Wellgistics Health Grapples with Integration and Financial Strains Amid Expansion of Specialty-Lite Pharma Ecosystem

The company's micro health ecosystem approach targets specialty-lite pharmaceutical markets but faces sizable integration, regulatory, and liquidity challenges.

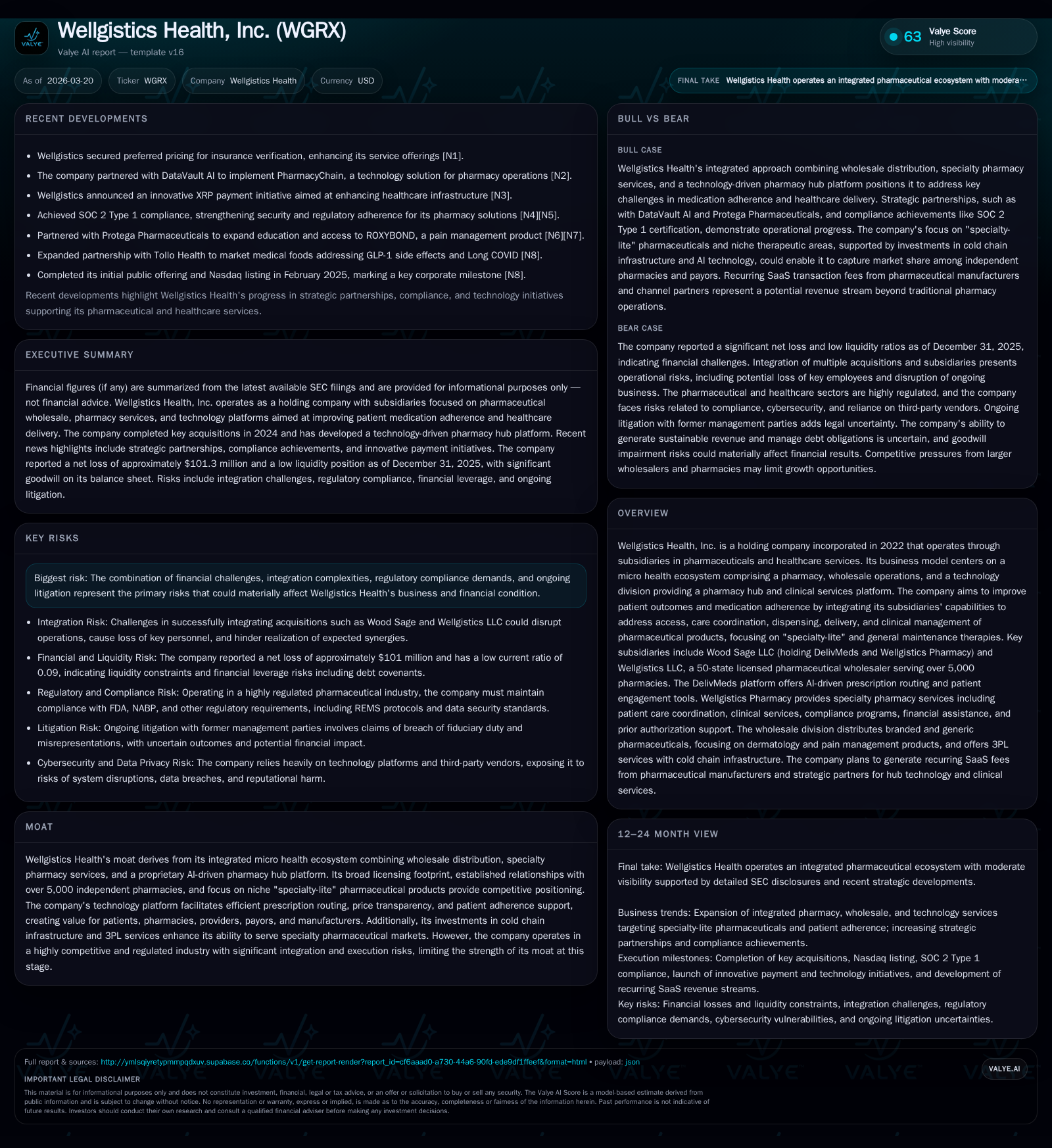

Wellgistics Health, incorporated in 2022, operates an integrated platform centered on pharmaceutical wholesale, specialty pharmacy services, and a proprietary technology hub aimed at improving patient outcomes and medication adherence. Its growth strategy focuses on expanding market access for specialty-lite drugs through a network of independent pharmacies and leveraging AI for prescription management. Despite strategic acquisitions and broad licensing reach, Wellgistics Health has experienced rapidly increasing losses and negative cash flow, compounded by significant litigation risks and industry-wide pricing pressures. Capital constraints and operational integration pose material challenges heading into 2026 as the company seeks to realize synergies among its subsidiaries.

Company Overview and Historical Growth

Wellgistics Health, Inc., established in 2022 as a holding entity, has pursued a distinctive micro health ecosystem model combining pharmaceutical wholesale distribution, specialty pharmacy services focusing on "specialty-lite" therapies, and an innovative technology platform known as DelivMeds. The core strategic vision aims at enhancing patient outcomes through improved medication adherence by integrating access, care coordination, dispensing, delivery logistics, and clinical management across its subsidiaries [S7][S8].

Key subsidiaries include Wood Sage LLC—holding DelivMeds (Wellgistics Tech & Hub) and Wellgistics Pharmacy—alongside Wellgistics LLC, which operates as a 50-state licensed pharmaceutical wholesaler servicing over 5,000 independent pharmacies nationally [S7][S8]. This positioning grants the company considerable reach within independent pharmacy networks that seek competitive pricing and niche products beyond the scope of major retail chains.

Wood Sage was acquired in June 2024 for stock valued at roughly $400,000 at a discount. Prior to acquisition by Wood Sage, DelivMeds provided technology solutions facilitating prescription transfers and backend clinical concierge services since its founding in 2017. Wellgistics Pharmacy dates back to 2011 as a community specialty pharmacy active continuously [S7]. The subsequent acquisition of Wellgistics LLC closed following a membership interest purchase agreement signed in May 2023 amplified the wholesale arm’s scale significantly [S7].

This accelerated consolidation underpins Wellgistics’ bid to leverage cross-segment synergies especially within specialty-lite pharma markets characterized by dermatology-focused topical generics (65% of wholesale portfolio), non-narcotic oral generics (20%), branded therapeutics (10%), and OTC products (5%). Significant investments in cold chain infrastructure underpin future expansion into specialty pharmaceutical categories reliant on temperature-controlled logistics [S8].

Historically, this growth trajectory has not yet translated into profitability. Operating income shifted from a loss of approximately $6.15 million in FY2024 to a substantially larger operating loss nearing $93.7 million in FY2025—a staggering negative swing of over 1400% year-on-year. Correspondingly, net income declined from -$6.86 million in FY2024 to -$101.27 million in FY2025. Operating cash flows deteriorated further into negative territory with -$10.85 million CFO last fiscal year compared to -$1.22 million previously [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -101 | -11 | -94 | -1377.1% |

| 2024 | -7 | -1 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 813.6 |

| 2024 | -101.8 |

Source: SEC companyfacts cache [F1].

The company’s current ratio at year-end 2025 was approximately 0.09 indicating severe liquidity constraints as current liabilities ($29.8 million) exceeded current assets ($2.8 million) by nearly tenfold [F1]. The sharp deterioration reflects ongoing costs related to integration efforts and operational scaling in a capital-intensive environment.

Business Model Nuances and Market Positioning

Wellgistics envisions its ecosystem creating value through three intertwined axes:

- Wholesale Distribution: The backbone operation serving thousands of independent pharmacies with competitive pricing and selective therapeutic portfolios enables the company to gain bargaining leverage with manufacturers.

- Specialty Pharmacy Services: Through Wellgistics Pharmacy LLC providing direct patient-facing dispensing focused on specialty-lite niches designed to enable better adherence for complex or chronic conditions.

- Technology Hub (DelivMeds): Proprietary AI-driven hub offering streamlined prescription routing; prior authorization assistance pre-dispensing; seamless copay processing (full pass-through); telepharmacy offerings for clinical education consultations generating incremental remuneration opportunities; patient financial assistance coordination; and real-time data analytics dashboards for manufacturers [S7][S18][S19][S27].

On the manufacturing side, Wellgistics builds relationships primarily with small-to-mid-size pharmaceutical firms—many boutique or early-stage—with roughly sixty manufacturing partnerships supporting access programs for their limited-distribution drugs with adherence monitoring services critical for successful go-to-market execution [S22][S27]. This contrasts with larger distributors focusing mainly on mass-market generics or top-selling specialty products.

Pharmacy benefit managers (PBMs) remain pivotal payors; however, reductions in third-party reimbursement rates alongside evolving benchmark pricing structures for pharmaceuticals represent pressing margin risks as the company depends heavily on these payer reimbursements [S4][S21]. The Inflation Reduction Act (IRA) passed in 2023 also introduced inflation-linked rebates to Medicare impacting drug pricing dynamics broadly and could impinge profitability going forward.

Risks Around Integration and Litigation

The company’s rapid organic growth through articulated acquisition deals has exposed it to considerable integration risk—aligning staff cultures across Wood Sage’s entities plus Wellgistics LLC while harmonizing IT systems poses execution challenges that could impair expected operational efficiencies or customer continuity [S1][S21]. Loss of key personnel during this transformation is flagged as a material threat.

Additionally concerning is ongoing litigation initiated by Wellgistics Health against certain former officers/directors alleging breach of fiduciary duties linked to shareholder conflicts arising from prior governance disputes. Defendants have sought arbitration complicating resolution timelines; pending hearings may influence contingent liabilities currently accrued around $17.5 million on the balance sheet though no definitive recovery is yet recognized [S11][S16][F1]. The eventual outcome carries financial implications beyond reputational impact.

Financial Structure and Capital Allocation Trends

Wellgistics maintains debt facilities subject to restrictive covenants including liquidity minima that constrain operational flexibility such as dividend payments or share buybacks which currently are not being pursued [S9][S13][S17]. Interest rate sensitivity is elevated given usage of asset-based lending facilities carrying variable rates tied to credit ratings; higher market rates since inception have increased borrowing costs without clear avenues to pass incremental costs downstream effectively due to sector competition [S9][S15].

The large goodwill component resulting from acquisitions constitutes roughly 80% of total assets at fiscal year-end 2025 heightening risk for impairment under adverse economic or business developments which would further depress earnings present and future [S25]. Management remains focused on leveraging its ecosystem synergy potential combined with digital solutions like DelivMeds subscription models targeted at sustainable revenue enhancement from manufacturers seeking real-time patient adherence tracking capabilities.

Future Growth Prospects: Opportunities vs Constraints

Wellgistics aims for continued expansion by deepening its engagement with specialized pharmaceutical manufacturers launching new limited-distribution medicines often requiring targeted patient assistance programs delivered via its integrated hubs. This sector remains attractive due to historically high margins relative to traditional generics but demands significant upfront investment plus regulatory compliance oversight especially regarding cold-chain requirements already underway.

The proprietary AI-driven prescription routing engine presents scalability potential by facilitating omni-channel patient-pharmacy connections with cost transparency features attractive amid payer cost scrutiny. Success hinges on convincing more independent pharmacies into DelivMeds networks enhancing prescription volumes alongside recurring SaaS transaction fees from manufacturer clients benefiting from aggregated clinical data insights.[N1]

However, pervasive reimbursement cuts coupled with rising regulatory burden including fraud/abuse safeguards plus competition from entrenched PBMs retail chains digital native pharmacies like Amazon Pharmacy create margin compression risks alongside market penetration hurdles.[S4][S24]

Continued organizational transformation will test managerial bandwidth impacting initial integration synergies realization timelines. Monitoring several near-term milestones like increases in prescription counts routed through DelivMeds platform combined with measurable improvements in patient adherence metrics will provide tangible proof points toward validating the integrated healthcare model.[N1]

Conclusion

Wellgistics Health embodies an ambitious attempt at forging an interconnected ecosystem spanning wholesale pharma distribution focused on niche categories blended with technology-enabled clinical hubs aiming to improve medication adherence critical for pharmaceutical manufacturers’ commercial success. Nevertheless, the company faces considerable headwinds stemming from severe operating losses escalating sharply over just one year post-major acquisitions compounded by acute liquidity stretches. Integration across multiple recent entities will likely shape near-term performance outcomes amid an evolving regulatory landscape imposing persistent reimbursement uncertainties. Monitoring execution progress against integration milestones along with financial stabilization steps will be essential going forward while assessing litigation resolutions influencing contingent liabilities.

This analysis is based solely on publicly available information as of March 20, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments