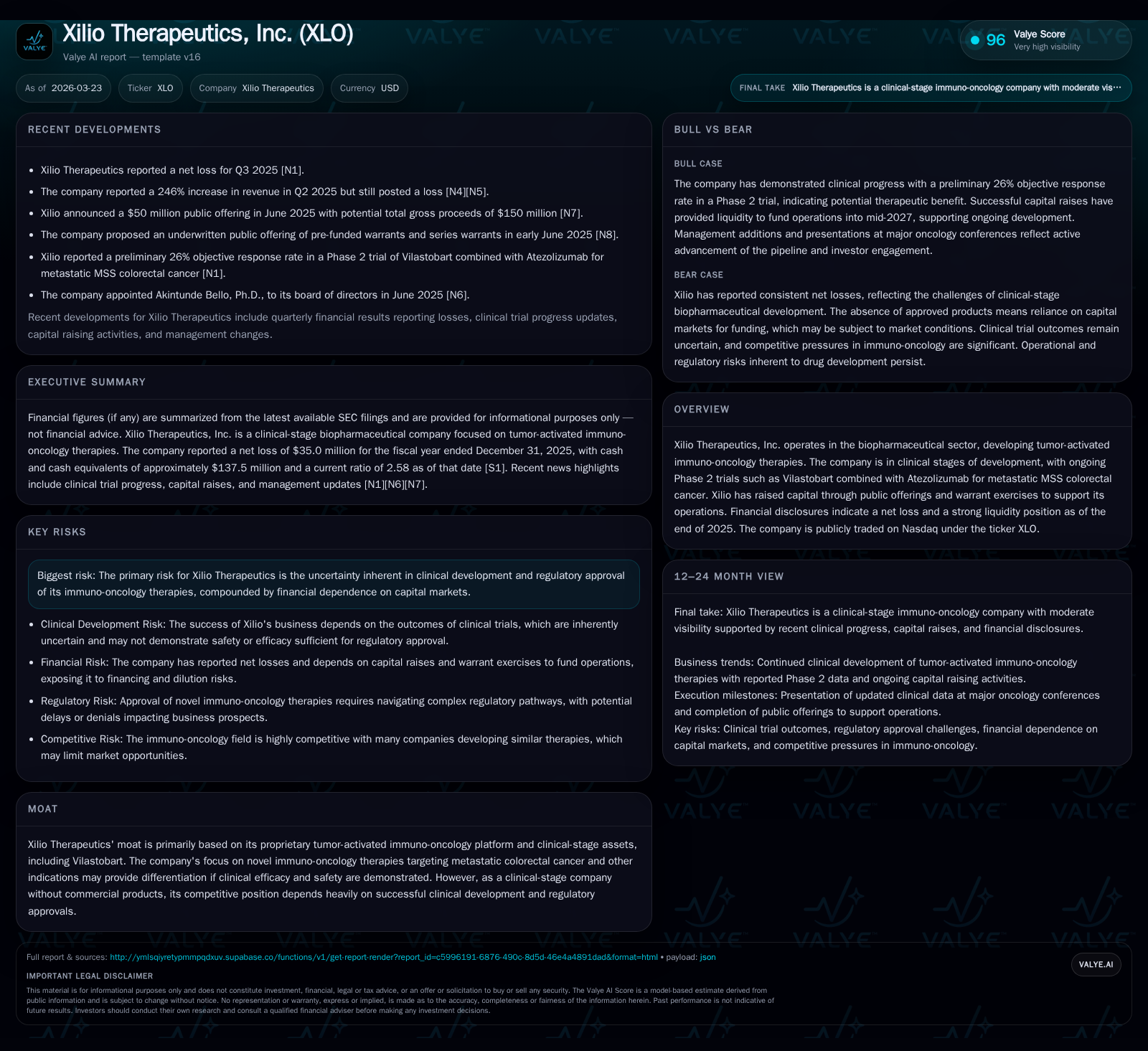

Xilio Therapeutics Advances Tumor-Activated Immuno-Oncology Amid Capital and Clinical Development Challenges

Xilio Therapeutics focuses on innovative cancer therapies with ongoing trials and maintains strong liquidity to support its clinical pipeline.

Xilio Therapeutics, a clinical-stage biopharmaceutical firm, is developing tumor-activated immunotherapies primarily targeting metastatic colorectal cancer. Over recent years, the company has progressively reduced operating losses while continuing negative cash flows, supported by capital raises including warrant exercises and pre-funded warrant offerings. Its future growth hinges on pivotal Phase 2 trials such as Vilastobart plus Atezolizumab, regulatory approvals, and sustained capital access. The firm's liquidity position was robust at the end of 2025, with over $137 million in cash and equivalents and a current ratio exceeding 2.5, ensuring runway into mid-2027.

Company Overview

Xilio Therapeutics, Inc. is a clinical-stage biopharmaceutical company specializing in tumor-activated immuno-oncology therapies aiming to enhance the immune system's ability to target solid tumors while minimizing off-target effects. Its lead clinical asset, Vilastobart, is under evaluation in Phase 2 studies combined with the checkpoint inhibitor Atezolizumab for metastatic microsatellite stable (MSS) colorectal cancer — an area with significant unmet medical needs due to limited efficacious treatments.

Historical Financial Performance

Over the past four fiscal years (2022–2025), Xilio has experienced consistent operating losses as it invests heavily in research and development without any product revenues to offset expenses. However, these losses have steadily narrowed from an operating loss of approximately $89.1 million in FY2022 to around $42 million in FY2025, illustrating some operational improvements possibly from cost controls or more efficient R&D spend [F1]. Net losses followed a similar trajectory — shrinking from $88.2 million in FY2022 to $35 million in FY2025.

Despite persistent net outflows from operations, cash flow shortfalls have also moderated considerably, with operating cash flow deficits narrowing sharply from approximately -$75.7 million in FY2022 to -$5 million in FY2025 [F1]. This pattern aligns with typical biopharma development-stage companies progressing closer toward clinical validation milestones that can support operational scaling or strategic partnerships.

Capital expenditures have remained minimal relative to operating costs but showed a notable increase last year ($518 thousand in FY2025 vs $36 thousand prior year), potentially reflecting investments related to infrastructure or technology upgrades.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -35 | -5 | -42 | 518000 | +39.8% |

| 2024 | -58 | -18 | -61 | 36000 | +23.8% |

| 2023 | -76 | -69 | -79 | 486000 | +13.4% |

| 2022 | -88 | -76 | -89 | 1867000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -99.3 |

| 2024 | -18 | -331.0 |

| 2023 | -69 | -207.5 |

| 2022 | -78 | -83.5 |

Source: SEC companyfacts cache [F1].

Table: Select annual financial metrics for Xilio Therapeutics (USD)

Capital Structure and Liquidity

As of December 31st, 2025, Xilio reported cash and cash equivalents totaling approximately $137.5 million and current assets of around $145 million against current liabilities near $56 million — yielding a strong current ratio of about 2.58 [F1]. This liquidity buffer supports operations comfortably into the foreseeable future.

This ample liquidity is supported by recent capital raises including the exercise of Series B warrants generating gross proceeds of about $35.8 million through end-2025 [S11], alongside a February 2026 underwritten offering of pre-funded warrants expected to deliver net proceeds near $37.1 million [S23]. These fundraises underscore management’s strategy focused on maintaining financial flexibility to advance clinical programs without commercial revenue streams.

Additionally, a reverse stock split (1-for-14) completed in March 2026 enhanced compliance with Nasdaq listing requirements following a period of price weakness but did not alter the number of authorized shares or par value [S7][S8].

Growth Prospects and Clinical Pipeline

Xilio's future growth potential largely hinges on successful clinical development of its tumor-activated immunotherapy platform which is designed to selectively activate therapeutics within the tumor microenvironment rather than throughout systemic circulation — mitigating immune-related adverse events common with current IO drugs.

Key near-term milestones include data readouts from ongoing Phase 2 trials such as Vilastobart + Atezolizumab for metastatic MSS colorectal cancer [N/A]. Regulatory approval prospects remain uncertain but are critical for commercialization given no approved products yet exist.

Xilio’s moat stems principally from its proprietary technology enabling site-specific activation that could differentiate efficacy and safety profiles if validated clinically. However, this also imposes significant risk because failure at any stage could substantially impair valuation and strategic options.

Capital Allocation and Returns

With no product revenues or dividend policy evident given Stage III development status [F1], Xilio's focus remains on deploying cash resources toward R&D activities essential for advancing pipeline candidates through clinical inflection points.

Equity levels have contracted significantly over four years — down from approximately $105.6 million at end-2022 to about $35.3 million by end-2025— reflecting cumulative losses that outpaced equity injections despite recent financing [F1]. This results in an approximate return on equity (ROE) of roughly -99% as per last annual data, illustrating the typical loss profile for early clinical biotech.

Free cash flow calculated as CFO minus capex is negative (about -$5.5 million in FY2025), but improving markedly compared to prior years [F1]. No share repurchases or dividends were reported during this period consistent with standard industry practice for clinical-stage firms reliant on external financing.

Industry Context Analysis (Non-company Specific)

Immuno-oncology continues as a highly competitive yet rapidly evolving sector dominated by checkpoint inhibitors like PD-1/PD-L1 antibodies with expanding combinations across tumor types including colorectal cancer. Tumor-specific activation platforms represent innovative approaches seeking better therapeutic indices by reducing systemic toxicities—a key barrier constraining broader adoption due to immune-related adverse events with existing agents.

Demonstrating robust efficacy coupled with manageable safety profiles will be essential for competing against established IO giants and emerging cell therapy modalities. Engagements with large pharma partnerships or licensing deals typically underpin mid-stage biotechs' sustainability outside direct commercialization.

Risks Overview

As highlighted by the company’s SEC disclosures [S4][S5], principal risks include inherent uncertainties tied to drug development timelines and outcomes plus regulatory approvals that are unpredictable by nature within oncology drug discovery programs.

Financially dependent on periodic access to capital markets for operational funding amid demonstration-dependent valuation volatility exposes Xilio to dilution risks or unfavorable financing conditions should trial setbacks occur or market sentiment shift negatively.

What To Watch Next (Analysis)

Key markers include:

- Clinical data releases from Phase 2 studies evaluating safety/efficacy signals of Vilastobart combinations.

- Updates on regulatory interactions which might provide guidance on possible accelerated pathways or approval timelines.

- Subsequent capital market moves reflecting investor sentiment toward upcoming catalysts or shifts in funding environment.

- Execution against planned milestones enabling transition toward late-stage development or partnering opportunities.

Summary

Xilio Therapeutics presents as a classic clinical-stage biotech venture operating within an innovative corner of immuno-oncology aimed at improving therapeutic windows through tumor-directed drug activation technology—an approach potentially capable of meaningful differentiation if validated clinically.

Financially resilient through active capital management strategies including reverse splits and warrant offerings providing sufficient liquidity into mid-2027 ensures runway continuity amid persistent operating losses typical of developmental biotechs without product revenues.

The company’s trajectory will be closely tied to upcoming clinical progress reports validating its scientific premise and practical benefits — both prerequisites before any material revenue generation can commence. Meanwhile Xilio remains exposed to developmental risks balanced against significant opportunity inherent within this challenging but high-potential oncology niche.

This analysis does not constitute investment advice or recommendations regarding Xilio Therapeutics’ securities. It is intended solely for informational purposes based on publicly available data as of March 23rd, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments