Hormel Foods Corp’s Turnaround: Restructuring Drives New Growth Opportunities

Hormel Foods’ recent operational restructuring and strong liquidity position underpin its strategic shift toward enhanced efficiency and growth resilience.

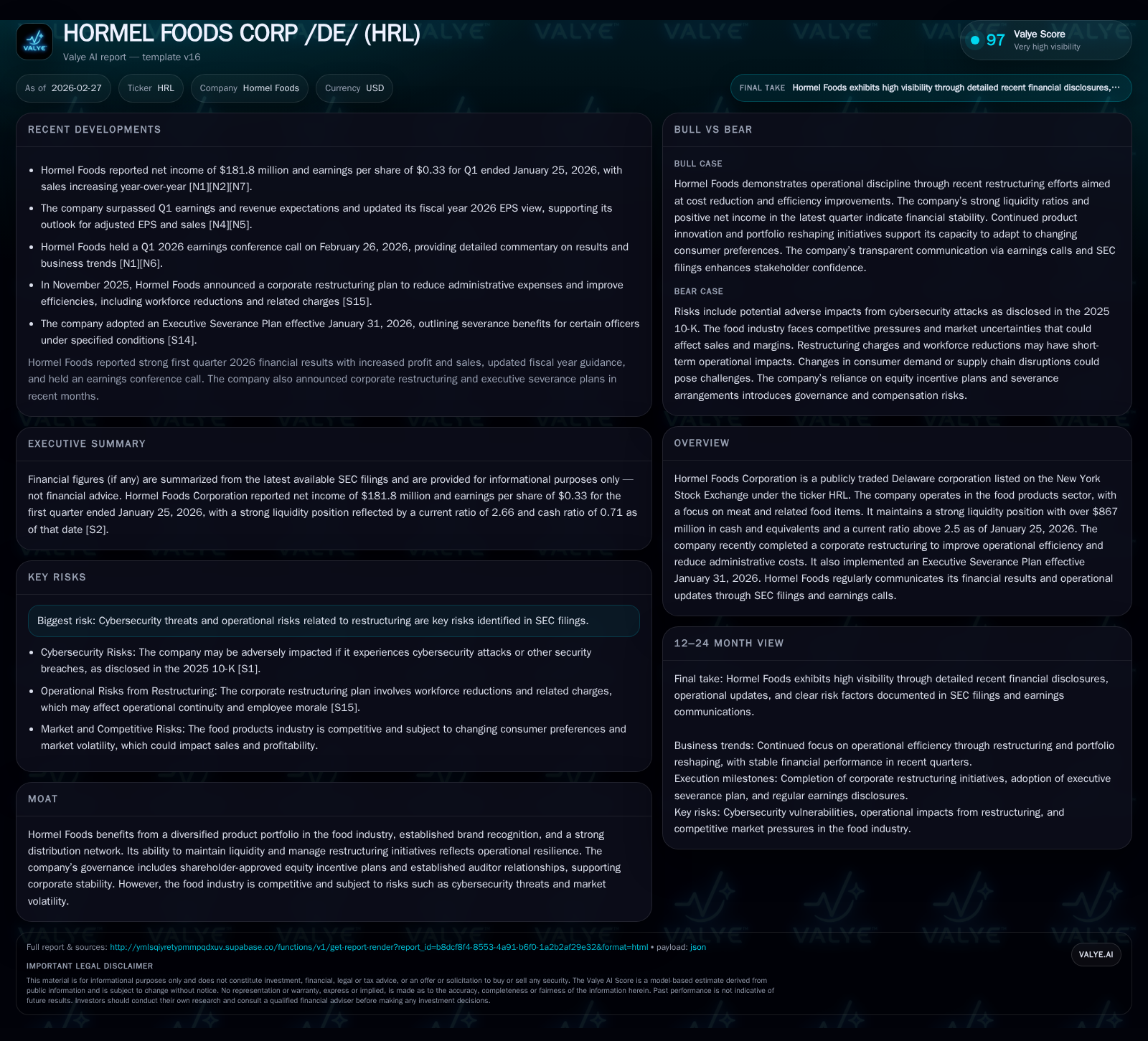

Hormel Foods Corporation has embarked on a significant turnaround effort highlighted by a corporate restructuring aimed at cutting administrative costs and improving operating efficiency. Recent financials reflect margin compression with operating income and net income declining substantially year-over-year, primarily influenced by restructuring charges. Despite these near-term earnings pressures, the company maintains robust liquidity, evidenced by over $867 million in cash and equivalents and a current ratio above 2.5. With an updated capital allocation approach focusing on steady dividend growth and disciplined investment, Hormel leverages its diverse portfolio and strong brand recognition to navigate sector challenges including cybersecurity risks and market volatility. Key upcoming milestones include monitoring margin recovery post-restructuring and sustaining revenue gains within evolving consumer landscapes.

Evolving Performance: A Mixed Picture of Recent Financials

Hormel Foods' financial trajectory through fiscal 2025 illustrates clear headwinds tied to its ongoing turnaround initiatives. Revenue has exhibited modest declines, registering a 5.1% drop year-over-year from $2.62 billion in FY2024 to approximately $2.49 billion in FY2017 (earliest comprehensive data point) — although exact recent revenue trends are not fully delineated beyond this snapshot [F1]. More pronounced are contractions in profitability metrics: operating income decreased sharply by nearly one-third (-32.7%), descending from $1.07 billion in FY2024 to $718.6 million in FY2025; net income echoed this trend with a 40.6% decline year-over-year to $478.2 million [F1]. Operating cash flow also contracted by a third (-33.3%) to $845 million in FY2025, while capital expenditures rose notably by over 21%, signaling targeted reinvestment amid tightening margins [F1]. These declines largely reflect the immediate cost burdens stemming from restructuring actions alongside adverse market dynamics influencing margins.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 478 | 845 | 719 | 311 | -40.6% |

| 2024 | 805 | 1267 | 1068 | 256 | +1.4% |

| 2023 | 794 | 1048 | 1072 | 270 | -20.6% |

| 2022 | 1000 | 1135 | 1313 | 279 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 633 | 0 | 534 |

| 2024 | 615 | 0 | 1010 |

| 2023 | 593 | 12 | 778 |

| 2022 | 558 | 0 | 856 |

Source: SEC companyfacts cache [F1].

*2017 revenue figure used due to limited recent disclosure [F1].

Operational Restructuring: The Heart of Efficiency Gains

The catalyst for much of Hormel’s recent financial variability is its comprehensive corporate restructuring program announced in November 2025 to streamline operations and reduce administrative burden [S14]. This plan encompasses voluntary early retirements, role eliminations totaling approximately 250 positions primarily across corporate and sales functions, as well as modifications to benefit programs—intended to foster leaner cost structures over time without compromising growth investments.

This initiative is estimated to incur restructuring charges between $20 million and $25 million predominantly reflected during Q4 FY2025 and Q1 FY2026, with a substantial portion attributable to pension liabilities, severance costs, stock compensation, and benefits outlays [S14]. Management underscores that while these represent short-term earnings headwinds, they set the stage for enhanced operational agility.

Supporting this shift is the formal adoption of an Executive Severance Plan effective January 31, 2026 designed to provide structured severance benefits aligned with executive transitions arising from organizational changes [S7][S12]. This plan articulates severance payments based on salary plus bonus multiplied by designated severance factors (e.g., CEO factor at two times base), along with COBRA premium reimbursements and accelerated equity vesting—all conditioned on standard release agreements.

Market Challenges and Sector-Specific Headwinds

Hormel operates within an intensely competitive food products segment dominated by evolving consumer preferences, volatile input costs, regulatory complexity, and digital transformation pressures. Notably, risk disclosures prominently cite cybersecurity threats as material vulnerabilities potentially impeding supply chain continuity or compromising sensitive data [S1][S6]. The intensifying sophistication of cyber-attacks necessitates sustained vigilance against operational disruption.

Furthermore, macroeconomic volatility affecting commodity prices weighs on margin stability given input cost pass-through lags common within meat processing sectors—a dynamic requiring proactive price management strategies embedded within Hormel’s operating model [S4][S5]. These external headwinds compound internal transitional risks amid the restructuring effort.

Growth Potential Anchored in Portfolio Diversification

Despite short-term pressures, Hormel retains structural growth levers derived from its broad product mix encompassing various branded meat-based food items distributed widely across retail channels [N7][F1]. This diversification dilutes exposure to single-category volatility while fostering stable revenue streams resilient against individual market shifts.

The combination of established brand equity paired with expansive distribution network infrastructure forms a formidable moat supporting volume retention even amidst evolving consumer health-conscious trends and alternative protein proliferation themes documented within the sector analysis context (analysis).

Capital Allocation Strategy: Balancing Shareholder Returns and Future Investment

Hormel’s balance sheet exhibits solid liquidity fundamentals highlighted by $867.9 million cash & equivalents and current assets exceeding liabilities with a current ratio of approximately 2.66 as of January 2026 — positioning it well for both near-term obligations and strategic capital deployment [F1][S23].

Capital allocation pivots toward maintaining steady dividend increases observed through FY2025 ($633 million total dividends paid), reflecting shareholder return consistency despite refraining from share repurchases since FY2024 likely due to ongoing restructuring investments [F1][S8]. Operating cash flow net of capex remains positive at over $534 million providing adequate FCF cushion for reinvestment along with distributions.

Return on equity approximates a moderate level near 6.1% underpinned by equity base expansion relative to contracting earnings but remains susceptible to improvement upon successful margin restoration post-turnaround [F1].

Governance Enhancements and Executive Compensation Plans

Corporate governance developments include shareholder approval in January 2026 of the new Equity Incentive Plan superseding the prior cycle—enabling targeted long-term incentives such as stock options, performance shares, and restricted stock units designed to align employee and director interests with performance outcomes [S7][S8].

Concurrently, adoption of the Executive Severance Plan reflects adaptive compensation governance balancing retention incentives with prudent oversight around executive departures contextualized within strategic realignment imperatives [S11][S12]. This multi-faceted approach underscores thoughtful management stewardship through transitional phases.

Cybersecurity Vigilance Amidst Increasing Digital Risks

SEC filings emphasize cybersecurity risk as a top-tier threat vis-à-vis potential operational disturbances or compromise of proprietary information critical to production and distribution functions [S1][S6]. Hormel has hence adopted continuous monitoring protocols complemented by evolving defense layers calibrated for threat detection and rapid response—acknowledging heightened cyberattack sophistication targeting vital food supply chains (analysis).

Key Milestones Ahead and What Investors Should Monitor

Investors should principally focus on quarterly earnings releases following Q1 FY2026 reflecting initial post-restructuring impact assessments including margin trajectory signals as efficiencies become realized [N2][N5][N9]. Updates on organic sales growth trends combined with raw material cost inflation pass-through remain crucial barometers in evaluating turnaround durability.

Additional watchpoints include progress metrics around workforce alignment outcomes announced during late-2025 initiatives alongside any adjustment in capital allocation priorities reflective of emerging cash flow trends or macro shifts.

Disclaimer: This report synthesizes publicly available information from SEC filings and recent news sources without offering investment advice or recommendations. All financial data are based explicitly on reported figures within cited references.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments