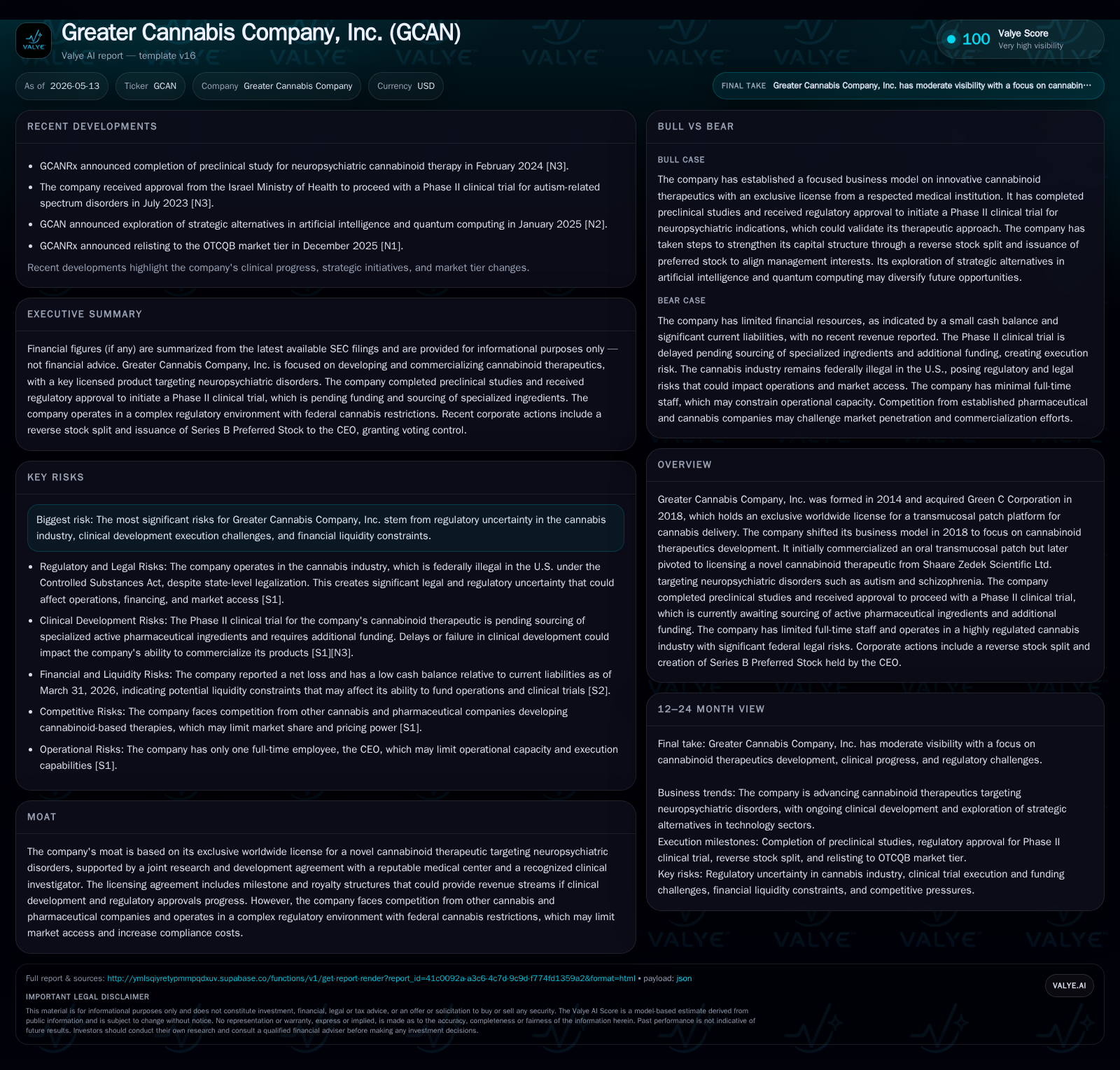

Greater Cannabis Company Advances Neuropsychiatric Therapeutics Amid Funding and Sourcing Challenges

The latest 10-Q reveals clinical trial delays and financial constraints as Greater Cannabis Company focuses on licensed cannabinoid therapeutics.

Greater Cannabis Company, Inc. reported in its most recent quarterly filing that it awaits procurement of specialized active pharmaceutical ingredients (API) to commence its Phase II clinical trial. This delay, coupled with necessary funding needs, has also led to the suspension of annual licensing fee payments. The company's strategic pivot from commercial cannabis delivery products to licensed cannabinoid therapeutics targeting neuropsychiatric conditions relies heavily on its exclusive worldwide license and joint R&D affiliation, but execution faces regulatory complexity and liquidity challenges.

Latest Quarterly Update: Clinical Trial Readiness and Financial Constraints

In the quarter ended March 31, 2026, Greater Cannabis Company disclosed critical developments impacting near-term operations. The company awaited sourcing of highly specialized active pharmaceutical ingredients (API) essential for initiating a Phase II clinical trial of their licensed cannabinoid therapy. This delay has effectively paused related milestone payments and licensing fees as no definitive timeline for API procurement is established. Additionally, management expects to secure further financing to cover anticipated costs of the clinical study expected to span 18 to 24 months once commenced [S2][S3].

Corporate restructuring was evidenced by a reverse stock split enacted at a ratio of one-for-1,500 shares effective October 16, 2025. This action significantly consolidated outstanding common shares aiming to enhance marketability and investor perception regarding equity value [S3][S13].

These operational realities underscore significant near-term execution risks compounded by strained liquidity metrics.

Evolution of Business Model and Technological Offering

Founded in 2014 but substantially reshaped after acquiring Green C Corporation in mid-2018, Greater Cannabis shifted from a preparatory phase characterized by commercializing its own transmucosal cannabis delivery patch towards focusing exclusively on developing licensed cannabinoid therapeutics [S1]. Green C’s acquisition brought an exclusive global license for a transmucosal patch platform initially deployed as an oral delivery system for cannabinoids absorbed through buccal mucosa. Despite limited commercial orders post-launch, management chose to pivot away from cannabis product commercialization towards therapeutic drug development marked by the October 2021 licensing agreement with Shaare Zedek Scientific Ltd. ("SZS")—the technology transfer entity linked to Israel's Shaare Zedek Medical Center.

This license grants Greater Cannabis exclusive rights to a novel cannabinoid therapeutic aimed at treating neuropsychiatric disorders such as autism spectrum disorder, schizophrenia, Parkinson’s disease, and Alzheimer’s disease. The arrangement is bolstered by a joint research and development agreement enabling the continuation of clinical programs led by Dr. Adi Aran, Pediatric Neurology Director at SZMC and co-inventor of the cannabis-based therapy [S6][S8].

The licensing contract stipulates staggered annual fees beginning modestly at $5,000 (starting third year after June 21, 2021), incrementing biennially up to $30,000 max. More substantial milestone payments are tied directly to clinical progress: $75,000 upon Phase II trial initiation, $200,000 at Phase III start, and $300,000 upon first regulatory approval for marketing a drug product. These milestones provide potential revenue triggers contingent on successful study execution [S1][S6].

Thus, Greater Cannabis’s business model has transitioned fundamentally into an R&D-driven therapeutic licensing platform with commercial upside hinging upon clinical validation of its proprietary cannabinoid compounds.

Competitive Dynamics in Cannabinoid Therapeutics

Within the fragmented cannabis sector — comprising cultivators, processors, consumer product makers, and delivery technology developers — Greater Cannabis occupies a niche focused on cannabinoid therapeutics for neuropsychiatric conditions using a specialized transmucosal delivery method. This differentiates it from many peers involved primarily in recreational or medical cannabis products.

However, incremental competition arises from pharmaceutical companies increasingly engaging cannabinoids' medicinal potential; among known competitors cited are Jazz Pharmaceuticals (NASDAQ: JAZZ) and Zynerba Pharmaceuticals (NASDAQ: ZYNE). These firms actively pursue cannabinoid-based treatments through more conventional pharma routes which may present hurdles around efficacy claims or regulatory acceptance compared to Greater Cannabis’s progressive but early-stage novel formulations [S11].

Regulatory constraints compound competitive pressures since cannabis remains federally classified as Schedule I in the US Controlled Substances Act. This classification restricts market access channels within the US federal regulatory framework while elevating compliance costs across state/federal divides—a pervasive limitation impacting all players in the licensed cannabis therapeutics space [S16].

Growth Prospects: Clinical Development and Licensing Revenue Potential

Future growth fundamentally depends on advancing through clinical development milestones that unlock staged payments per the Shaare Zedek license agreement. The recently approved Phase II trial represents a critical inflection point expected to trigger an initial $75,000 milestone payment upon commencement (currently delayed pending API availability). Successful completion would set the stage for Phase III trials tied to $200,000 further payment milestones.

Beyond these fixed fees lie longer-term royalty streams on the sale of dietary supplement products (capped at $100 million net sales with tiered royalty rates between approximately 2.25%–3%) as well as drug product royalties scaling up marginally from 1% toward 2% depending on sales volume thresholds [S3][S6]. Additionally, sublicensing options could enable broader market monetization if properly executed under regulatory-compliant distribution partnerships.

However, timelines are protracted with expected clinical study durations between 18–24 months followed by uncertain FDA review periods contingent on positive trial data availability—a prerequisite for initiating any formal regulatory submission process in the US.

Hence growth levers appear structurally plausible but tightly correlated with execution risk factors affecting timing and capital adequacy.

Key Risks: Regulatory Uncertainty, Funding Gaps, and Operational Execution

The company's positioning within a highly regulated and federally constrained cannabis industry poses ongoing legal risks regarding compliance burdens especially given evolving enforcement priorities articulated under DOJ guidance documents such as the Cole Memo [S16]. Federal illegality maintains an omnipresent overhang potentially affecting cross-border R&D collaborations and commercial exploitation even in medically liberal states.

Operationally Greater Cannabis manages minimal staffing resources — notably only one full-time employee serving as CEO — which constrains internal capacity for managing complex clinical programs or rapidly scaling administrative functions inherent in biopharmaceutical ventures [S4].

Financially, the company faces significant liquidity challenges given cash reserves of approximately $1,439 as of March 31, 2026, contrasted with substantially higher current liabilities [F1]. These factors highlight the need for additional financing to support planned clinical expenditures amid ongoing operating losses [S3]. The suspension of licensing fees due to delayed trial start further reflects fragile funding dynamics requiring external capital raising initiatives promptly.

Additionally reliance on key individuals such as Dr. Adi Aran for clinical leadership introduces concentration risk should principal investigator availability or contractual terms shift adversely.

Upcoming Catalysts to Monitor

Marketplace participants should track key upcoming transformative events including:

- Confirmation of API sourcing enabling formal commencement of Phase II clinical trials.

- Fundraising progress announcements crucial for financing multi-year clinical activities.

- Milestone payment realization reports following Phase II initiation.

- Updates on clinical trial enrollment completion dates providing insight into developmental timelines.

- Regulatory submissions timing post-trial results which will illuminate path towards FDA review initiation.

Each milestone functions as both an execution barometer and revenue trigger shaping future strategic flexibility.

Financial Overview: Liquidity Position and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1439 | |

| 2026-03-31 | ||

| Total debt | $171437 | |

| 2025-12-31 | ||

| Net debt | $169998 | |

| 2025-12-31 | ||

| Current assets | $1439 | |

| 2026-03-31 | ||

| Current liabilities | $776464 | |

| 2026-03-31 | ||

| Current ratio | 0 | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | 1,439 | |

| 2026-03-31 | ||

| Total Debt | 171,437 | |

| 2025-12-31 | ||

| Current Assets | 1,439 | |

| 2026-03-31 | ||

| Current Liabilities | 776,464 | |

| 2026-03-31 | ||

| Current Ratio | ~0 | |

| 2026-03-31 | ||

| Operating Income | -183,005 | |

| 2025-12-31 |

This snapshot underscores severe liquidity constraints juxtaposed against high current liabilities; negative operating income reflects ongoing investment stage operational losses typical of early-stage biotech/pharma ventures reliant on capital markets funding rather than self-sustaining cash flows.

Disclaimer: This analysis is based solely on publicly available information filed with the SEC up through May 13, 2026. It does not offer investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments