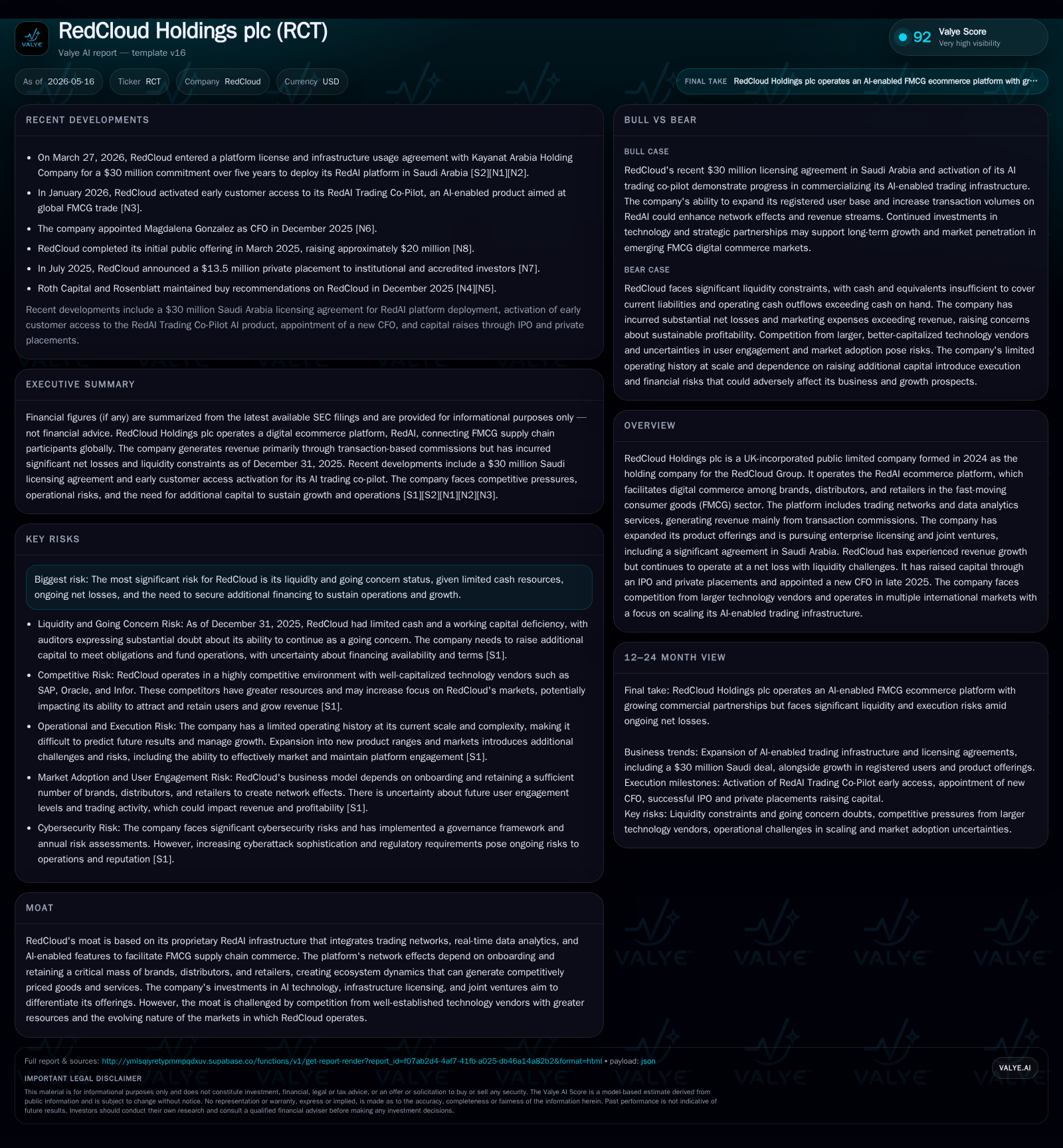

RedCloud Holdings Advances Saudi Arabia Expansion Amid Persisting Profitability and Liquidity Challenges

Recent licensing deal with Saudi partner marks a major platform deployment, while RedCloud sustains operational losses and funding needs.

RedCloud Holdings plc signed a five-year $30 million licensing agreement to deploy its RedAI platform infrastructure in Saudi Arabia with local partner Kayanat, signaling an important step for international expansion and revenue diversification. This license underscores RedCloud's strategic shift toward enterprise platform licensing alongside its transaction-commission ecommerce model focused on FMCG supply chains. However, despite generating $48.5 million in 2025 revenue with growth, the company reported a substantial operating loss exceeding $43 million that year and faces material doubt about going concern due to low liquidity and high short-term liabilities. The firm is actively pursuing capital raises through equity line of credit agreements and convertible notes to stabilize finances and fund growth. RedCloud's value proposition centers on its proprietary AI-powered digital commerce infrastructure, RedAI, which integrates trading networks and real-time analytics to orchestrate FMCG trade among brands, distributors, and retailers primarily in emerging markets.

Recent Operating Update

On April 14, 2026, RedCloud Holdings plc disclosed entering a significant platform license and infrastructure usage agreement with Kayanat Arabia Holding Company for the deployment of its RedAI ecommerce infrastructure in Saudi Arabia [S2]. This deal involves a commitment valued at approximately $6 million annually over five years, totaling up to $30 million. It encompasses technology enablement costs (localization, regulatory compliance) as well as operational services fees that will be paid based on revenues generated by the platform in the country. This milestone marks RedCloud’s first major enterprise license outside its existing emerging market clusters and leverages a joint venture framework established in August 2025 [S2]. The license deal points to the company’s strategic evolution from primarily transaction commissions within its digital supply chain platform toward an expanded licensing and joint venture model targeting new geographic markets.

Earlier in April 2026, shareholders approved expanding the maximum number of board directors to eleven and empowered the board to allot ordinary shares without pre-emption rights [S3]. These governance changes likely aim to facilitate future capital raising activities and strategic flexibility as the company pursues funding initiatives recently executed.

Business Model Overview

RedCloud Holdings operates through its proprietary RedAI intelligent infrastructure platform which facilitates digital commerce in fast-moving consumer goods (FMCG). The system connects three main user groups: brands (sellers), distributors (brokers/resellers), and retailers (buyers), enabling seamless transactions across trading networks Red101 and TradeX. Complementing this is RedInsights — an AI-driven data analytics service ingesting over 50,000 real-time market data points to optimize supply chain intelligence.

The firm's primary revenue streams stem from transaction-based commissions charged as a percentage of goods sold via its trading networks. Additionally, it is developing recurring revenue models through enterprise platform licensing — exemplified by the new Saudi Arabia licensing agreement — as well as pursuing joint ventures that extend reach and local operational capabilities.

A payments facilitation layer integrates established payment service providers tailored regionally in each operating country to enable seamless financial settlement.

This multi-component ecosystem aims to create network effects by onboarding a critical mass of FMCG stakeholders, providing real-time actionable insights, reducing trade friction costs through AI-enabled features (e.g., RAID - Realtime AI for Distribution engine), thereby attracting more users maintaining sticky ecosystem dynamics.

Industry Structure and Competitive Position

RedCloud occupies a specialized niche at the intersection of B2B ecommerce infrastructure for FMCG markets primarily in emerging economies including Nigeria, South Africa, Brazil, Peru, Argentina, now expanding into Saudi Arabia. Its competitive set ranges from large global technology platforms offering broad ecommerce or supply chain software solutions to local incumbents with traditional distribution networks.

The company's moat rests on the integrated nature of RedAI combining transactional marketplace functionality with advanced AI analytics embedded at supply chain nodes — features not yet commoditized widely among regional competitors. Proprietary technology such as RAID supports real-time demand forecasting and optimized distribution decisions that are critical in fast-moving sectors where margins are tight.

However, this moat is challenged by formidable incumbents with vast resources who can replicate components rapidly or bundle solutions within larger enterprise software suites. Moreover, the reliance on emerging market customers entails higher regulatory risks and currency volatility impacting financial stability.

Growth Drivers

- Geographic Expansion: The Saudi Arabia JV licensing deal signals entry into Middle Eastern markets beyond established Latin American and African footprints. This could open access to more stable regulatory frameworks and wealthier customer bases.

- Platform Licensing & Joint Ventures: Moving beyond transaction commissions enables predictable recurring revenues from large enterprise clients underwriting platform deployment costs.

- User Base Scaling: Increasing registrations across buyer-seller networks sustains transactional volume growth vital for commission income.

- Enhanced AI & Analytics Services: Continuous improvements in data services via RedInsights can increase customer dependency by driving measurable sales uplift.

- Payments Integration: Offering integrated payments processing tailors user experience improving retention rates.

- Strategic Partnerships: Collaborations like Kayanat bring local market knowledge aiding localization success mitigating execution risk.

Risks / Watchpoints / Growth Constraints

- Liquidity & Going Concern: The company ended 2025 with approximately $479k cash against current liabilities nearing $19.6 million, resulting in a current ratio of 0.27, indicating significant short-term liquidity risk [F1]. Despite recent financings including an equity line of credit facility ($30M) and senior convertible notes ($4M), sustained operating losses (~$43M in 2025) raise substantial doubt about continued operations without successful capital raises or rapid profitability gains [S1].

- High Operating Costs: Marketing commissions alone exceed revenue levels ($49M vs $48.5M revenue FY25), exerting severe margin pressure [S9]. Scaling efficiently remains critical.

- Foreign Exchange Exposure: Multinational operations expose earnings to currency fluctuations against GBP reporting currency affecting results unpredictably [S1].

- Competitive Pressure: Larger players with deeper pockets could erode pricing power or accelerate feature parity diminishing differentiation.

- Execution Risks: Localizing complex AI-driven systems across diverse regulatory environments requires ongoing investment; delays or deficiencies could impact uptake negatively.

- Customer Concentration & Retention: Success depends on sustaining participant networks; failure to maintain engagement undermines network effects crucial for economic sustainability.

What To Watch Next

- Implementation progress of the Saudi Arabia license agreement: milestones on platform activation rates, revenue recognition against annual committed fees [$6M/year], renewal negotiations post initial 5-year term [S2].

- Quarterly user growth metrics across all geographies indicating network expansion velocity; retention rates within trading networks detailed if disclosed [S13].

- Cost control efforts—particularly marketing spend rationalization—to improve unit economics relative to transaction volume growth trends [S9].

- Further capital raise outcomes under ELOC or other financing vehicles; debt amortization schedules given prominent debt load [S12][S19][S22].

- Impact or announcements regarding technological advancements within RedInsights or feature upgrades potentially improving competitive positioning.

- Management commentary on path toward sustainable profitability given persistent net losses despite increasing revenue base [S1].

Financial Profile Snapshot

Latest financial snapshot

FY ended 2025 |

These figures underscore operational scale paired with significant losses resulting from elevated marketing expenses and payroll amid rapid expansion efforts [F1][S1][S9]. Capital structure reflects heavy reliance on unsecured shareholder loans converted partly into equity but still featuring substantial near-term obligations [S6][S19].

This analysis synthesizes information available from recent regulatory filings reflecting public disclosures about RedCloud Holdings plc’s strategic initiatives including major contracts extending its AI-powered ecommerce infrastructure internationally while balancing liquidity constraints characteristic of aggressively scaling tech ventures still distant from profitability.

Disclaimer: This document is for informational purposes only based on publicly available filings as cited; it is not investment advice or recommendations.

Comments