LIVE VENTURES Inc Q2 Unveils Mixed Profitability Amid Strategic Leadership Renewal

LIVE VENTURES reports revenue growth alongside net losses and extends key subsidiary CEO’s contract, highlighting operational focus with liquidity considerations.

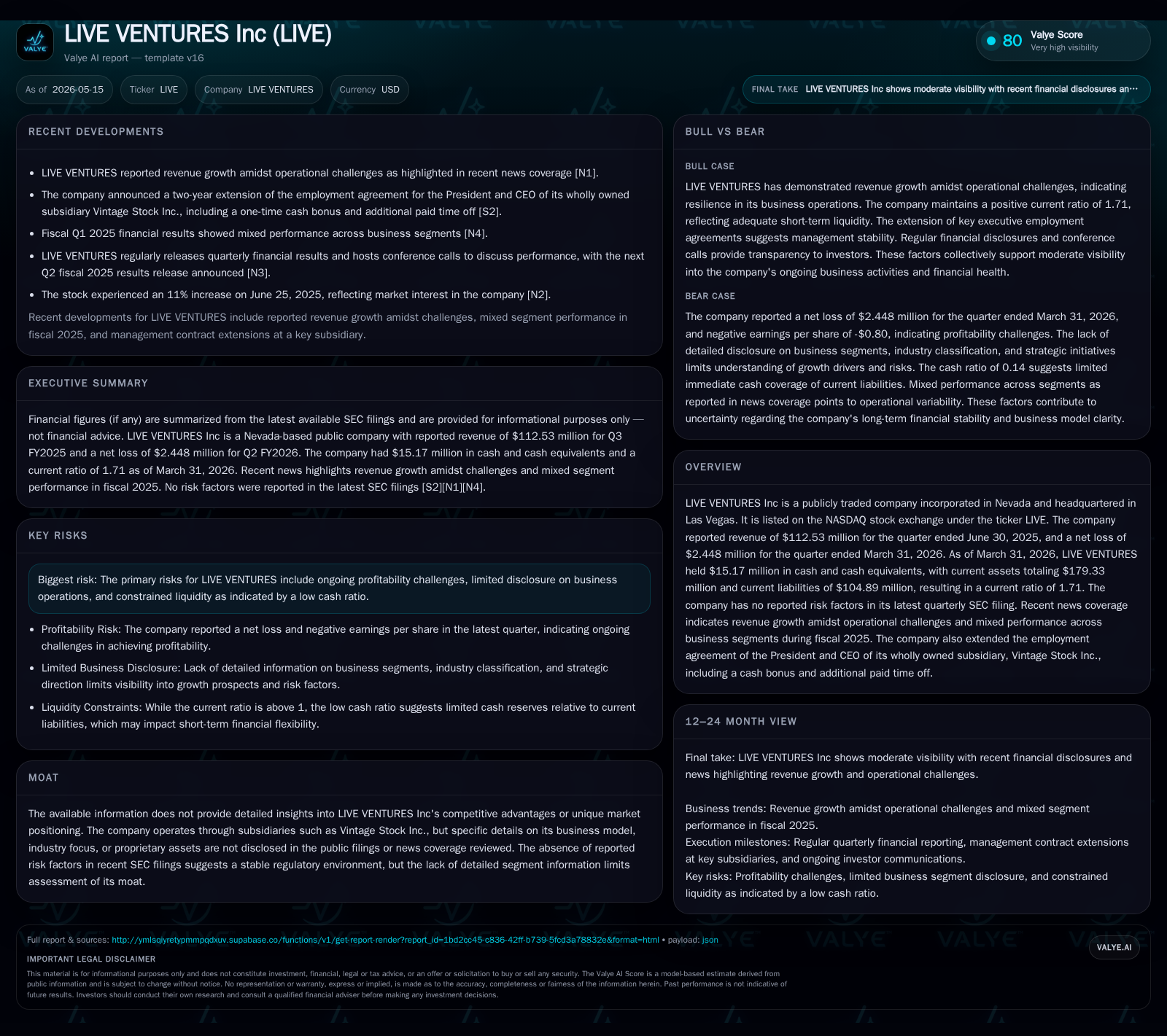

In its latest quarter ended March 31, 2026, LIVE VENTURES Inc reported $112.53 million in revenue but a net loss of $2.448 million, reflecting ongoing profitability challenges despite top-line growth. The company simultaneously secured leadership continuity by extending the employment agreement of Vintage Stock Inc.’s CEO through March 2028, underscoring a commitment to stabilize and enhance subsidiary operations. With a current ratio of 1.71 and cash reserves of $15.17 million, liquidity remains moderate but adequate for current obligations, positioning LIVE VENTURES at a crossroads of balancing growth initiatives against improving profitability.

Latest Quarterly Operating Highlights

LIVE VENTURES Inc’s most recent 10-Q filing dated May 14, 2026 reveals nuanced operational dynamics marked by top-line growth tempered by profitability challenges [S2]. The company generated $112.53 million in revenue during the quarter ended March 31, 2026 while recording a net loss amounting to $2.448 million [F1]. This marks continued progress from prior periods but underscores persistent pressures on operating margins and bottom-line results. Notably, the SEC filing discloses no new risk factors, signifying a stable regulatory environment and absence of emergent material concerns that might otherwise weigh on near-term outlooks [S2][S8].

Concurrently filed supplemental documents including an 8-K confirm these financial results and provide context for management’s strategic posture as LIVE balances growth ambitions against margin recovery efforts [S3]. This quarterly update serves as the clearest near-term barometer for LIVE’s performance trajectory during evolving market conditions.

Subsidiary Leadership and Employment Agreement Update

A critical strategic development impacting LIVE’s operational future is the extension of Rodney Spriggs’ employment agreement as President and CEO of Vintage Stock Inc., its wholly owned subsidiary [S9]. Effective March 31, 2026, the contract extends through March 31, 2028 with incremental benefits including a $250,000 one-time cash bonus payable shortly after renewal and an additional 80 hours of paid time off annually above existing entitlements [S9].

This contract renewal signals management’s prioritization of leadership continuity at Vintage Stock Inc., which is central to LIVE VENTURES’ revenue base. Retaining a seasoned executive like Mr. Spriggs provides stability during the backdrop of mixed segment-level performance experienced during fiscal year 2025 [S1]. It also reflects confidence in internal turnaround strategies focused on operational efficiencies rather than rapid expansion or diversification.

Given Vintage Stock’s significance within LIVE’s consolidated operations, this leadership renewal functions as a tangible offset to profit volatility and speaks to deliberate governance aimed at incremental value preservation.

Business Model Overview and Product Portfolio

LIVE VENTURES primarily operates through its subsidiaries with Vintage Stock Inc. serving as the flagship entity responsible for the majority of consolidated revenues [S1][F1]. While detailed segment disclosures remain sparse in public filings, available information positions the company within retail entertainment media — operating physical outlets coupled with some digital offerings that cater to niche collectors and entertainment enthusiasts.

Revenue generation is largely volume-driven via product sales channels supported by brand heritage from its affiliated entities. Pricing power appears modest given competitive pressures and product commoditization typical in consumer electronics or entertainment collectibles sectors.

Profit margins suffer accordingly due to cost structures that include inventory management expenses and operating leases inherent to physical retail footprints. Current profitability issues highlight room for refining unit economics whether through supply chain optimization or selective inventory rationalization.

Overall, LIVE’s business model hinges on leveraging legacy brand equity embedded in subsidiaries while navigating challenging retail industry headwinds characterized by shifting consumer preferences toward digital consumption.

Industry and Competitive Landscape Analysis

Within its competitive context, LIVE operates in a fragmented retail segment where players contend primarily on price competitiveness and assortments rather than defensible technology or patents [S1][S10]. Pricing pressure emerges from digital disruption reducing foot traffic across legacy brick-and-mortar venues.

The absence of any reported regulatory risks or litigation suggests that LIVE faces a neutral compliance landscape free from immediate external burdens [S2][S10]. Opportunities for differentiation may arise through curated merchandise offerings or exclusive partnerships managed at subsidiary levels but these have yet to markedly alter competitive positioning.

Capacity constraints are not explicitly reported; however, ongoing challenges balancing store-level productivity with fixed cost overheads remain implicit in profit difficulties cited across filings. Supply chain conditions appear stable without noted shortages or disruptions that would otherwise complicate inventory management.

Hence, LIVE's market positioning is more tactical—aimed at capitalizing on niche customer bases via veteran leadership execution rather than pursuing aggressive technological innovation or new markets.

Growth Trajectory and Demand Expansion Drivers

Future growth pathways for LIVE VENTURES stem principally from optimizing subsidiary operations rather than broad-based market expansion initiatives [S3][S9]. Revenue improvements hinge on deepening customer engagement at established stores and selectively improving inventory mix to enhance gross margins.

Retention efforts such as CEO Rodney Spriggs’ contract extension emphasize human capital continuity linked to execution capability—critical for driving operational discipline necessary for sustainable growth trajectories.

Absent evidence of major capital investments or diversification strategies in recent filings, growth prospects appear measured and dependent on internal efficiencies and possibly gradual digital channel enhancements aligned with evolving consumer behavior.

This suggests structural revenue uplifts tied closely to improvements in store productivity metrics or ancillary service offerings rather than rapid scaling through acquisitions or new verticals.

Risk Factors and Operational Constraints

Despite recent revenue gains, LIVE VENTURES continues facing headwinds manifesting as net losses that reflect lingering profitability issues rooted in cost structures and competitive pressures [F1][S2]. While the current ratio stands at a healthy 1.71 derived from $179.33 million in current assets against $104.89 million liabilities, cash levels totaling approximately $15.17 million introduce moderate liquidity constraints relative to scale [F1].

The company does not currently disclose material legal proceedings or heightened risk factors thus far suggesting manageable risk exposure under prevailing operating conditions [S2][S8][S10]. However, limited public disclosure on business segment details imposes analytical opacity making it harder to assess specific vulnerabilities within individual operating units.

Operational constraints likely revolve around balancing inventory turnover efficiency against maintaining broad product assortments demanded by collector communities—a challenge compounded by fixed retail infrastructure costs.

Profit margin improvement remains essential to shift the overall risk profile favorably while sustaining cash flow generation sufficient to fund ongoing working capital requirements without escalating leverage beyond manageable bounds.

Upcoming Catalysts and Monitoring Points

Key near-term milestones warranting close observation include forthcoming quarterly earnings releases which will shed light on margin progression trends and potential incremental reductions in net losses under renewed leadership frameworks [S3][S9].

Monitoring developments within Vintage Stock Inc.’s operations such as same-store sales metrics or inventory turnover rates can provide actionable signals regarding execution success attributed to strategic human capital retention.

Additionally, any corporate communications outlining shifts toward digital engagement models or changes in capital allocation priorities could materially influence growth outlook assumptions beyond organic subsidiary improvements.

Transparent disclosure enhancements around segment contributions would also materially enhance visibility into fundamental demand drivers.

Current Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $15mm | |

| 2026-03-31 | ||

| Current assets | $179mm | |

| 2026-03-31 | ||

| Current liabilities | $105mm | |

| 2026-03-31 | ||

| Current ratio | 1.71x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot encapsulates LIVE VENTURES’ capacity to meet near-term obligations with liquid assets complemented by working capital cushions reflective of a stable yet cautious financial posture [F1]. The approximate net debt position (total debt minus cash) remains elevated relative to earnings capacity indicating leverage considerations rooted partly in legacy investments predating the latest quarters [F1].

Such financial metrics corroborate observed operational themes: sufficient liquidity buffer mitigates immediate solvency concerns but pressure exists to optimize cash flows through profitability gains if sustainable enterprise value creation is to be achieved.

Disclaimer: This analysis is based solely on publicly available information as disclosed by LIVE VENTURES Inc through SEC filings up to May 14, 2026 ([S1], [S2], [S3], et al.) and companyfacts data ([F1]). It does not constitute investment advice or recommendations. Readers should consider company disclosures comprehensively before forming assessments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments