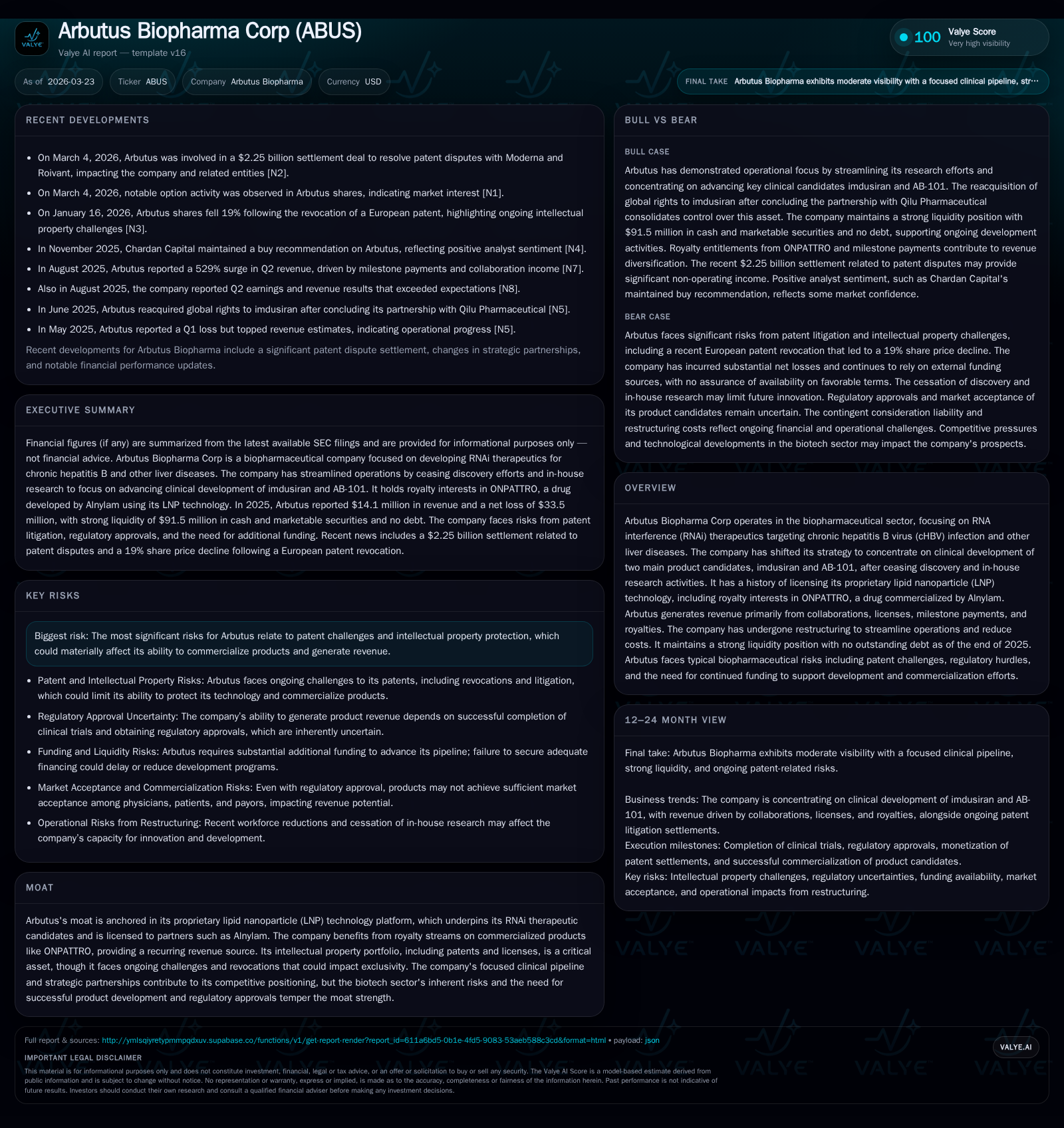

Arbutus Biopharma’s Shift to RNAi Clinical Focus Reframes Financial Trajectory

Streamlining R&D towards two RNAi candidates and monetizing LNP royalties reshape Arbutus’s financial and legal profile in 2025.

Arbutus Biopharma has transitioned from broad discovery operations to concentrated clinical advancement of imdusiran and AB-101, reflecting a strategic pivot evident in substantial R&D cost reductions and focused pipeline investment. Despite operating losses, revenue more than doubled year-over-year driven by growing royalty streams tied to its proprietary lipid nanoparticle platform, particularly via ONPATTRO. Ongoing patent litigations with major biotech players Moderna and Pfizer/BioNTech remain critical, with a recent $2.25 billion settlement with Moderna impacting contingent payments and cash flow visibility. The company maintains a robust liquidity position with no debt, but faces typical biopharma risks linked to patent challenges, regulatory compliance and reimbursement uncertainties.

Strategic Refocus: Transitioning To Imdusiran and AB-101 Clinical Development

In 2025, Arbutus Biopharma executed a marked strategic shift away from its prior broad R&D model toward a streamlined clinical-stage focus anchored on two RNA interference (RNAi) therapeutic candidates: imdusiran and AB-101 [S1][S13]. This pivot entailed ceasing all discovery efforts and halting preparations for an IM-PROVE III trial as part of the imdusiran program. Workforce reductions were implemented to align with this narrower scope, allowing a concentration of resources on advancing these lead programs in chronic hepatitis B virus (cHBV) infection and other liver diseases [S1].

The impact is apparent in expense profiles where research and development (R&D) costs dropped by approximately $28.8 million compared to 2024, reflecting both the elimination of early-stage research and leaner personnel expenses [S1]. Such cost containment underscores an operating leverage effect; however, it also increases pipeline concentration risk given future growth depends heavily on the success of these two molecules.

Revenue Upswing Despite Operating Losses: Examining 2025's Turnaround Metrics

Financially, Arbutus posted revenues of $14.08 million in FY2025 representing a significant rebound of +128% compared to the $6.17 million recorded in FY2024 [F1]. This revenue surge was driven primarily by collaborations, license agreements, milestone payments, and royalty income related to its proprietary lipid nanoparticle (LNP) technology [S1]. Despite this growth in top-line figures, the company reported an operating loss of $38.16 million in 2025—a narrower deficit relative to the $76.32 million operating loss posted in FY2024—indicating ongoing investment in clinical development phases but with improved operational efficiency [F1].

Net income losses followed a similar pattern: -$33.5 million versus -$69.9 million previously [F1]. Operating cash flow remains negative at -$39.6 million but represents a material improvement over prior years’ cash burn rates, signaling enhanced sustainability alongside reduced capex spending which was effectively nil in 2025 versus minimal prior levels [F1][S13]. These metrics reflect the company’s transition phase where revenue generation begins balancing against heavy experimental costs—a common profile for clinical-stage biotech firms riding emergent assets.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 14 | -34 | -40 | -38 | +128.2% | +52.1% |

| 2024 | 6 | -70 | -65 | -76 | -66.0% | +4.0% |

| 2023 | 18 | -73 | -86 | -78 | -53.5% | -4.9% |

| 2022 | 39 | -69 | -35 | -65 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -40 | -43.7 |

| 2024 | -65 | -71.8 |

| 2023 | -87 | -68.7 |

| 2022 | -36 | -50.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue surged proportionally after restructuring; losses narrowed but remain significant amid ongoing R&D investments.

LNP Platform Monetization: Royalty Streams and Licensing as Revenue Pillars

Arbutus’s moat centers on its proprietary lipid nanoparticle (LNP) technology platform critical for delivering RNAi therapeutics. This patented LNP technology underpins its clinical candidates but also serves as a vital income source through licensing agreements—most notably royalties linked to ONPATTRO from Alnylam Pharmaceuticals [N1][S12]. These royalty streams provide recurring revenue less correlated with Arbutus’s direct internal R&D expenditures.

The company strategically monetized portions of these royalties; a notable transaction includes selling part of the ONPATTRO royalty interest to OMERS for upfront proceeds while retaining future royalty upside beyond a threshold amount [S12]. This approach strengthens cash reserves while maintaining long-term option value from partner drug sales.

From an intellectual property standpoint within biotech sector dynamics:

- Licensing income is recognized based on subsequent partner sales rather than upfront fees alone,

- Royalty payments typically involve low single-digit percentages generating stable revenue support for otherwise capital-intensive innovation cycles,

- Protecting exclusivity around such platform patents remains central given competitive threats from large pharmaceutical players seeking LNP applications.

Patent Litigation Fronts and Settlement Implications: Moderna and Pfizer/BioNTech

Arbutus remains actively engaged in asserting patent rights against major industry players Moderna and Pfizer/BioNTech concerning alleged infringement related to mRNA vaccine delivery using LNP technologies foundationally developed by Arbutus/Genevant affiliates [N1][S1][S4]. The litigation strategies encompass multiple cases including claims in District Courts as well as appeals invoking defenses such as §1498—a complex statutory defense relevant when government contract use is involved.

A landmark development occurred March 3, 2026 through the Moderna Settlement Agreement valued at $2.25 billion comprising both noncontingent ($950 million) and potential contingent ($1.3 billion) settlement payments reliant on appellate outcomes favoring Arbutus’s position [N1][S1]. These contingent payments hinge on final judicial determinations about claim validity and interpretation (“claim construction”) with potential clawbacks if rulings later negate Arbutus’s victory.

Such legal outcomes materially affect:

- Near-term liquidity through received settlement payments,

- Longer-term risk profiles due to contingent payment reversals,

- Share price volatility tied to pending court decisions,

- The company's capacity to reinvest or return capital based on litigation result timelines.

Parallel litigation continues against Pfizer/BioNTech with partial favorable rulings on claim constructions announced late 2025 though full resolutions remain pending [S1][S4]. Litigation cost impact has declined somewhat with lower legal fees contributing to general administrative expense reductions.

Cost Discipline in a Biotech Context: Impact of Workforce Reductions and R&D Cuts

The company’s restructuring yielded tangible expense declines despite increased restructuring-related charges [$12.9 million vs $3.7 million prior year] reflecting severance and facility consolidation costs [F1][S1]. Operating expenses fell roughly $30 million overall driven chiefly by slashed R&D outlays ($25.2 million in 2025 vs $54 million prior), aligning with strategic de-emphasis on discovery programs [F1][S13].

General administrative expenses dropped nearly $6.2 million due mostly to lower employee compensation accruals and litigation-related legal fees easing post-settlement agreements [S1]. Continued operating leverage emerges from reduced burn rates supporting longer runway amid modest revenue gains.

Trade-offs include elevated pipeline risk due to fewer diversified projects weighted towards imdusiran/AB-101 success—common tension balancing cost reduction against innovation breadth in biotech corporates.

Liquidity Strength and Capital Allocation: Managing Cash Without Debt

As of December 31, 2025 Arbutus held $18 million in cash plus $73.5 million invested in marketable securities totaling approximately $91.5 million liquid resources with zero outstanding debt creating an enviable balance sheet structure among clinical-stage peers [F1][S12]. The resulting current ratio stood at 15.7x underscoring substantial short-term solvency cushion.

The company has not executed any share buybacks during this period nor declared dividends consistent with its developmental stage but runs an Employee Stock Purchase Plan contributing minor stock-based compensation expense without dilutive share issuance spikes [S25]. Capital allocation focuses chiefly on funding clinical trials while preserving cash reserves amidst volatile legal payment timing uncertainty.

Negative free cash flow around -$39.6M illustrates ongoing investment requirements even with reduced capex spending demonstrating reliance on external capital markets or monetization events moving forward for sustainability [F1][S12].

Regulatory, Legal, and IP Risks: Navigating the Challenging Biopharma Terrain

Arbutus operates under complex regulatory regimes including FDA compliance for clinical development stages alongside extensive IP risks highlighted by ongoing patent disputes detailed earlier . Additional liabilities arise from healthcare laws such as Anti-Kickback statutes and False Claims acts that impact collaborations or marketing efforts requiring vigilant compliance frameworks.

Pricing regulations enacted recently—like those embedded within the Inflation Reduction Act impacting Medicare Part B/D inflation rebates—introduce variable risks around reimbursement tied to pricing acceleration controls starting in 2026 potentially affecting commercial viability if relevant products reach market . Participation obligations under Medicaid Drug Rebate Program impose further rebate liabilities where defective pricing reports can trigger penalties or loss of federal fund eligibility.

Product liability remains a nontrivial concern anticipated to increase upon commercialization attempts requiring adequate insurance coverage; current clinical trial insurance capped at $10 million per occurrence provides limited protection should adverse events occur post-launch [S18].

Growth Catalysts and Risks Ahead: Milestones to Monitor in Clinical and Legal Arenas

Looking forward key inflection points will revolve around:

- Reporting progress from imdusiran’s clinical trials including any resumed or advanced studies beyond halted IM-PROVE III preparation,

- Data readouts from AB-101’s Phase 1a/1b trials offering safety/efficacy insights feeding regulatory discussions,

- Judicial rulings upcoming within roughly one year concerning patent disputes especially related to §1498 appeals influencing contingent payment reception,

- Potential new licensing deals or royalty monetizations leveraging remaining LNP portfolio extensions,

- Regulatory submissions or approvals tied to their RNAi therapeutics impacting commercial readiness,

- Market reimbursement landscape adjustments given federal drug pricing policy shifts extracting negotiation leverage away from novel drugs.

Any adverse developments on these fronts could impair growth prospects whereas successful trial outcomes coupled with favorable litigation results would materially strengthen valuation narratives despite persistent sector risks intrinsic to innovative biotechnology firms.

This analysis is based exclusively on publicly available data as of March 23rd, 2026 without forecasting unreported financial metrics or making investment recommendations. Past financial performance is not indicative of future results; readers should consider inherent biotech sector volatilities related to regulatory approvals and patent litigations when assessing Arbutus Biopharma's outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments