Bally’s Corp’s Capital-Intensive Expansion and Indebtedness Challenge Profitability and Cash Flow

Bally’s Corp pursues global gaming growth through integrated resorts, interactive platforms, and acquisitions amidst high leverage and operational risks.

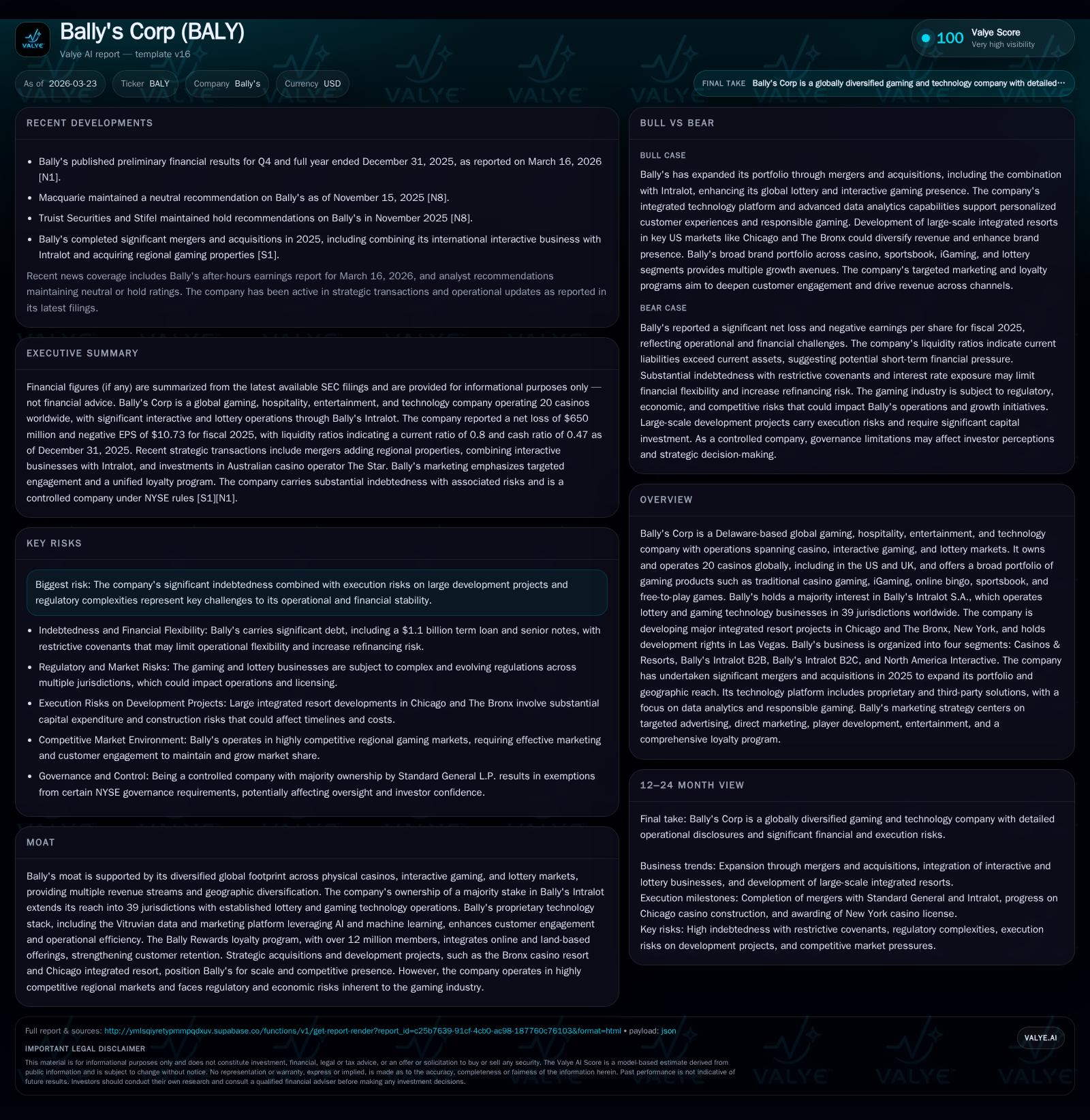

Bally’s Corp operates a diversified portfolio across land-based casinos, North American interactive gaming, and international lottery businesses via Bally’s Intralot. Despite expansive growth efforts including major resort developments in Chicago and The Bronx, the company recorded operating losses worsening to $278 million and net losses expanding to $650 million in 2025. Heavy capital expenditures continue alongside negative free cash flow and significant indebtedness exceeding $4.9 billion, posing constraints on financial flexibility. Strategic execution, regulatory navigation, and successful integration of acquisitions will be key to reversing cash flow pressures and leveraging Bally’s multi-channel ecosystem.

Company Overview

Bally's Corporation (NYSE: BALY), headquartered in Providence, Rhode Island, is a Delaware-based global gaming and entertainment company operating across casino properties, interactive gaming platforms, and lottery services. As of early 2026 it owns or operates 20 casinos worldwide—primarily in the United States across 11 states as well as key locations in the United Kingdom—with additional holdings including a New York golf course and a Colorado horse racetrack [S1][S17].

The company has cultivated multiple revenue streams: traditional gaming at physical properties; iGaming through its Bally Bet Sportsbook & Casino platform licensed across 14 North American jurisdictions; global lottery management via majority ownership of Bally's Intralot S.A., active in 39 international jurisdictions; plus free-to-play games and online bingo offerings. This business diversity mitigates exposure to region-specific downturns or regulatory shifts.

Strategic growth is driven by ongoing major integrated resort developments—most notably in Chicago, Illinois, and The Bronx, New York—alongside retained development rights in Las Vegas at the former Tropicana site. These projects are intended to scale Bally's physical presence into destination-class resorts integrating gaming with hospitality amenities [S1][S17][N1].

Historical Growth and Financial Performance

Bally's revenues are derived primarily from its gaming operations supplemented by ancillary hospitality services. However, despite this diversity, the company's profitability has been under sustained pressure over recent years.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -650 | -11 | -278 | 168 | -14.5% |

| 2024 | -568 | 114 | -258 | 200 | -202.8% |

| 2023 | -187 | 189 | 104 | 311 | +55.9% |

| 2022 | -426 | 271 | -293 | 212 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -179 | -65.4 | |

| 2024 | 0 | -86 | -1837.3 |

| 2023 | 99 | -123 | -29.5 |

| 2022 | 153 | 59 | -52.8 |

Source: SEC companyfacts cache [F1].

Numbers sourced from the latest SEC filings [F1].

Operating income declined further into negative territory reaching approximately negative $278 million for FY2025 compared with a loss of around $258 million a year prior. Net loss widened by over $80 million year-over-year to about $650 million. These results are symptomatic of elevated expenses related to asset investments as well as possible impairments or higher operating costs.

Operating cash flow has turned negative for the first time since FY2022, recording roughly negative $11 million in FY2025 after positive inflows of around $114 million in FY2024. This shift reflects rising working capital consumption or operational cash fragmentation potentially linked to slower integration benefits or cycle timing [F1].

Capital expenditures remain substantial but have slightly moderated to ~$168 million from nearly $200 million last year as Bally's continues its large-scale development projects requiring heavy upfront investment before full commercialization.

Equity grew significantly to nearly $995 million from about $31 million the prior year reflecting balance sheet recapitalization moves or equity injections likely tied to recent M&A transactions [F1]. However, despite this equity build-up, approximate calculated return on equity stood near negative 65%, evidencing that incremental shareholders’ funds have yet to generate sustainable profitability.

Future Growth Prospects

Bally’s future growth hinges on several factors:

- Integrated Resorts: Completion and successful ramp-up of casino-resorts under construction in Chicago and The Bronx will drive visitation traffic expansion beyond existing regional markets. These projects incorporate hotel rooms, entertainment venues, restaurants, and retail components designed to broaden appeal beyond core gamers [S17][N1].

- Interactive Gaming Expansion: The North America Interactive segment represents a strategic growth engine. Bally Bet’s presence across multiple states provides scale benefits as new iGaming regulations materialize nationally. Cross-marketing between land-based casinos and online platforms is expected to boost customer acquisition and retention via unified loyalty rewards [S17][S19].

- Lottery Market Penetration: Through Bally's Intralot S.A., lottery technology sales and management services serve an extensive global network of government clients across Europe, Africa, Asia Pacific, and Latin America. Continued contract wins or renewals underpin steady revenue inflows but face political/regulatory risk variability [S1][S29].

- Acquisitions: Strategic acquisitions made during FY2025 aim to diversify product offerings geographically while leveraging owned intellectual property and proprietary technology systems including AI-driven marketing platforms such as Vitruvian.

However, growth may be capped due to:

- High competition not only from Native American casinos which benefit from tax advantages but also newly legalized operators ramping up aggressive marketing campaigns.

- Regulatory uncertainty around gambling legalization timelines especially for remote iGaming products at state levels could delay market penetration.

- Execution risks inherent in large real estate development projects including construction delays or cost overruns.

- Potential adverse impacts arising from ongoing adjustments for data privacy rules such as GDPR or anti-money laundering enforcement particularly affecting online operations [S1][S9].

Forecasts and Milestones – What To Watch

While explicit forward guidance is not presented publicly [N1][S3], investors should monitor:

- Milestone completions of the Chicago integrated resort construction phases as outlined under GLP Development Agreements which condition funding tranches on achieving specific project deliverables [S23][S28].

- Regulatory license approvals for The Bronx casino redevelopment project expected within current permitting schedules.

- Expansion of Bally Bet licenses into newly legalized states bolstering interactive revenue streams.

- Quarterly earnings relative to operating income improvement trends indicating better cost control or synergies from acquisitions.

- Liquidity metrics tracking adherence to debt covenant ratios given restrictive credit facility terms restricting discretionary spending [S4][S5][S27].

Returns & Capital Allocation Considerations

Bally's reported significant net losses imply very depressed returns on equity—calculated ROE approximates minus-65% for FY2025—with no dividend payout declared reflecting a focus on conserving cash amid heavy reinvestment cycles [F1][S20].

Free cash flow remains negative estimated near -$179 million after accounting for continued capital expenditure outlays exceeding operating cash inflows.

Capital structure is characterized by substantial indebtedness approximating $4.94 billion comprising term loans ($1.47 billion retired early Feb 2026), senior notes due in 2029 and 2031 ($3 billion combined), plus revolving credit facilities providing liquidity buffers [$588 million available] [F1][S4][S5][S27]. Recently issued term loans totaling $1.1 billion carry interest rates ranging roughly from 9–10%, exposing the firm to meaningful financing charges amplified by variable rate exposure linked partly to SOFR benchmarks with floors at 3% plus margins [S16].

Credit facility covenants impose limitations on dividends, share repurchases (none conducted since FY2024), additional borrowings beyond set thresholds, asset sales without lender consent, and capital expenditure caps restricting operational flexibility during refinancing periods [S14][S20]. Consequently:

- Shareholders do not currently receive dividends;

- Buybacks have been halted;

- Cash generation prioritized toward debt servicing;

- Financial strategies must carefully consider covenant compliance whilst supporting ongoing development projects.

Industry Context & Competitive Positioning (Analysis)

In a fiercely competitive industry intersecting physical casinos with burgeoning digital gaming environments, Bally's attempts at integrating these channels via unified loyalty programs surpass many peers who struggle with siloed customer bases. Their Bally Rewards program boasting over twelve million members creates meaningful cross-sell opportunities critical for maximizing lifetime value amid shifting player preferences.

Competition includes low-tax Native American casinos often operating gaming facilities on sovereign lands that evade many state tax policies along with fast-growing iGaming specialists benefiting from agile tech deployment unencumbered by brick-and-mortar constraints.

Seasonality impacts key regional markets requiring careful calendar alignment of events/promotions to drive penetration during peak periods ranging from tourism cycles affecting resort visitation to sports seasonality influencing sportsbook betting volumes.

Operational risks relate predominantly to payment processing dependencies where disruption could severely disrupt transaction flows; credit exposure related to extending lines of credit to customers; evolving consumer data protection laws such as GDPR complicating marketing personalization efforts; compliance burdens around AML/CTF regulations ensuring adherence across multijurisdictional environments; plus construction risk inherent in multi-year capital projects critical for long-term competitive positioning [S11][S22][S24].

Summary & Outlook Considerations

Bally's Corporation occupies a multifaceted role within global gaming combining legacy land-based assets with emerging interactive offerings augmented by international lottery tech operations. Recent financials reflect short-term distress stemming largely from heavy capital investment commitments necessary for ambitious large-scale resorts coupled with lingering challenges integrating acquisitions into cohesive revenue-producing engines.

The company’s future hinges crucially on successfully navigating restrictive debt covenants while executing permitting milestones without significant delay; accelerating online wagering adoption rates supported by robust cross-channel marketing drives; regaining profitability leverage through scale efficiencies; maintaining regulatory compliance amid complex jurisdictional overlays; managing foreign exchange volatility affecting its Intralot exposures; plus sustaining brand vitality via innovative entertainment experiences allied with enhanced data analytics platforms.

Given these dynamics investors should closely track quarterly trends on operating income trajectories vis-à-vis project progress updates alongside liquidity positions highlighting capacity for debt service payments without impairing strategic initiatives.

This memorandum synthesizes publicly available SEC filings dated March 23, 2026 ([S#]) along with company-reported financial figures ([F1]) and relevant news citations ([N#]). It does not provide investment advice but aims solely to inform internal analyses regarding Bally's Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments