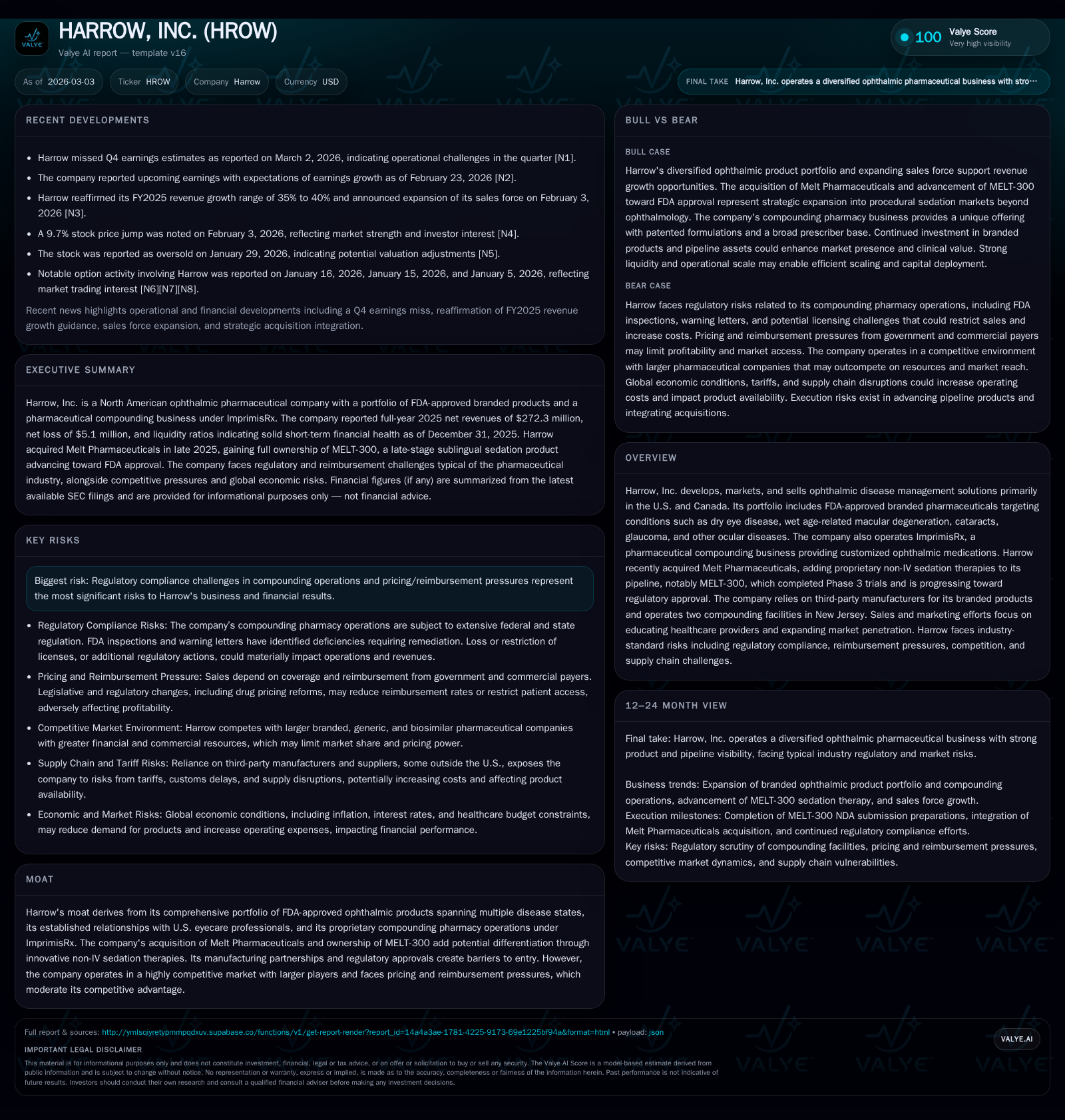

Harrow, Inc. Expands Ophthalmic Portfolio with Increased Revenues and Regulatory Headwinds

Harrow’s diversified ophthalmic pharmaceutical offerings and compounding services underpin recent growth while regulatory challenges and legal disputes remain key risks.

Harrow, Inc. has demonstrated robust revenue growth over recent years driven by its expanding FDA-approved branded ophthalmic products and its ImprimisRx compounding segment. The company’s acquisition of Melt Pharmaceuticals broadens its pipeline with innovative sedation therapies poised for regulatory approval. Nonetheless, ongoing legal disputes and regulatory scrutiny in its compounding operations, coupled with pricing pressures, temper near-term outlooks. Harrow reported strong operating income growth in 2025 but remains unprofitable on a net basis due to non-operating factors and corporate expenses.

Company Overview

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | 44 | 31 | 1 | +70.6% |

| 2024 | -17 | -22 | 9 | 2 | +28.4% |

| 2023 | -24 | 4 | 0 | 1 | -73.3% |

| 2022 | -14 | 2 | 2 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 43 | -9.8 |

| 2024 | -24 | -25.1 |

| 2023 | 2 | -34.5 |

| 2022 | -1 | -51.0 |

Source: SEC companyfacts cache [F1].

Harrow, Inc. operates primarily in the U.S. and Canadian markets providing FDA-approved ophthalmic pharmaceuticals targeting diseases such as dry eye disease, wet age-related macular degeneration (AMD), cataracts, glaucoma, among others [S1][S4]. The company also runs ImprimisRx, its pharmaceutical compounding business specializing in customized ophthalmic medications. Recently, Harrow acquired full ownership of Melt Pharmaceuticals, adding non-IV sedation treatment candidates like MELT-300 that recently completed Phase 3 trials [S1][N4].

The firm's strategy blends established branded product offerings with the compounding pharmacy platform to cover a broad spectrum of ophthalmic needs. It markets products including IHEEZO (ocular anesthesia gel), VEVYE (cyclosporine solution for dry eye), BYOOVIZ and OPUVIZ biosimilars targeting wet AMD and other retinal conditions [S1]. Manufacturing is outsourced to third parties for branded products while two New Jersey-based facilities produce compounded drugs under ImprimisRx [S1][S27].

Historical Performance and Growth Drivers

Between FY2023 and FY2025, Harrow's net revenues increased markedly from approximately $130 million to $272 million [F1][S4]. This surge was driven primarily by explosive growth in the Branded segment—from about $50 million in 2023 to nearly $196 million in 2025—reflecting successful commercialization and portfolio expansion [F1][S15]. Key products IHEEZO and VEVYE accounted for the largest shares of branded revenues at roughly 30% and 33%, respectively, by end-2025 [S4].

Conversely, ImprimisRx revenues declined slightly from $83.5 million in 2024 to $76.5 million in 2025 but remain significant at ~28% of total sales [S4]. The mixed trend here reflects regulatory scrutiny constraining some formulations despite initiatives to scale pharmacy operations [S9][S25].

Profitability metrics improved dramatically: operating income increased about 246% year-over-year in 2025 to $30.5 million—driven by higher gross margins on branded sales combined with cost discipline [F1][S26]. However, net income remained negative (-$5.1 million) despite this operating improvement due partly to elevated corporate expenses, interest costs associated with debt financing arrangements secured as recently as late-2025 [F1][S22], and ongoing legal costs [S1].

Cash flow from operations turned strongly positive at over $43 million in FY2025 versus a negative $22 million outflow the prior year—a reflection of improved working capital management alongside earnings progress [F1]. Capex spending decreased more than 40% to below $1 million as Harrow focused resources on market development rather than fixed asset investments [F1]. The firm maintains a healthy current ratio above 2x supported by liquidity sources including cash balances near $73 million plus a recently negotiated $40 million revolving credit facility maturing in 2030 [F1][S22].

| FY | Rev ($M) | Branded ($M) | ImprimisRx ($M) | OpInc ($M) | Net ($M) | CFO ($M) | Capex ($M) |

|---|---|---|---|---|---|---|---|

| 2023 | 130 | 50 | 80 | 0.43 | -24.4 | 3.8 | 1.46 |

| 2024 | 200 | 116 | 83 | 8.8 | -17.48 | -22.2 | 1.60 |

| 2025 | 272 | 196 | 77 | 30.5 | -5.14 | 43.9 | 0.89 |

Table: Harrow Consolidated Financial Highlights [F1][S4][S15]

Future Growth Prospects

Harrow’s expansions center on bolstering its branded product pipeline and scaling compounding capabilities while navigating regulatory compliance challenges specific to the latter.

The expected mid-2026 commercial launch of BYOOVIZ—the first FDA-approved LUCENTIS biosimilar—and subsequent OPUVIZ launch planned for mid-2027 provide potential revenue catalysts [S1]. These biosimilars target large patient populations facing retinal diseases; their success depends on market uptake amid competitive pressure from originator biologics like Lucentis and Eylea.

The Melt Pharmaceuticals acquisition adds MELT-300, an innovative non-IV sedation therapy for procedural anesthesia which has completed Phase 3 trials and is progressing toward FDA approval—a different therapeutic area that could diversify revenue if approved successfully [N4][S1].

ImprimisRx faces continuing regulatory oversight following recent FDA inspections yielding warning letters related to manufacturing practices at its NJ-based out-of-state outsourcing facility (NJOF). While remediation efforts continue voluntarily under FDA supervision with improvements acknowledged by regulators, any further restrictions or loss of licenses could materially impact compounded product sales [S9][S11][S25]. Additionally, state-level regulatory actions could compound operational risks.

Pricing pressure remains persistent across the industry with government payors implementing rebate structures under Medicare/Medicaid reforms following the Inflation Reduction Act provisions along with private payor constraints limiting pricing flexibility [S6][S10]. These factors could cap margins on both branded and compounded products.

Further uncertainty surrounds tariff implications on active pharmaceutical ingredients (API) sourced globally which may increase input costs despite mitigation efforts involving dual sourcing or tariff engineering [S13].

Returns and Capital Allocation

Although profitability has yet to be consistently achieved net of all expenses—FY2025 net loss narrowed significantly—the sizable operating income improvement suggests growing operational efficiency [F1]. Return on equity approximates negative 9.8% based on FY2025 results reflecting residual losses despite equity base growth from roughly $28 million at end-2022 to over $52 million at end-2025 [F1].

Free cash flow calculated as operating cash flow less capital expenditures reached approximately $42.9 million on fiscal year-end basis—a sign of solid internal funding capacity without reliance on external financing for core operations currently [F1].

Harrow’s recent credit facility agreements provide additional financial flexibility but come with covenants limiting certain capital deployment activities such as asset disposals or debt incurrence beyond thresholds [S22][S24]. The company has not reported share repurchases or dividend payments in recent history which aligns with standard biotech/pharma growth phase capital retention strategies.

Legal Risks and Regulatory Considerations

Legal proceedings notably include a case involving subsidiary ImprimisRx against Ocular Science entities resulting in a jury verdict awarding nearly $11.2 million plus post-judgment interest after adjustments; however, collections remain uncertain due to pending appeals restraining enforcement action currently [S1][S7]. Additionally, ongoing litigation related to product liability inherent in ophthalmic pharmaceuticals requires adequate insurance coverage but introduces expense volatility.

FDA engagement continues closely around compounding operations following past inspections revealing repeat observations requiring enhanced quality system processes within NJOF facilities—including warnings issued in 2017, again in recent years—and voluntary product recalls implemented to remediate risks [S9][S11][S25][S27]. State board actions such as those from California pose further operational uncertainty although current geographic sales diversification mitigates single-market dependency risk somewhat.

Political landscape factors such as government shutdowns can delay FDA review cycles impacting submission timelines for new therapies or generics including biosimilars [S6][S17], alongside healthcare policy evolutions affecting coverage decisions by CMS or competitors’ formulary placements which indirectly influence adoption rates.

What To Watch Going Forward (Analysis)

Absent explicit forward guidance demarcated by management for upcoming periods beyond reaffirmed FY2025 revenue growth projections between 35–40% supported by expanded sales force investments noted last quarter ([N4]), investors should monitor:

- Commercial ramp success of BYOOVIZ starting mid-2026 including uptake vs originator biologics;

- MELT-300 regulatory approval progression timeline amid FDA filings;

- Regulatory developments impacting ImprimisRx compounding licenses especially renewal outcomes across states;

- Impact of pricing reforms through Medicare/Medicaid rebate mechanisms or formulary shifts;

- Execution against tariff inflation mitigation strategies;

- Legal outcomes tied to ongoing appeals affecting contingent liabilities recognition;

- Cash flow conversion stability sustaining scaling initiatives.

Conclusion

Harrow's trajectory embodies an aggressive expansion within ophthalmic disease management through both proprietary pharmaceuticals and personalized compounding services augmented by targeted acquisitions like Melt Pharmaceuticals broadening therapeutic reach beyond ophthalmology sedation solutions. Its strong revenue growth combined with sizeable operating income improvement cements operational momentum despite net losses persisting alongside legal/regulatory headwinds. Ultimately balancing innovation pipeline rollout timing against intricate drug pricing environments alongside rigorous compliance regimes will dictate whether Harrow can translate these gains into sustained profitability over medium term horizons.

Disclaimer: This analysis is intended solely for informational purposes based on data available as of early March 2026. It does not constitute investment advice or recommendations regarding buying or selling securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments