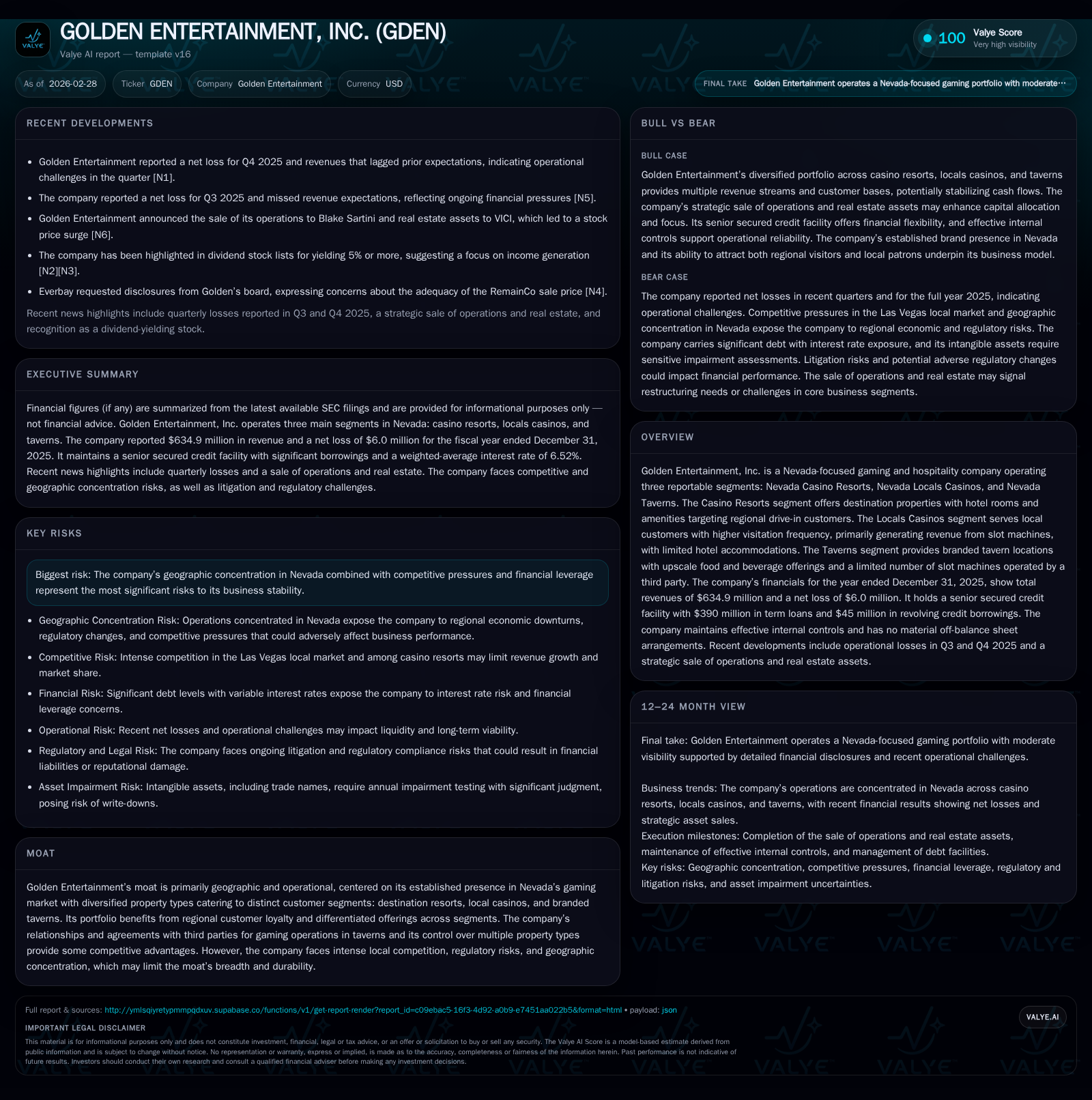

Golden Entertainment Confronts Profit Pressure Amid Shifting Local Gaming Dynamics

Golden Entertainment’s financial performance reflects the challenges of geographic concentration in Nevada combined with evolving segment demand and strategic capital decisions.

After years of robust growth fueled by a diversified Nevada portfolio spanning casino resorts, locals casinos, and taverns, Golden Entertainment faced a revenue decline and net loss in 2025. The company’s $635 million revenue represented a nearly 5% dip year over year, pressured by shifts in gaming visitation patterns and competitive saturation within its core market. Maintaining leverage at approximately $435 million under its senior secured credit facility, Golden prioritized disciplined capital allocation including continued dividends and share repurchases despite earnings pressure. Regulatory complexities and operational headwinds constrain near-term outlook while segment-level performance suggests evolving customer dynamics across its property types.

Historic Growth Trajectory and Operational Drivers Through 2025

Golden Entertainment experienced significant expansion over the past decade, growing annual revenues from approximately $58 million in FY2014 to a peak above $666 million in FY2024 before experiencing a decline to about $635 million in FY2025 — marking a -4.8% year-over-year contraction [F1]. Operating income similarly exhibited volatility: after peaking at $399 million in FY2023, operating income fell sharply to $112 million in FY2024 and further down to just over $21 million in FY2025, an 80.8% decrease [F1]. Net income mirrored this trajectory with gains through FY2023 followed by a plunge into a net loss of roughly $6.0 million in FY2025 [F1].

The initial growth was driven primarily by Golden's expansion within Nevada’s gaming sector, capitalizing on regional drive-in resort customers alongside locals who frequented the company’s casino properties regularly. These were complemented by branded tavern operations offering upscale casual environments with modest slot machine presence operated under third-party agreements starting recently [S16], [S18]. Early profitability benefitted from strong slot handle volumes particularly within Locals Casinos which produced repeat visitation, albeit with smaller average spend per visit than resort guests.

Margin compression preceding the 2025 losses signals intensifying competitive pressures during Nevada's mature gaming landscape. Costs related to property upkeep, wage inflation due to legislated increases, and marketing toward differentiated customer segments have offset revenue gains despite steady top-line figures until the latest yearly downturn [N1], [S10].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 635 | -6 | 83 | 22 | -4.8% | -111.9% |

| 2024 | 667 | 51 | 92 | 112 | -80.2% | |

| 2023 | 256 | 119 | 399 | +210.6% | ||

| 2022 | 82 | 150 | 148 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 26 | 22 | 36 |

| 2024 | 21 | 92 | 42 |

| 2023 | 58 | 9 | 33 |

| 2022 | 51 | 99 |

Source: SEC companyfacts cache [F1].

Note: Operating income YoY % provided only where data is available; earlier years omitted due to unavailable comparable data.

Segment-Level Performance Shifts: Casinos vs. Taverns

Golden segments its operations into three key buckets: Nevada Casino Resorts targeting regional drive-in visitors with extensive hotel accommodations; Nevada Locals Casinos catering to high-frequency slot players primarily from local customer bases; and Nevada Taverns featuring upscale casual venues with limited slot machines now operated via third-party agreement [S16], [S18], [S23].

While resorts generate longer stays albeit less frequent visitation compared to locals casinos where weekly visits are common due to proximity and demographic factors, revenue generation skewed towards slots play especially within the locals segment drives much of the topline gains historically. The slot handle — total amount wagered — is a vital metric impacting gaming yield (revenue per unit wagered), which for Golden has faced compression due to increased competition among local markets and saturation effects [S16]. Taverns’ outsourcing of slot operations reduces direct operational costs but alters the revenue recognition model to a share-of-revenues basis rather than pure gaming win.

In recent periods the Locals Casinos have borne the brunt of slowing demand shifts while Casino Resorts maintained relatively stable occupancy but faced fluctuating hotel utilization impacted by transportation cost pressures within Nevada’s travel corridors [N1]. The tavern segment benefits from food & beverage sales more than gaming yield given limited machine counts under third-party operation.

Geographic Concentration: Strength or Vulnerability?

Golden Entertainment’s entire portfolio is concentrated exclusively within Nevada markets comprising Las Vegas metropolitan areas as well as Laughlin and Pahrump regions [S16], [S19]. This concentration produces several advantages including brand awareness anchored in local communities alongside operational synergies across property types fostering customer loyalty — aspects fortifying its moat [N1].

However, this geographic focus simultaneously heightens exposure to adverse regulatory shifts such as minimum wage hikes—currently unpredictable yet impactful—environmental laws mandating costly compliance actions particularly involving historical land use contamination risks and evolving responsible gaming legislation enforcing promotional standards [S10], [S19]. Market saturation is also notable particularly for Locals Casinos where visitor overlap between competitive regional operators compresses room for expansion without cannibalization risks.

Furthermore, external factors such as transportation capacity constraints limiting visitor inflow exacerbate competitive headwinds given limited alternative markets geographically accessible for expansion or diversification within Golden’s current operating paradigm.

Capital Structure Evolution and Leverage Impact

As of December 31, 2025 Golden carried approximately $390 million in principal Term Loan B-1 borrowings plus an additional $45 million outstanding on its revolving credit facility out of available revolver capacity totaling $240 million [S4], [S7]. The weighted-average effective interest rate stood at about 6.52%, reflective of variable rate exposure tied primarily to Term SOFR benchmarks plus margins adjusted by leverage ratios [S4], [S11].

The Term Loan B-1 amortizes through fixed quarterly installments of $1 million starting September 2023 culminating in a sizeable maturity payment nearing $373 million due May 2030 [S4]. Covenants embedded restrict further indebtedness beyond defined limits plus impose constraints on liens granting asset collateral rights alongside caps on dividends or share repurchases potentially limiting discretionary capital usage [S9], [S20].

While operating cash flows exceed interest expense comfortably based on reported figures ([F1] CFO ~$83M vs implied interest), rising rates or cash flow deterioration could pressure refinancing strategies or growth investments necessitating prudent leverage management.

Dividend Policy and Share Repurchase Trends

Golden initiated quarterly cash dividends at $0.25 per share commencing February 27, 2024 maintained through at least September 30, 2025 totaling dividends paid around $26.3 million for FY2025 as per disclosures [N2], [F1], [S5], [S24]. This dividend level represents an enduring commitment despite recent profitability pressure signaling strategic prioritization of investor returns.

Share repurchase activity continued albeit reduced from prior years with expenditures totaling approximately $22.3 million in FY2025 against a Board-authorized cumulative program initially set at $100 million then supplemented by an additional $100 million authorization through late 2024 iterations [F1], [S8]. Shares were mainly retired post repurchase supporting EPS accretion potential once profitability normalizes.

This capital return approach balances sustaining market presence amidst shrinking earnings while deploying excess free cash flow estimated near $35.6 million (operating cash flow minus capex) cautiously aligned with covenant flexibility parameters discussed previously.

Regulatory Environment and Its Influence on Future Prospects

The company explicitly acknowledges multifaceted regulatory risks including potential legislation expanding or restricting gaming permissions locally or federally that could materially affect operations if enacted unfavorably [S10], [S19]. Responsible gaming initiatives form an integral marketing pillar with investments exceeding $400k since inception toward community programs emphasizing healthy gambling norms accompanied by self-exclusion options mitigating social liabilities.

Labor cost inflation risk remains elevated given periodic minimum wage escalations mandated through state statutes complicating labor expense forecasting alongside compliance costs tied to environmental remediation obligations linked historically acquired properties possibly contaminant-laden as per federal/state environmental rules enforcement standards [S10], [S25]. Marketing practices face scrutiny under tight legal frameworks preventing targeting minors or high-risk individuals underscoring operational vigilance needs.

These variables collectively suggest adherence cost creep will factor materially into expense forecasts constraining margin recovery absent parallel revenue acceleration strategies.

Key Financial Indicators To Watch Moving Forward

Monitoring stabilization—or ideally reversal—of revenue declines across the three primary segments will be critical given recent negative trends documented for FY2025 quarterly periods encapsulated within recent reports [N1], coupled with close attention on gross gaming revenues influenced by slot win hold rates—a key metric signifying proportionate player wagers retained as revenue often sensitive to macroeconomic swings.

Interest coverage ratio development affects debt service resiliency especially under changing interest rate regimes interlinked with the variable rate debt structure described above; deterioration here would signal covenant breach risks or refinancing difficulties.

Free cash flow preservation near current levels around mid-$30 millions offers runway for balancing dividends plus opportunistic share buybacks facilitating shareholder value returns while buffering against operational volatility.

Return on equity currently negative (-1.4%) highlights net losses generated relative to sizable equity base accrued primarily via retained earnings growth originally—recovery herein remains contingent upon margin improvement amidst structural expenditures rationalization ([F1]).

Operational Challenges Tempering Near-Term Outlook

Seasonality typical in hospitality sectors combined with intensified competition has led to visitor segmentation changes wherein locals versus destination guests show differential spending patterns influencing utilization particularly at casino resorts where hotel occupancy metrics exhibit sensitivity not fully offset by ancillary amenity revenues so far documented post-pandemic era uncertainties influencing travel habits temporarily restrictive toward extended stays ([N1], [S3]).

Additionally cannibalization risk among overlapping market customer pools between company properties necessitates calibrated marketing expenditure deploying sector-native optimizations like dynamic player reinvestment frameworks focusing disproportionately toward higher-yield customers balancing volume against yield tradeoffs effectively.

Maintaining compliance amid expanding regulatory overlays adds complexity elevating internal controls burden thus requiring ongoing investments that further press margins despite scale advantages otherwise expected from integrated multi-property operating platforms within Nevada markets.

This analysis focuses exclusively on factual information disclosed through SEC filings and recent news releases without providing investment advice or forward-looking recommendations regarding Golden Entertainment's securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments