Huineng Technology’s Early Struggles and Growth Prospects in a Fragmented Market

Huineng Technology faces operational losses and client concentration while seeking growth via early marketing initiatives in a competitive digital services industry.

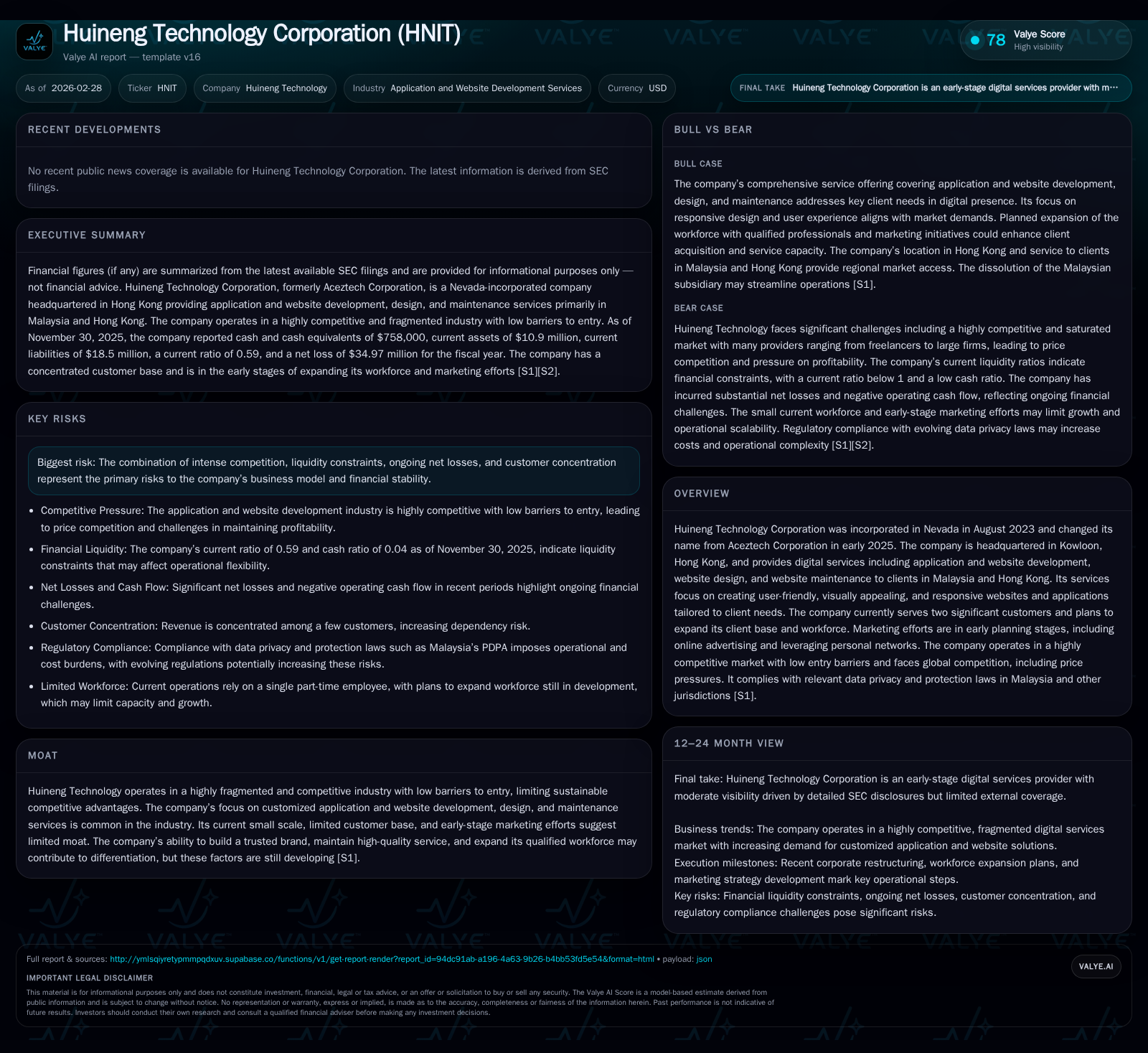

Huineng Technology Corporation, transformed from Aceztech in early 2025, is a Hong Kong-based digital service provider focusing on website and application development tailored to Malaysia and Hong Kong clients. The company endures widening losses and cash flow challenges primarily due to its small scale and dependency on few key customers that contribute over 90% of revenues. Its competitive environment is marked by low entry barriers and global pricing pressures, limiting sustainable differentiation. Growth hinges on expanding the customer base, enhancing workforce capacity, and executing nascent marketing strategies, while financial stability remains constrained by liquidity pressure and lack of capital returns.

Transformation from Aceztech to Huineng Technology: Foundation and Recent Corporate Developments

Huineng Technology Corporation's recent evolution traces back to its origin as Aceztech Corporation, incorporated in Nevada in August 2023. The pivotal corporate transformation occurred in early 2025 when the company rebranded, changing its name to Huineng Technology Corporation and adopting a new stock symbol (HNIT) effective February 18, 2025 as approved by FINRA [S1]. Coinciding with this rebranding was a leadership transition: Kae Ren Tee resigned as director and CEO, succeeded by Guoxiang Ao who assumed multiple executive roles including CEO and President on February 20, 2025 [S1][S12].

The company’s headquarters are established in Kowloon, Hong Kong, although earlier it had incorporated a Malaysian subsidiary (Aceztech Sdn. Bhd.) acquired June 2024 but subsequently dissolved by April 2025, leading to deconsolidation in financial statements [S1]. Huineng’s operational focus lies in providing digital solutions such as application development, website design, and maintenance services catering mainly to clients based in Malaysia and Hong Kong [S1].

This foundational phase reveals an entity still defining its strategic identity amidst market realities — it is at an embryonic stage concerning marketing efforts which remain limited to preliminary online advertising plans and tapping into personal networks for client acquisition [S1]. This period thus marks both opportunity for growth and significant uncertainty around establishing an efficient operational model.

Historical Financial Performance: Tracking Operational Losses Amid Initial Growth

Financially, Huineng Technology’s trajectory has been challenged by increasing losses as it attempts to scale. From fiscal year (FY) 2024 through FY2025, the company witnessed its net income worsen dramatically — moving from a loss of approximately $10.78K in FY2024 to an amplified deficit near $34.97K in FY2025, representing a decline of roughly 224% year-over-year [F1]. Operating income similarly deteriorated with a loss deepening beyond $35.7K at FY2025 year-end [F1].

Operating cash flows paint a similar picture; cash used in operating activities surged over double from an outflow of $27.46K in FY2024 to nearly $55.78K negative cash flow for FY2025 [F1], signaling stressed internal liquidity performance consistent with deepening operating losses.

Notably, capital expenditure remained steady at around $729 annually over both years — indicating that growth investment is minimal or deferred amid liquidity constraints [F1]. The balance sheet reflects these strains as well with shareholders' equity shifting closer towards zero but remaining negative between FY2024 (-$9.55K) and FY2025 (-$5.84K), evidencing accumulated deficits without infusion large enough to restore positive equity levels [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -34968 | -55784 | 729 | -224.3% |

| 2024 | -10784 | -27461 | 729 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -56513 | 598.6 |

| 2024 | -28190 | 112.9 |

Source: SEC companyfacts cache [F1].

The table above encapsulates Huineng's financial stresses through widening operational deficits accompanied by growing negative cash flows amidst flat capital expenditure.

Customer Concentration: Reliance on Few Clients in Malaysia and Hong Kong

One critical risk factor tethering Huineng’s revenue stability is acute customer concentration. Financial disclosures reveal that revenues are overwhelmingly dependent on a handful of major customers — three to four clients accounted for over 90% of total revenue consistently during recent reporting periods spanning late 2024 through mid-2025 across the Malaysia and Hong Kong markets combined [S3][S4][S7][S8].

For example, during the nine months ended August 31, 2024, three customers contributed approximately $18.9 million or about 91% of revenue overall [S3]. This pattern persists into subsequent periods with varying specific clients but maintains high concentration magnitude exceeding typical cautionary thresholds for sustained business viability [S4][S7][S8]. Moreover, outstanding accounts receivable related to these major customers are minimal at reporting dates suggesting solid payment performance but reinforcing risk if any major client were lost.

In digital services industries such as website development where client diversification typically underpins revenue resilience due to projects’ contractual nature and cyclical spend patterns, Huineng’s narrow client portfolio represents vulnerability—any churn or contract non-renewal materially impacts operational continuity.

Competitive Landscape: Challenges of Low Entry Barriers and Global Price Pressures

Huineng operates within a highly fragmented sector typified by low barriers to entry where numerous small-scale firms compete intensely for projects largely commoditized across website development, design, and maintenance offerings [S1]. This lack of proprietary technology or unique service differentiation limits sustainable competitive moats.

Industry dynamics manifest strong downward pricing pressure stemming from global competition including offshore providers who undercut costs leveraging lower wage environments combined with agencies offering packaged solution bundles that squeeze margins further. Firms struggle not only on winning contracts but also maintaining service quality amid compressed budgets.

This environment exacerbates Huineng’s challenge given its limited brand recognition, relatively modest workforce scale compared to larger regional players, and early-stage marketing approaches focused primarily on grassroots networking amidst online advertising pilots rather than proven scalable channels [S1].

Growth Opportunities: Marketing Plans, Workforce Expansion, and Service Differentiation

While these challenges loom large, Huineng articulates growth ambitions centered around expanding its client base beyond its current two main markets — Malaysia and Hong Kong — alongside bolstering its workforce which today remains lean reflecting startup weightings [S1]. Efforts include developing targeted online advertising campaigns designed to enhance visibility coupled with leveraging personal contacts within industry circles aiming for incremental contract wins.

Quality assurance is posited as a strategic lever; the company aims to build reputational strength by delivering user-friendly website experiences customized per client requirements—a tactic intended to differentiate despite commoditized offerings common across competitors [S1]. Success depends critically on translating these nascent strategies into measurable customer acquisition gains while ensuring workforce capability grows responsibly without unsustainable overhead escalation.

Financial Stability: Liquidity Position, Capital Allocation, and Returns Analysis

Examining Huineng's liquidity profile uncovers notable stress points clouding near-term financial flexibility. As of end-FY2025 data shows:

- Current assets totaling roughly $10.9K versus current liabilities near $18.5K yields a current ratio of approximately 0.59 indicating liquidity shortfall prone to solvency concerns if unaddressed promptly;

- Cash reserves remain minimal at around $758 signaling tight working capital buffer against daily operating expenses;

- No dividends have been issued nor share repurchases conducted likely due to accumulated losses evidenced by negative shareholders’ equity near -$5.8K further constraining shareholder distributions capability;

- Approximate return on equity calculated using reported net loss (-$34.97K) against negative book value (-$5.84K) yields distorted metric reflective of ongoing value erosion rather than positive returns given capital deficits;

- Free cash flow approximates strongly negative near -$56.51K confirming deficient internal generation capacity amid rising cash burn trends.

Collectively these metrics demonstrate constrained capital allocation possibilities limiting proactive measures such as investing heavily into growth initiatives or weathering prolonged client acquisition cycles absent external financing or operational turnaround.

What Investors Should Monitor: Milestones, Cash Flow Trajectories, and Business Expansion

Absent explicit forward guidance or milestones disclosed publicly for HNIT ([N#]), stakeholders tracking Huineng must orient toward monitoring several critical forward-looking indicators:

- Progressive narrowing of net losses would suggest improving cost control or expanding revenues potentially stemming from diversified clientele;

- Measurable diversification beyond current four dominant customers lowering single-client revenue dependence risks;

- Successful execution of early marketing campaigns converting into firm pipeline expansion measurable via contract wins or new customer onboarding statistics;

- Stabilization or improvement in liquidity ratios signaling working capital adequacy upkeep;

- Incremental workforce growth aligned with sustainable revenue scales rather than disproportionate fixed cost increments.

These markers will serve as barometers for whether Huineng can overcome inherent industry fragmentation hurdles plus internal resource restraints towards forging durable growth platform within the competitively agnostic digital services ecosystem.

Disclaimer: This report is prepared solely for informational purposes without recommending any investment action regarding Huineng Technology Corporation securities. Financial figures are directly cited from official filings without speculative adjustments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments