations rest on assumptions that management can swiftly consummate deals before capital depletion becomes acute given the reported tight liquidity profile.

Key Risks and Operational Challenges

RRE’s foremost risks stem from its balance sheet condition: current liabilities outstrip current assets by almost two orders of magnitude as per latest filings [F1]. Such illiquidity threatens solvency risks if anticipated acquisitions or additional financings fail to materialize timely.

Moreover:

- Operating losses recorded reflect early-stage status without internal cash generation capacity [F1].

- Dilution pressures exist given the significant warrant issuances both public and private placement forms following the IPO [S9; S10; S16].

- No material updates have alleviated initial risk disclosures from IPO prospectus filings including potential regulatory uncertainties tied to smaller reporting companies exempt from certain disclosure requirements [S2; valye_report_excerpt].

These factors together paint a cautionary framework around execution risk largely tied to external capital markets dynamics rather than operational fundamentals.

Monitoring Points: Upcoming Events and Milestones

Critical near-term indicators will illuminate whether the company can overcome structural constraints:

- Monitoring announcements around targeted acquisition candidates or strategic partnerships will be paramount to validate capital deployment rationale.

- Observing trading volumes and price behavior post-May 20 separate trading commencement could signal investor confidence shifts regarding warrant conversion impacts [S7].

- Watch for any material contractual developments relating to sponsor investments or changes in underwriting arrangements published via Form 8-K filings.

Such signals will inform shifts in risk/reward perceptions and influence secondary market valuations amid ongoing business model opacity.

Concise Financial Context: Snapshot of Liquidity and Operating Results

As restated from the most recent quarterly submission ending March 31, 2026:

- Current assets totaled only $3,117 contrasted sharply against current liabilities at $472,159 translating into a critical current ratio near 0.01 [F1].

- Net loss amounted to roughly $60k during this period aligning with foundational administrative expenses rather than substantive operations [F1].

- Total gross proceeds raised through IPO was approximately $250 million before expenses primarily allocated in trust accounts pending acquisition uses [S9].

Consequently, while headline fundraising appears strong on paper accompanying listing mechanics typical for SPACs [S9], immediate liquidity available for corporate purposes excluding trust-held funds is thin. The company remains heavily reliant on consummating planned acquisitions or additional financings to sustain ongoing viability absent operating cash flows.

Financial position in context

Current assets of $3117 and current liabilities of $472159 imply a current ratio near 0.01x for 2026-03-31 [F1]

This analysis synthesizes public SEC filings through May 22, 2026 along with structured Valye excerpts without extrapolation beyond supplied data. Given limited operational transparency inherent in SPACs pre-business combination stage, readers should apply heightened scrutiny to forthcoming disclosures that clarify RREV's path forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments