Spectral Capital Shifts Gears with Telecom-Focused Revenue Model

Latest quarterly results underscore a strategic transition toward recurring revenues from telecom operations, balancing ongoing IP development with commercial service delivery.

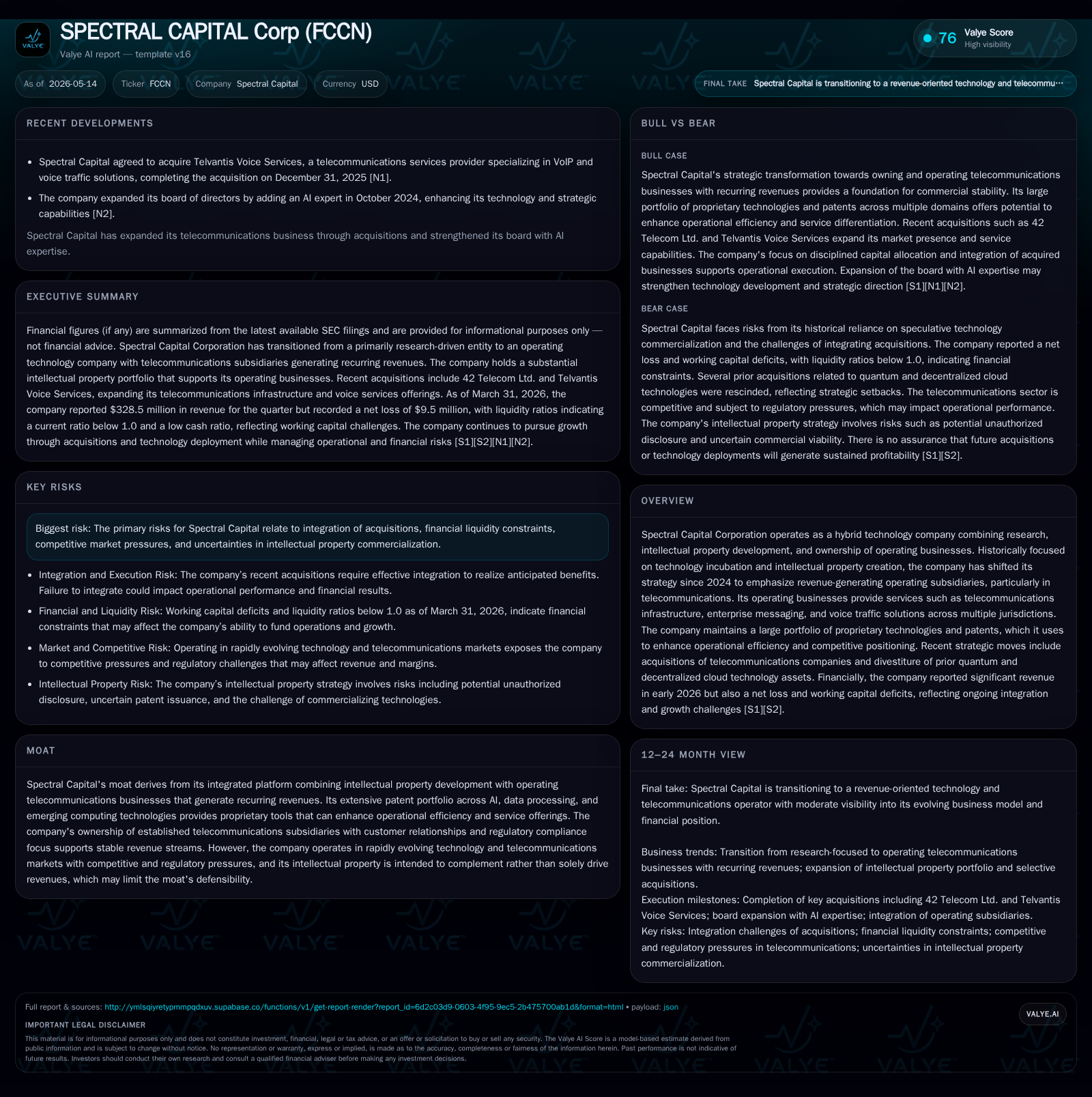

Spectral Capital’s Q1 2026 filing shows tangible progress executing its pivot from a speculative technology incubator into an operating telecommunications platform. The company now derives meaningful revenue from its telecom subsidiaries while maintaining a deep patent portfolio that supports operational efficiency and competitive positioning. Despite working capital challenges reflected in a sub-1 current ratio, Spectral’s integration of acquisitions like Telvantis and collection of legal judgments provide near-term operational traction. Growth hinges on expanding telecom services, cross-selling proprietary technology enhancements, and careful management of liquidity and integration risks.

Latest Quarterly Update: Evidence of Strategic Execution

Spectral Capital’s latest 10-Q filing for the quarter ended March 31, 2026 confirms the company’s material progress in executing its pivot towards operating telecommunications subsidiaries that generate recurring operating revenues [S2]. This marks a shift away from the company’s earlier profile as primarily a technology incubator reliant on speculative R&D outputs. The filing highlights stable revenue streams emerging from acquired telecom companies such as Telvantis Voice Services Inc., acquired at the end of 2025, now functioning as wholly owned subsidiaries with commercial contracts generating cash inflows.

These operational gains notwithstanding, the company continues to face integration challenges typical of recent acquisitions and notes legal proceedings inherent in the sector. Notably, a court judgment in favor of FortyTwo Telecom Ltd., a subsidiary, reinforces accounts receivable strength but remains subject to collection efforts. The filing does not report any substantial increase in debt levels but reflects working capital stress evidenced by a current ratio below 1.0 [S2],[F1]. Management reiterates discipline in cost control alongside regulatory compliance priorities essential for sustained service reliability.

Evolving Business Model: From Technology Incubator to Operating Telecom Platform

Historically focused on intellectual property development encompassing over 500 patentable innovations mainly in AI, data processing architectures, and hybrid computing systems, Spectral Capital has strategically recalibrated since 2024. Management transitioned the business from predominantly developing speculative software prototypes without significant recurring revenue toward owning and operating commercial telecommunications entities providing tangible enterprise messaging, voice traffic solutions, and infrastructure services across multiple jurisdictions [S1].

This model leverages proprietary technologies not solely as standalone revenue drivers but as performance enhancers to boost efficiency and competitive differentiation within the telecom operations. For instance, efficient routing algorithms or AI-driven network optimization tools embedded in subsidiaries’ offerings can improve margins while preserving service quality. This hybrid approach enables diversification away from patent monetization uncertainties toward stable subscription or usage-based revenue contracts maintained through regulatory adherence and long-term customer relationships.

Competitive Positioning in Telecommunications: Patents and Operational Footprint

Spectral’s competitive advantage arises from its integrated platform that combines an extensive intellectual property portfolio—with patents spanning AI-enabled data processing techniques—with direct ownership of regulated telecommunications businesses. Such subsidiaries benefit from licenses and compliance sanctioned by multiple jurisdictions granting market access otherwise difficult to achieve swiftly organically,[S1].

Nonetheless, competition remains intense both from large traditional telcos wielding scale advantages and agile technology providers offering commoditized voice or messaging services via cloud platforms. Spectral’s differentiated value lies in specialized services tailored for enterprise messaging needs where switching costs are heightened due to bespoke integrations or regulatory certifications required by customers. Further barriers include the complex regulatory environment which imposes operational overhead but simultaneously acts as a moat by limiting new entrants lacking requisite approvals.

Growth Catalysts: Revenue Expansion & IP Synergies

Key growth drivers for Spectral are anchored in expanding telecommunications across geographies matched with technology-enhanced product offerings. Cross-selling opportunities between subsidiaries allow bundled service deals while efficiencies gained through deploying patented technologies lower operating costs and improve scalability. Contract renewals secured from longstanding customers underpin recurring revenue visibility.

Additionally, management signals intent to pursue further disciplined acquisitions aiming to bolster telecom footprint or add complementary capabilities that can utilize existing IP assets practically. On the technology front, incremental inventions continue to undergo review processes for patentability; select breakthroughs may translate into licensing revenues or improved service features although management prudently refrains from forecasting specific IP-driven income [S1],.

External factors such as evolving telecommunications regulation potentially enable new service launches or expanded network capabilities fostering uptake among enterprise clients.

Risks and Challenges: Integration, Capital, and Market Pressures

Despite operational strides, significant risks remain. Most pronounced is the working capital deficiency highlighted by a current ratio near 0.85 driven by current liabilities exceeding assets at quarter-end March 2026 [F1]. Absent notable borrowings (only $10K total debt last measured mid-2025), liquidity must be managed carefully to avoid interruptions in service or growth initiatives.

Integration complexity of recently acquired entities like Telvantis carries execution risk including cultural alignment, systems harmonization, and regulatory hurdles in various jurisdictions [S1],[S3]. Legal contingencies persist relating to prior purchase agreements—such as Tellza litigation involving $250K—and collection uncertainties despite recent Maltese court wins for FortyTwo Telecom support caution.

Furthermore, the highly competitive landscape puts pressure on pricing and customer acquisition costs while rapid technological advances threaten obsolescence if innovation pipelines slow or capital constraints impede timely reinvestment [S1]. Reliance on financing markets introduces vulnerability should funding conditions tighten or capital raise timing mismatch operational cash needs.

What Investors Should Monitor Next

Investors should focus on forthcoming quarterly filings that will disclose post-integration performance of recent acquisitions with special attention to revenue growth trajectories and margin developments reflecting efficiency gains from deployed IP technologies [S2],[S3]. Resolution progress on outstanding litigations impacting cash flows will also be critical signals around risk mitigation.

Announcements related to geographic expansion plans or service diversification will help gauge management's success in leveraging the combined tech-operating platform advantageously. Moreover, any public guidance updates indicating shifts in capital allocation priorities or anticipated new contract wins would materially inform near-term outlook.

Current Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3mm | |

| 2026-03-31 | ||

| Current assets | $291mm | |

| 2026-03-31 | ||

| Current liabilities | $340mm | |

| 2026-03-31 | ||

| Current ratio | 0.85x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Date |

|---|---|---|

| Revenue (TTM) | $21.8M | |

| 2025-12-31 | ||

| Net Income | $0.92M | |

| 2025-12-31 | ||

| Cash & Equivalents | $2.7M | |

| 2026-03-31 | ||

| Total Debt | $10K | |

| 2025-06-30 | ||

| Current Ratio | 0.85 | |

| 2026-03-31 |

The company reported trailing twelve-month revenues around $21.8 million with net income positive at approximately $920 thousand reflecting initial stabilization amid transformation efforts [F1]. Cash reserves stand at $2.7 million against minimal recorded debt though current liabilities surpass current assets resulting in liquidity pressure requiring prudent working capital management moving forward [F1].

This analysis is based solely on publicly available filings and primary source evidence without any forward-looking statements or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments