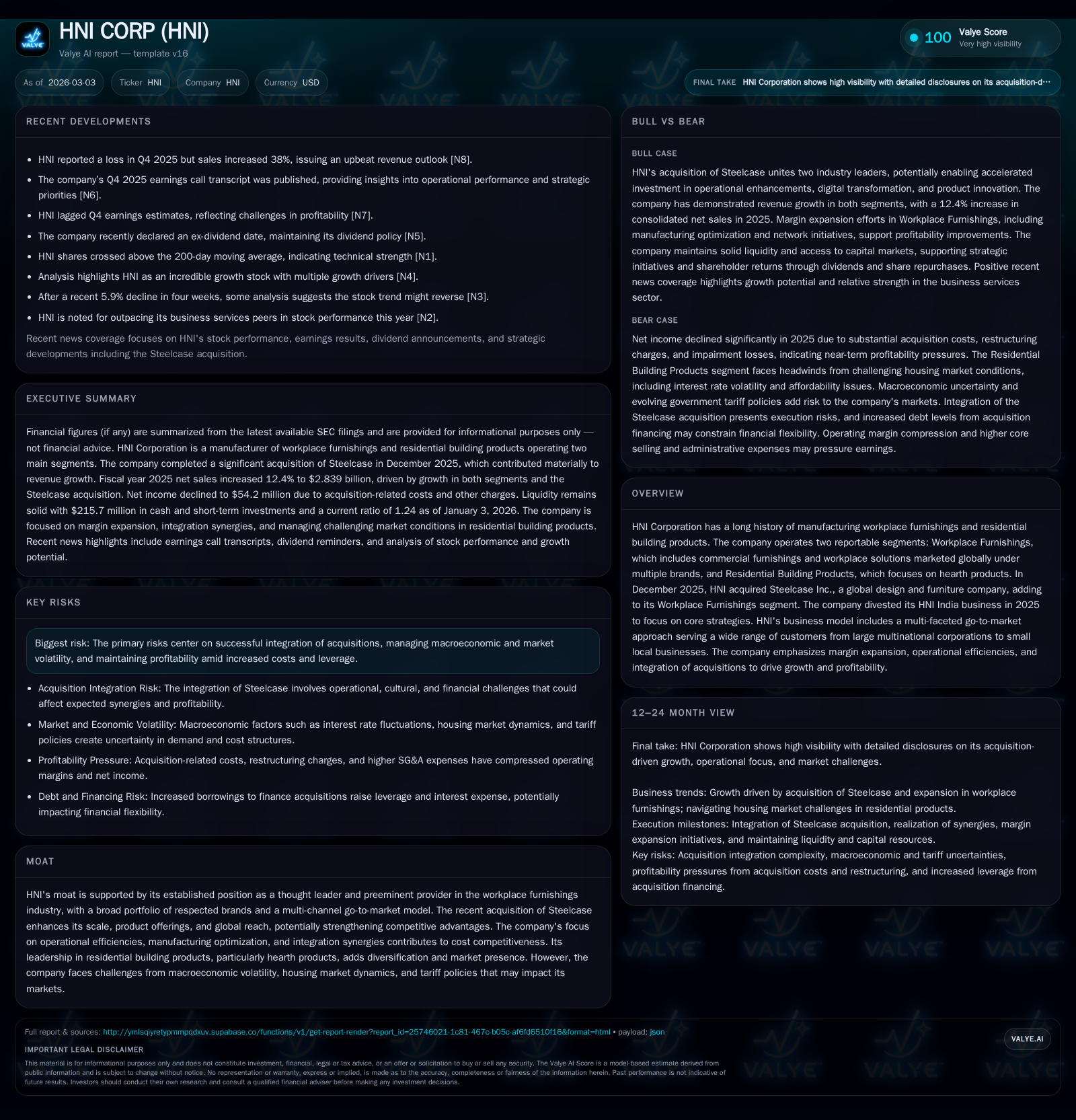

HNI Faces Integration Challenges and Leverage Pressure Following Steelcase Acquisition

The 2025 acquisition of Steelcase reshapes HNI’s workplace furnishings scale but weighs on near-term profitability and leverage.

HNI Corporation expanded significantly with the $1.9 billion acquisition of Steelcase in late 2025, enhancing product breadth and global reach. While revenue growth was driven by acquisitions, operating income declined 39% year-over-year due to acquisition-related costs and restructuring charges. Net income fell over 60%, pressured by higher interest expense from increased borrowings. The company’s total debt rose to approximately $1.3 billion post-acquisition, creating covenant constraints. Capital expenditures increased to nearly $68 million, supporting manufacturing and digital investments. Share repurchases accelerated to $83.6 million, while dividends remained steady at around $63 million in 2025. The outlook depends on successful integration, synergy realization, margin recovery, and macroeconomic stability.

Company Overview and Segment Structure

HNI Corporation has a history spanning more than eight decades as a manufacturer of workplace furnishings through its Workplace Furnishings segment and operates the nation’s largest hearth products business within Residential Building Products [S1]. In December 2025, HNI completed the acquisition of Steelcase Inc., a global design and furniture company, in a cash and stock transaction valued at approximately $1.9 billion [S1]. This transaction significantly expanded HNI’s scale and capabilities in the commercial furnishings market.

The company serves customers mainly via independent dealers, distributors, direct sales channels, including government entities [S1]. Its diversified portfolio includes furniture systems, seating, storage, tables, architectural products, ancillary hospitality products for workplaces, as well as hearth products for residential customers.

Historical Performance (FY2023-2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 54 | 276 | 126 | -61.1% |

| 2024 | 140 | 227 | 207 | +183.5% |

| 2023 | 49 | 268 | 90 | -60.3% |

| 2022 | 124 | 81 | 155 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 63 | 84 | 3.0 |

| 2024 | 64 | 66 | 16.6 |

| 2023 | 59 | 0 | 6.5 |

| 2022 | 53 | 65 | 20.1 |

Source: SEC companyfacts cache [F1].

Note: Consolidated revenues are not explicitly stated for FY25 but segment disclosures indicate growth largely driven by acquisitions [S16], [S27].

In fiscal year 2025, operating income declined by approximately 39% compared with the prior year due primarily to significant acquisition-related costs totaling $94.6 million related to Steelcase integration plus restructuring and impairment charges of $18.5 million attributable mainly to smaller Workplace Furnishings businesses and manufacturing optimizations [S17], [S18]. Net income decreased by over 60%, impacted also by increased interest expense rising to $35.6 million from $27.2 million in the prior year following higher borrowings used to finance the acquisition [F1], [S18].

Despite earnings pressure, operating cash flow increased by nearly 22% year-over-year to $276 million due to strong underlying cash generation and working capital management [F1]. Capital expenditures rose almost 28% year-over-year to $67.8 million as investments supported manufacturing enhancements—particularly at the Mexico facility—and digital transformation initiatives [F1], [S19].

Revenue Growth Drivers and Segment Analysis

Revenue growth was primarily acquisition-driven with the consolidation of Steelcase beginning late Q4 FY25 adding scale within Workplace Furnishings alongside ongoing integration synergies from Kimball International acquired in mid-2023 [S1], [S26]. Segment data suggest Workplace Furnishings revenues grew from about $1.74 billion in FY23 to roughly $2.16 billion in FY25 [S27]. Residential Building Products revenue remained relatively stable near the $650–675 million range but faced modest declines due to housing market softness [S27].

Operationally, the Workplace Furnishings segment focused on margin expansion through network rationalization, production relocation to lower-cost geographies like Mexico, pricing adjustments amid inflationary pressures, and divestiture of non-core businesses such as HNI India completed mid-2025 [S1], [S26].

Debt Profile and Leverage Considerations

Following the Steelcase acquisition closing on December 10, 2025, HNI’s total debt rose substantially to about $1.3 billion as of January 3, 2026—up from roughly $345 million at the prior fiscal year-end—consisting of revolving credit facilities ($15 million drawn), Term Loan A ($350 million), Term Loan B ($500 million), and public notes ($450 million) issued or restructured around the transaction close [S14], [S15], [F1]. Interest rates on floating rate debt approximate mid-5% levels reflecting base rates plus margins tied to net leverage.

Financial covenants under these credit agreements require maintenance of maximum net leverage ratios starting at approximately 4.25x immediately post-acquisition declining progressively toward about 3.50x within two years post-close. Additionally, a minimum interest coverage ratio of at least 3.50x is mandated quarterly [S9], [S13].

Liquidity is supported by a revolving credit facility with total borrowing capacity up to approximately $425 million available beyond amounts drawn plus restricted cash balances totaling around $8.8 million at fiscal year-end [S10], [F1].

Capital Allocation Strategy

Despite elevated leverage levels following acquisition financing activities, capital returns remained active: dividends paid were steady at approximately $63 million annually over recent years reflecting consistent shareholder yield policy amid transitional earnings volatility [F1], [S24]. Share repurchases accelerated significantly in fiscal year 2025 reaching about $83.6 million compared with lower levels previously as management pursued opportunistic buybacks supported by stable cash flow generation despite stock price fluctuations reported in market commentary [F1], [N10]. Approximately $84 million remained authorized for future repurchases at year-end.

Additionally, tactical liquidity management included borrowing against Company Owned Life Insurance (COLI) policies totaling $32 million drawn during Q4 FY25 providing supplemental financial flexibility within broader capital structure oversight frameworks [S17].

Outlook and Risks

HNI anticipates modest accretion beginning in fiscal year 2026 as Steelcase integration progresses with synergy realization ramping beyond initial partial contributions recorded late FY25 [S1]. Key milestones include successful operational integration focusing on Americas manufacturing footprint rationalization without compromising customer service or brand equity across multiple proprietary brands.

Risks include execution challenges related to integration complexity; macroeconomic uncertainties impacting commercial office demand amid hybrid work trends; potential tariff-related supply chain cost pressures; housing market volatility influencing residential segment sales; input cost inflation potentially constraining margin recovery if price pass-through proves limited over coming quarters [S21], [N2]. Leverage management will remain critical balancing strategic investment needs against covenant compliance requirements.

Operational investments targeting digital transformation aim to simplify customer buying experiences fostering long-term retention essential for competitive positioning amid industry consolidation trends globally.

Conclusion

HNI Corporation’s transformative acquisition of Steelcase repositions it as a leading global competitor in workplace furnishings but carries near-term financial tradeoffs reflected in reduced profitability margins driven by steep transaction costs alongside elevated leverage increasing interest expenses outlays.

Underlying this shift is a strong foundation characterized by diversified channel reach and established leadership across office furnishing solutions complemented by solid residential building products franchise stability.

Management’s commitment toward synergy capture, operational streamlining—especially through globalized manufacturing operations—and disciplined capital returns signals strategic intent focused on medium-to-long-term value creation despite cyclical headwinds ahead.

This analysis is based solely on publicly available financial filings and company disclosures as of March 2026; forward-looking statements are referenced only where explicitly presented by company management without speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments