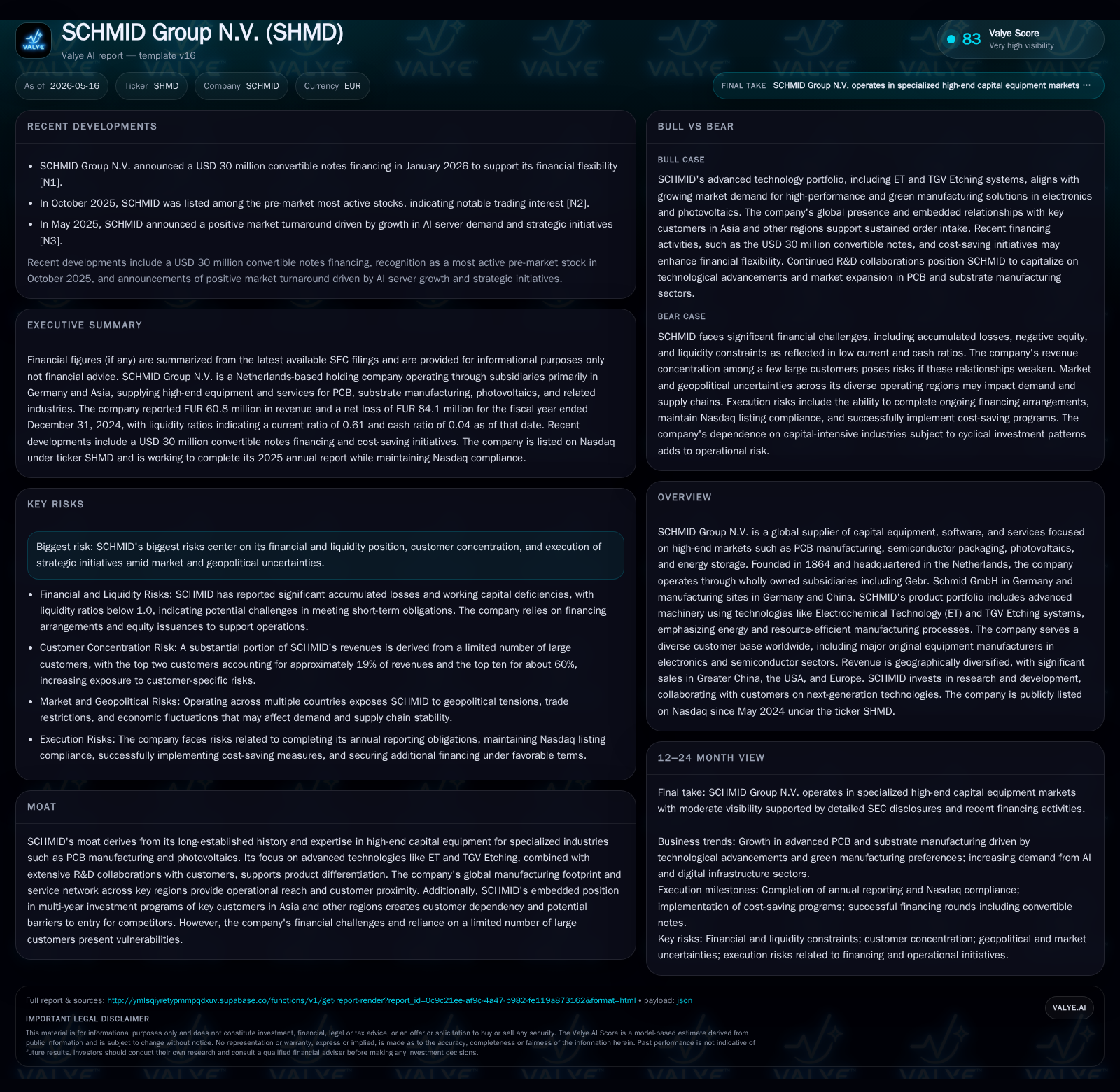

SCHMID Group’s Q1 2026 Update Highlights Capital Structure Shift and Technology Adoption

Recent financial liability offset agreements and convertible note conversions underpin SCHMID’s operational progress in advanced PCB and photovoltaic equipment.

In Q1 2026, SCHMID Group N.V. executed significant capital structure adjustments by entering offset agreements with family insiders to convert EUR 30.75 million of liabilities into equity, pending shareholder approval. Concurrently, institutional investors converted $12 million of convertible notes into shares, expanding SCHMID’s share base and reducing debt exposure. These moves stabilize liquidity amid a working capital deficit and support the company’s advanced technology offerings, including Electrochemical Technology and TGV Etching, critical for high-end PCB manufacturing and semiconductor packaging growth. Order backlog conversion and ongoing R&D collaborations indicate structural demand growth, though customer concentration and execution risks remain key watchpoints.

Q1 2026 Operating Milestones and Financial Restructuring

The latest quarterly disclosure dated April 27, 2026 [S2] reveals pivotal moves in SCHMID Group's capital structure aimed at stabilizing liquidity and preparing for growth acceleration. The company struck subscription agreements with key Schmid family insiders — Anette Schmid, Christian Schmid, Christine Schmid, and Schmid Grundstücke GmbH & Co KG — to off-set financial liabilities totaling EUR 30.75 million via issuance of new ordinary shares. This effectively converts debt owed to related parties into equity, subject to shareholder approval at the upcoming meeting scheduled for May 20, 2026. The share price for issuance will correspond to a five-day VWAP prior to board approval; however, a portion worth EUR 2.4 million (liabilities linked to Christine Schmid) will be priced at a 20% discount.

In parallel, institutional investors exercised conversion rights on senior convertible notes first issued in January and fully funded by March 2026 [S3], converting $12 million principal into approximately 2.2 million new shares. This increased total issued shares to roughly 57.8 million (including non-voting earn-out shares subject to price hurdles). Collectively, these transactions reduce leverage by replacing near-term liabilities with equity capitalization.

Simultaneously, SCHMID restored full compliance with Nasdaq listing requirements following overdue filings from prior years and is diligently progressing on its Form 20-F for FY2025 submission within SEC timelines [S2]. A shareholder vote will also consider adoption of a new share incentive plan granting up to 2.5 million shares for executive officers, directors, and employees — a strategic governance measure aimed at aligning incentives with long-term value creation.

These financial maneuvers serve as foundation stones enabling SCHMID to pursue its organic growth strategy in capital equipment markets while addressing prominent near-term liquidity constraints.

Decoding SCHMID’s High-Tech Industrial Equipment Business Model

SCHMID operates principally through Gebr. Schmid GmbH and subsidiaries delivering specialized capital equipment tailored especially for the high-end segments of printed circuit board (PCB) manufacturing, semiconductor packaging substrates, photovoltaics production lines, and energy storage solutions [S1]. Revenue streams arise not only from initial machinery sales but also from modular software upgrades, maintenance contracts, spare parts provisioning, training services across global sales centers (US, Europe, Asia), and project management support that together foster recurring revenue components.

Technologically differentiated offerings include advanced Electrochemical Technology (ET) leveraging precision etching processes that reduce resource consumption while elevating manufacturing throughput quality standards. The TGV Etching system – suitable for both small-scale laboratories and full-scale mass production – represents an innovative addition expanding addressable market scope considerably.

Integral to SCHMID’s model are collaborative R&D partnerships with leading original equipment manufacturers (OEMs), jointly developing next-generation electronics fabrication solutions that embed switching costs and build customer dependency over multi-year investment cycles. The company’s dual manufacturing footprint in Germany and China underpins cost competitiveness coupled with proximity advantages facilitating responsive service provision.

Competitive Edge in PCB and Photovoltaic Machinery Markets

Founded in 1864 with over a century-and-a-half tradition in precision industrial machinery development — transitioning from iron foundry roots — SCHMID commands established expertise within Europe and Asia’s PCM supply chains [S1]. Its specialization in high-performance ET systems situates it uniquely against competitors focused more heavily on conventional fabrication methods.

Competitors range from other European precision equipment manufacturers to Asian OEMs targeting cost-sensitive low-to-mid-tier segments; SCHMID’s investment in proprietary technologies like TGV Etching has broadened its differentiation vector beyond pure hardware into integrated process innovation.

Global market dynamics favor suppliers able to deliver energy-efficient production tools responding to escalating miniaturization trends driven by AI acceleration demands, edge computing infrastructure rollout (5G expansions), and rising IoT device volumes requiring exponentially greater PCB substrate complexity.

The firm’s expansive geographic sales network — complemented by partnerships such as AVACO in South Korea — promotes market penetration across major electronics hubs including Greater China (notably a sizeable revenue contributor), the USA, and Europe [S1].

Growth Opportunities from Electrochemical Technology Penetration

Internal management estimates foresee the share of capital expenditures devoted to ET-based factories rising significantly: whereas traditional fabrication methods account for approximately 20% of upstream equipment spending today, future ET-centric facility builds may command roughly half or more of these investments as technology adoption matures [S1]. Early revenue generation reported for ET technology during fiscal year 2024 validates underlying traction.

Demand acceleration is tightly linked to secular macro trends: ongoing digitization propels data volume growth necessitating enhanced storage capacities; pervasive AI workloads exacerbate computation needs; miniaturization mandates precision circuit manufacturing enhancements; sustainability imperatives pressure manufacturers towards energy-efficient tooling like ET systems.

Moreover, the TGV Etching system's dual applicability lends itself well to research institutions forecasting new product cycles as well as high-throughput contract manufacturers scaling production capabilities — broadening prospective client bases beyond incumbent OEMs [S1].

These credible growth drivers anchor optimistic multi-year topline expansion assumptions tied directly to factory capex conversion rates alongside sustained order momentum.

Financial and Execution Risks Underpinning Near-Term Outlook

Notwithstanding technological promise and operational initiatives implemented recently, several material risks could constrain execution:

- Liquidity metrics remain tight: as of end-2024 cash stood modestly at EUR ~3.8 million while current liabilities exceeded EUR 100 million resulting in a current ratio around 0.61 — indicating working capital deficiency that necessitates successful financing plan execution [F1][S2].

- Revenue concentration persists with two largest customers accounting for about 19% of revenues alone; ten largest represent some 60%, thus dependency on few key clients elevates volatility risk should any pullback occur [S1].

- Embedded derivatives sensitivity inherent in certain warrant liabilities introduces earnings volatility linked closely to share price fluctuations complicating forward guidance clarity [S13].

- Outstanding warrants present dilution risk ranging from exercise price triggers dependent partly on stock performance metrics which may affect existing shareholders’ interests adversely upon exercise.

- Execution risk exists surrounding timely shareholder approvals due May 20 required for share issuances related to debt set-off transactions alongside pay-for-performance incentive plan adoption which may influence governance stability.

- Geopolitical tensions impacting supply chains or capital spending decisions among OEMs could temper demand unexpectedly given SCHMID's international exposure across multiple economic zones [S20].

Overall risk management hinges on balancing near-term funding sufficiency with pace of order book realization alongside vigilant cost controls.

Milestones to Monitor: Order Book Developments and Shareholder Votes

Critical upcoming events include:

- The May 20 shareholders' meeting where votes on approving issuance of shares against existing financial liabilities (EUR ~30.75 million) will determine whether structural de-leveraging transactions proceed as planned [S2].

- Approval consideration of the new equity incentive plan aimed at attracting/retaining key talent through stock-based compensations reinforcing long-term alignment.

- Order backlog conversion trajectory currently pegged at EUR ~51 million per management forecasts represents an essential near-term operational KPI acting as leading revenue indicator; progress updates on order intake particularly related to ET technology machinery will validate demand assumptions [S5][S6][S12].

- Regulatory compliance maintenance vis-à-vis Nasdaq continuing listing conditions following recent remediation bolsters investor confidence but will require sustained transparency moving forward [S2].

- Monitoring of potential exercise activity regarding outstanding warrants issued concurrent with convertible notes financing provides insight into imminent dilution timing/theoretical share float expansion scope.

These milestones collectively form the operational cadence defining execution clarity in the subsequent quarters.

Financial Snapshot: Capital Structure and Liquidity Overview

As supported by disclosures through April 2026 filings:

- Cash & equivalents hovered near EUR

3.8 million at end-2024 with current assets totaling roughly EUR 60.8 million versus current liabilities approximating EUR 100.4 million reflecting constrained working capital liquidity ratios (0.61) exposed primarily due ongoing operating losses requiring financing actions [F1][S2]. - The subscription agreements signed on April 24 between SCHMID subsidiaries and family insiders aim at extinguishing EUR ~30.75 million financial liabilities via new share issuance pending shareholder nod thereby reducing short-term debt burden significantly while bolstering equity base structurally [S2][S22].

- Convertible notes raised USD $30M split equally between tranches were partially converted ($12M) by investors resulting in an increased share count (~57.8M total shares outstanding) diluting leverage but potentially contributing float volatility depending upon warrant exercises subsequently involved [S2][S3].

- Additional access was negotiated post-quarter (May ’26 SEPA agreement) granting discretionary rights to raise up to $30M more equity over two years providing optional capital flexibility managing interim liquidity needs should operational cash flows lag projections further [S5][S6][S22].

- Trade payables (

EUR 28M), loans from shareholders (EUR 21M), related party loans (EUR11M), warrant liabilities (EUR26M fair value) collectively underline complex liability structure demanding careful monitoring alongside embedded derivative valuations sensitive to market price variables [S8][S13][S23].

Judicious stewardship concentrating on converting backlog orders efficiently while accessing committed equity lines if needed shapes immediate solvency outlook.

Disclaimer: This analysis is based solely on publicly available filings as cited without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments