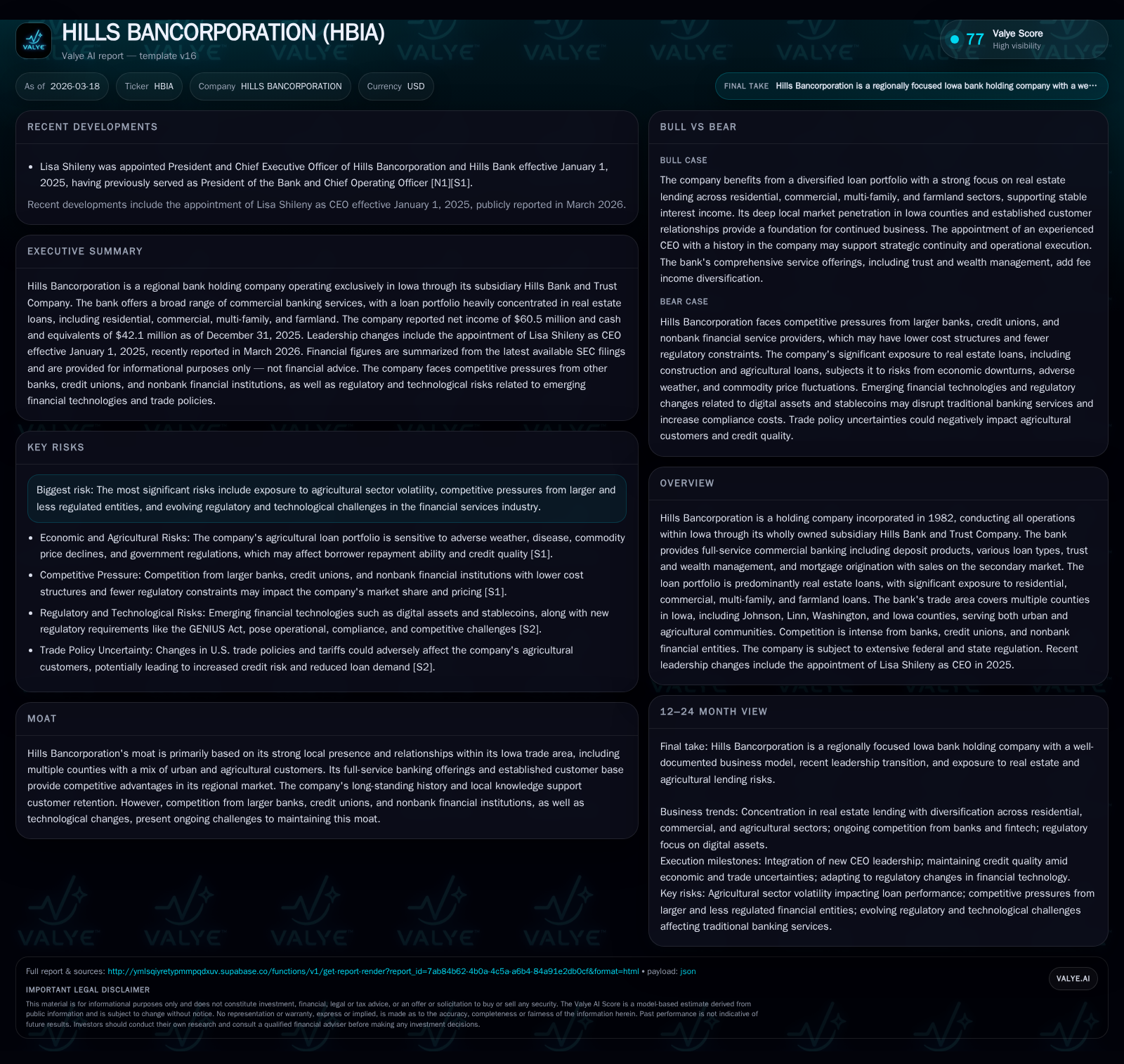

Hills Bancorporation Strengthens Loan Growth and Profitability While Managing Regional Banking Risks

Hills Bancorporation reported solid financial performance in 2025 supported by expanding loan portfolios, increased net interest margins, and disciplined capital management within the Iowa regional market.

In 2025, Hills Bancorporation, through its wholly owned Hills Bank and Trust Company, exhibited strong earnings growth with net income rising 27.1% to $60.5 million. The key driver was a $119 million increase in loan balances, particularly in residential and commercial real estate loans, alongside improved net interest margin from higher rates and asset growth. Despite competitive pressures and macroeconomic headwinds including inflation and evolving regulatory demands, Hills maintained well-capitalized status with a community bank leverage ratio of nearly 13%. New CEO Lisa Shileny steps into leadership amid ongoing shifts in banking technology and deposit behaviors. Watching credit quality trends and deposit stability will be critical for future growth given the bank’s nearly 22% uninsured deposit exposure.

Company Overview and Historical Performance

Hills Bancorporation was incorporated in 1982 as a holding company for Hills Bank and Trust Company, conducting all operations within Iowa through its subsidiary bank. The bank serves individuals, businesses, governmental units, and institutional customers across multiple counties including urban centers like Iowa City as well as agricultural communities.

The business model centers on full-service commercial banking offerings such as demand, savings, time deposits; commercial, real estate (residential and commercial), agricultural loans; trust administration; wealth management services; and mortgage origination with secondary market sales without servicing retention.

No acquisitions have occurred since early 2000s consolidation efforts within Iowa [S1]. The bank’s strong local presence supports its competitive positioning.

Financial Performance Trends (FY2022–FY2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 61 | 69 | 4 | +27.1% |

| 2024 | 48 | 56 | 5 | +24.7% |

| 2023 | 38 | 53 | 3 | -20.1% |

| 2022 | 48 | 56 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 10 | 16 | 65 |

| 2024 | 10 | 13 | 51 |

| 2023 | 10 | 8 | 50 |

| 2022 | 9 | 8 | 55 |

Source: SEC companyfacts cache [F1].

Note: Figures represent fiscal year-end data; operating cash flow (CFO), capex, dividends, buybacks reflect annual cash movements; equity is period-end stockholders’ equity.

Over this period:

- Net income rebounded strongly after a dip in 2023.

- Operating cash flow grew significantly while capital expenditures moderated.

- Equity base expanded steadily supporting lending capacity.

- Dividends steadily increased alongside more aggressive share repurchases reflecting shareholder return focus.

Business Composition and Growth Drivers

As of December 31, 2025, the loan portfolio held for investment totaled approximately $3.57 billion representing a year-over-year increase of about $119 million [S4][F1]. Real estate loans constitute roughly eighty-six percent of the loan book covering residential (first liens dominant), commercial real estate including multifamily units, construction loans, farmland mortgages, and agricultural loans.

Key portfolio movements include:

- Residential real estate loans increased by approximately $88 million driven mainly by one-to-four family first mortgages (~40% of loan portfolio).

- Commercial mortgages rose by about $67 million reflecting completion of construction projects transitioning into permanent financing.

- Smaller increases occurred in junior mortgages (+$2 million) and farmland (+$1 million).

- Construction loans decreased modestly (-6%), possibly indicating slower new project starts or paydowns.

Loan originations accelerated markedly to around $130 million net new loans compared to minimal origination prior year indicating renewed lending activity focused on core markets without significant external participations beyond small community development activities [S4].

Deposits grew slightly by approximately $21.7 million reaching about $3.37 billion primarily due to increases in noninterest-bearing deposits (+$15 million) and savings accounts despite declines in time deposits (-$97 million) [S10][F1].

Interest rate dynamics favored wider spreads as the Federal Reserve moderately reduced target funds rate during the year but overall maintained elevated real rates relative to prior cycles; net interest margin expanded from about 2.78% to approximately 3.45% for full-year 2025 contributing substantially to net interest income growth [S21].

Forward Growth Outlook and Constraints

Hills Bancorporation's future performance depends on several factors:

- Regional Economy: Agricultural commodity prices and farm incomes remain vital given Iowa’s economic profile; trade policy uncertainties could affect credit demand or asset quality [S2].

- Interest Rates: Rate levels influence mortgage refinancing volumes and commercial borrowing costs; prolonged high rates may constrain demand or elevate credit risk.

- Competition: Larger banks with scale advantages plus fintech entrants offering digital alternatives challenge customer acquisition/retention requiring innovation alongside relationship strength.

- Credit Quality: Management maintains conservative allowance for credit losses with ongoing review of nonaccruals amid inflationary pressures [S16][S20].

- Regulation: Capital adequacy remains strong with Community Bank Leverage Ratio near 13%, comfortably exceeding minimum regulatory requirements impacting capital deployment flexibility [S5][S13].

- Technology: Increasing digital delivery channel adoption is critical; delays or failures here risk losing ground to more tech-savvy competitors [N1][S24].

Formal guidance is not publicly disclosed but milestones include continued loan book growth especially residential real estate which historically drives margins; maintenance of low delinquency; efficiency ratio control amidst digital investments; strategic capital return consistency signaling confidence.

Capital Allocation & Shareholder Returns

The company demonstrates prudent capital stewardship balancing growth investments against shareholder returns:

- Return on average equity approximates about 11% for fiscal year 2025 based on net income relative to average equity levels indicating sound profitability for a regional lender [F1].

- Operating cash flow generation (

$68.8 million) comfortably exceeds capital expenditures ($3.7 million), sustaining robust free cash flow availability for distributions or reinvestment [F1]. - Dividends paid totaled just over $10 million consistent with steady payout policies.

- Share repurchases approximated $15.6 million highlighting active efforts to enhance per-share metrics amid earnings growth [F1].

Liquidity is primarily funded by customer deposits supplemented by Federal Home Loan Bank advances which declined notably from prior periods suggesting greater reliance on internal funding sources [S12][S17]. Elevated uninsured deposit share—around one-fifth—could present episodic withdrawal risks under stress scenarios warranting monitoring [S6].

Sector Context Analysis

Community banks like Hills Bancorporation operate regionally balancing personalized service against scale economies favoring larger institutions or digital-first national models. Local relationships are emphasized especially given agriculture sector cyclicality affecting credit cycles.

Post-financial crisis reforms including Basel III integrate risk sensitivity into capital requirements which Hills meets comfortably. Fintech innovations disrupt traditional revenue streams raising urgency for adaptation.

Leadership Transition & Strategic Signals

The appointment of Lisa Shileny as CEO announced early 2026 marks a governance milestone signaling planned succession combined with strategic continuity amid technological change challenges [N1]. Her leadership will be pivotal navigating digital transformation initiatives aligning with evolving customer demands while managing inflation-induced borrower stress risks.[N1][S1]

There are no material legal proceedings currently affecting the company reinforcing operational stability.[S23]

Conclusion & Monitoring Points

Hills Bancorporation presents stable earnings growth fueled by diversified real estate loan expansion alongside disciplined capital allocation delivering meaningful shareholder value via dividends and buybacks. Liquidity management balances notable uninsured deposit exposure against strong secured funding access through FHLB advances. Risks stem from macroeconomic pressures—persistent inflation affecting borrower creditworthiness—and intensified competition from less regulated fintech players challenging traditional banking moats anchored on locality.[S24] Leadership change presents opportunity for refreshed strategic vision critical as financial services face accelerating innovation.[N1] Investors should monitor quarterly credit quality disclosures particularly special mention categories alongside deposit mix changes as early indicators shaping ongoing financial performance.

Disclaimer: This report provides an analytical perspective on Hills Bancorporation’s historical performance, industry context, operational risks, and capital dynamics without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments