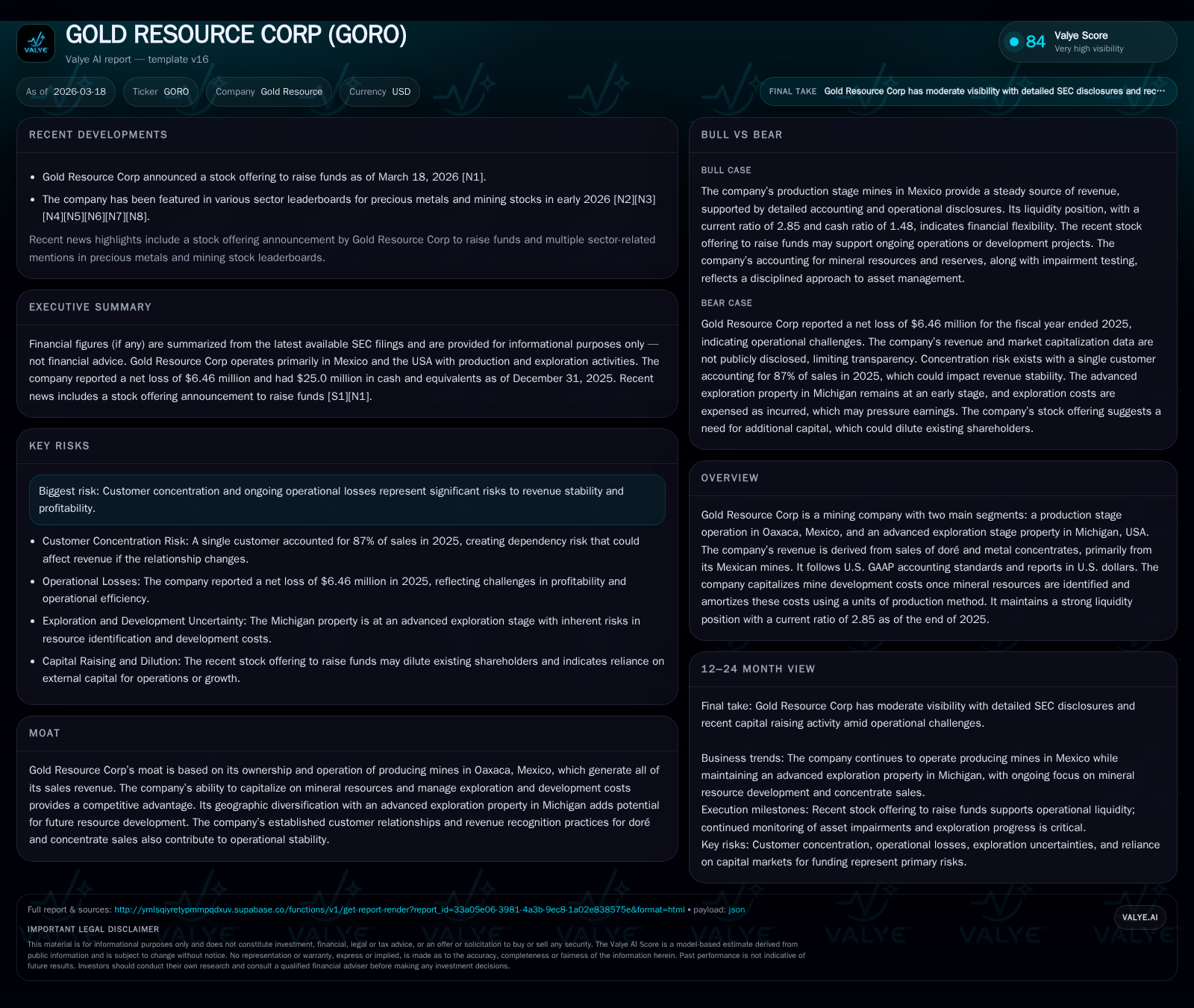

Gold Resource Corp Navigates Operational Challenges and Strengthens Liquidity Amid Strategic Transition

Declining ore grades and metal recoveries at Oaxaca operations in 2025 weighed on production and profitability, while a successful stock offering enhanced liquidity to support ongoing development and exploration.

In 2025, Gold Resource Corporation faced reduced ore grades and metal recoveries at its Arista underground mine in Oaxaca, Mexico, resulting in lower processed volumes and continued operating losses despite significant year-over-year improvement. The company raised approximately $7.5 million through a registered direct stock offering in early 2026, boosting cash reserves to $25 million and improving its current ratio to 2.85. Operating cash flow turned positive at $21.7 million, offsetting increased capital expenditures of $21 million aimed at sustaining development. Customer concentration risks intensified as one buyer accounted for 87% of sales in 2025. The advanced-stage Michigan exploration project remains a potential growth avenue, while a pending merger with Goldgroup Mining Inc. adds strategic complexity. Key focus areas include post-blockade operational recovery, Back Forty project permitting progress, and commodity price impacts on revenue.

Operational Overview: Production and Grade Variability Impacting Output

Gold Resource Corporation's primary operating asset remains the Don David Gold Mine (DDGM) in Oaxaca, Mexico, where the Arista underground mine accounted for all precious metal production during fiscal year 2025 [S1]. Processing throughput declined with tonnes milled decreasing from approximately 356,633 in FY24 to about 271,404 in FY25, reflecting operational constraints including ore availability and processing capacity utilization [S1].

Ore quality deteriorated notably as average gold grades dropped from 1.13 grams per tonne (g/t) to 0.85 g/t while copper grades fell from 0.26% to 0.16%. Conversely, silver grades increased substantially from around 92 g/t to approximately 217 g/t; this likely reflects geological variability rather than an operational improvement [S1]. Metal recovery rates also softened mildly with gold recovery declining from an average of 76.6% to about 71.5%, and silver recovery slipping from roughly 87.5% to near 84.4%, further affecting payable metal output volumes [S1].

These factors combined led to reduced contained precious metals available for sale despite efforts to maintain milling rates (Tonnes Milled per Day decreased slightly from ~1,277 to ~1,191). Such grade variability is typical in polymetallic underground mining operations where selective mining influences feedstock quality and processing efficiency [S1]. Lower base metal grades (lead and zinc) also contributed to diminished polymetallic concentrate value.

Financial Performance: Narrowing Losses during Operational Headwinds

The operational challenges translated into financial results showing significant improvement but persisting losses:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -6 | 22 | -3 | 21 | +88.6% |

| 2024 | -57 | -1 | -47 | 8 | -252.8% |

| 2023 | -16 | -5 | -22 | 12 | -153.4% |

| 2022 | -6 | 14 | 2 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | -14.7 | |

| 2024 | -8 | -207.1 | |

| 2023 | 4 | -18 | -16.6 |

| 2022 | 4 | -4 | -5.7 |

Source: SEC companyfacts cache [F1].

Despite negative operating income of approximately -$3 million for FY25, this marked a substantial reduction compared with the prior year's much larger loss [F1]. Net loss similarly narrowed significantly though remained negative due primarily to non-cash charges and lower revenues amid grade declines.

Operating cash flow rebounded strongly into positive territory at $21.7 million after years of negative cash generation, driven by improved working capital management alongside operational improvements [F1][S9]. Capital expenditures more than doubled year-over-year to over $21 million reflecting investments in mine development infrastructure and equipment commitments totaling around $4.3 million by year-end [F1][S6].

Return on equity stayed negative at an estimated -14.7%, consistent with ongoing net losses despite equity growth fueled by share issuances [F1]. Free cash flow—operating cash flow less capital spending—was modestly positive near $644k indicating limited excess funds after reinvestment needs.

Capital Structure and Liquidity: Strengthening Financial Flexibility

Liquidity improved markedly during the period supported by both operational cash flows and financing activities:

- Cash & equivalents surged from $1.6 million at end-2024 to $25 million at end-2025.

- Current ratio improved substantially to approximately 2.85 reflecting stronger current assets relative to liabilities.

- The company repaid a $6.28 million working capital loan ahead of maturity using proceeds from a registered direct stock offering completed in early Q1 2026 that raised about $7.5 million gross proceeds before costs [N1][S6][F1].

This enhanced liquidity position supports ongoing working capital needs as well as continued capital investment programs critical for sustaining production levels amid geological variability challenges.

Customer Concentration: Elevated Risk Due to Revenue Dependence

A notable risk factor is the pronounced concentration of sales revenue among a small number of customers:

- One customer accounted for approximately 87% of total sales revenue during FY25 compared with just 19% the prior year.

- Another customer’s share declined significantly during this timeframe [S8][S19].

This concentration elevates credit risk exposure and dependency vulnerabilities should disruptions or renegotiations arise affecting these key relationships.

Growth Prospects: Michigan Exploration Project and Merger Developments

Geographically diversified growth opportunities include the advanced-stage exploration project located in Michigan which remains non-producing but holds potential contingent on successful permitting and financing milestones ahead [S23][S18].

Strategically transformative is the announced definitive merger agreement dated January 26, 2026 under which Goldgroup Mining Inc intends full acquisition of Gold Resource Corp shares [N1][S1]. This pending transaction introduces prospects for portfolio realignment including integration of stream agreements liabilities exceeding $90 million tied primarily to the Back Forty Project alongside contingent royalties linked to project development progress [S20][S23].

Outlook and Key Monitoring Points

Stakeholders should monitor several critical developments moving forward:

- Resumption of full mining operations post-blockade lifting early in FY26 with attention toward stabilization of tonnage milled per day and ore grade metrics reported quarterly [N2][S3].

- Progression milestones related to the Back Forty project’s feasibility study completion and permitting status which are prerequisites for commercialization.

- Capital expenditure trends focusing on equipment procurement exceeding $4 million highlighting expansion priorities.

- Sensitivities associated with fluctuating commodity prices impacting provisional pricing mechanisms embedded within accounts receivable valuations disclosed quarterly [S13][S14].

- Merger integration outcomes including any material changes in capital structure or realization of cost synergies anticipated post-acquisition announcement.

These factors collectively will shape Gold Resource Corp’s ability to navigate present operational challenges while pursuing longer-term growth opportunities amid evolving market conditions.

Disclaimer: This analysis is based exclusively on publicly filed documents through March 18, 2026 ([F1],[S#],[N#]) without any speculative projections or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments