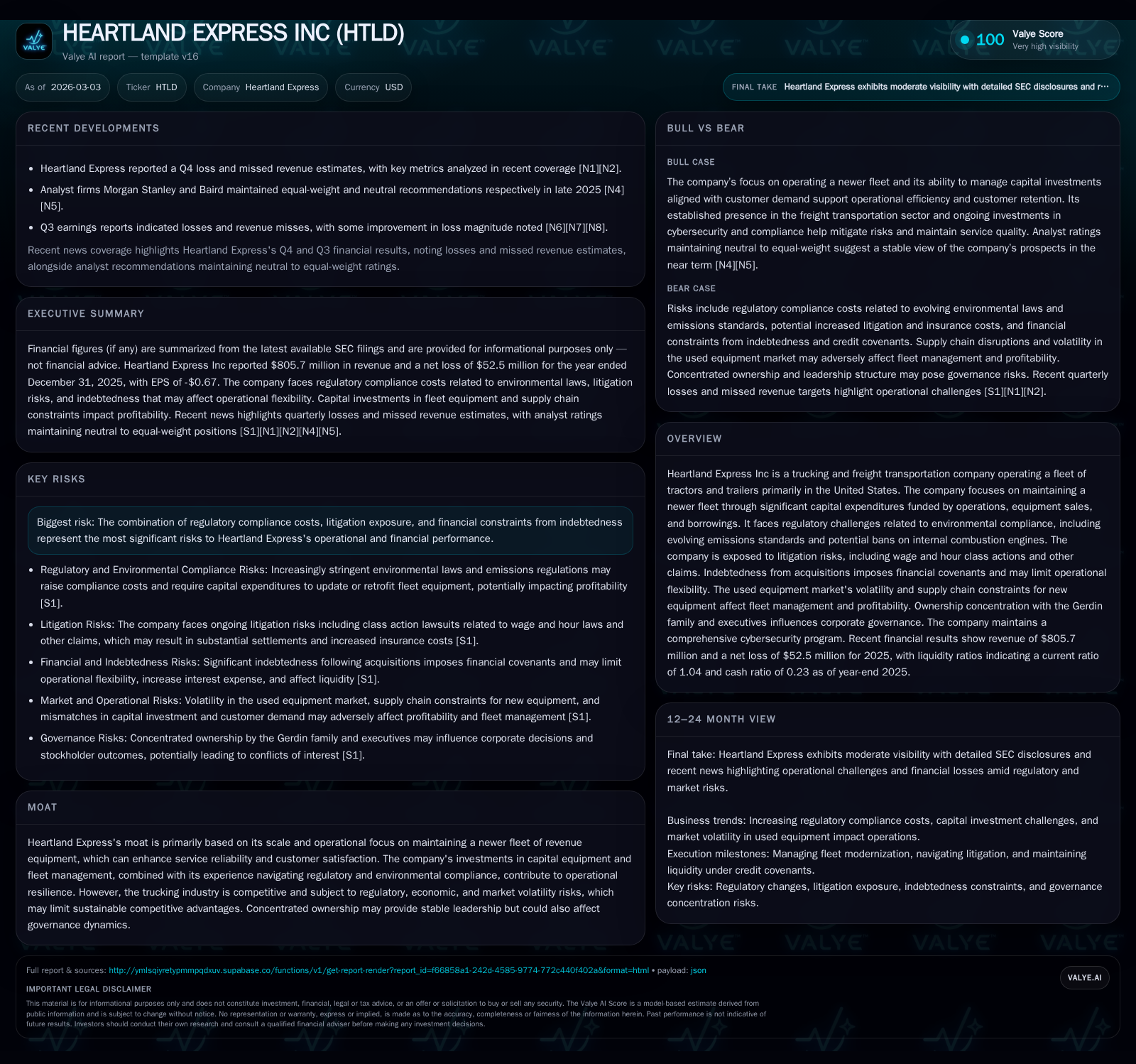

Heartland Express Faces Profitability Pressure from Revenue Declines and Elevated Capital Costs

The trucking operator contends with a shrinking top line, intensifying regulatory compliance expenses, and fleet investment challenges that weigh on its financial performance.

Heartland Express Inc reported a significant contraction in revenues and operating income in fiscal year 2025 compared to prior years, reflecting ongoing industry headwinds and operational challenges. The company’s strategic emphasis on fleet modernization drives substantial capital expenditures amid a softened used equipment market and supply chain constraints, contributing to negative free cash flow despite positive operating cash flows. Regulatory developments around emissions and litigation risks further complicate the outlook. While dividends and share buybacks continue at moderate levels, leverage and covenant considerations constrain financial flexibility.

Introduction

Heartland Express Inc (HTLD) operates primarily as a freight trucking service provider across the United States, focusing heavily on maintaining a late-model revenue equipment fleet to optimize service reliability and efficiency [S1]. The company’s financial results for the fiscal year ended December 31, 2025 show pronounced challenges across multiple fronts: top-line contraction, operational losses, heightened capital expenditures, and increased regulatory compliance costs. This report synthesizes these facets alongside governance dynamics to provide a comprehensive view of Heartland Express’s current positioning.

Historical Performance Trends

Heartland Express’s annual revenues peaked above $1.2 billion in FY2023 but declined sharply thereafter. In FY2025, total revenue dropped to approximately $805.7 million, representing a 23.1% decrease from $1.047 billion in FY2024 [F1]. Operating income swung dramatically negative from -$20.2 million in FY2024 to -$57.4 million in FY2025 — an 183.7% year-over-year decline. Correspondingly, net income contracted from a loss of $29.7 million to a larger loss of $52.5 million [F1].

Operating cash flows declined by about 38% YoY to $89.3 million in FY2025 but remained positive [F1]. However, free cash flow turned negative due to increased capital investments in the fleet (see next section).

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 806 | -52 | 89 | -57 | -23.1% | -76.5% |

| 2024 | 1048 | -30 | 144 | -20 | -13.2% | -301.2% |

| 2023 | 1207 | 15 | 165 | 42 | +24.7% | -88.9% |

| 2022 | 968 | 134 | 195 | 188 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 10 | -67 |

| 2024 | 6 | 7 | 35 |

| 2023 | 6 | 0 | -43 |

| 2022 | 6 | 0 | 34 |

Source: SEC companyfacts cache [F1].

Table: Financial Summary for Heartland Express (FY2022-FY2025)

Fleet Investment & Capital Expenditures

A core element of Heartland Express’s strategy is maintaining a newer average age fleet of tractors and trailers to boost efficiency and customer satisfaction [S1], [S7]. Capital expenditures rose steeply by roughly 43% in FY2025 to $156 million from $110 million the year prior [F1], underscoring continued aggressive reinvestment.

This high level of capex partly reflects rising prices for new equipment driven by factors such as stricter emissions regulations impacting engine design costs; tariffs enacted since April 2025 further elevate component prices [S16]. Trade disputes contribute supply-side constraints affecting availability of trucks [S18]. Maintaining this modern fleet amidst inflationary input costs pressures margins.

The used equipment market has softened from prior peaks seen before FY2023 which diminishes gains on sale of replaced vehicles; combined with high purchase prices for new equipment this dynamic generated negative free cash flow of approximately $66.9 million last year despite positive operating cash flow [F1], [S7], [S18]. This mismatch between spending and asset disposition values introduces added profitability risk.

Regulatory & Legal Challenges

Environmental regulation remains a salient risk vector for Heartland Express given its reliance on diesel-powered vehicles subject to evolving emissions standards [S1], [S16]. New laws could mandate costly retrofits or accelerated fleet replacement if internal combustion engines face bans in certain jurisdictions.

Uncertainty around legislation also engenders compliance cost volatility – recent EPA proposals to withdraw federal greenhouse gas regulations risk patchwork state-level rules raising complexity [S16], [S21]. Compliance challenges not only inflate direct expenses but may require disclosure of operational metrics historically confidential.

Litigation exposure is pronounced: the company faces class action lawsuits alleging federal/state wage-and-hour violations including unpaid overtime and meal breaks as well as personal injury claims typical in trucking operations [S6], [S19]. These legal cases impose financial settlement risks plus potential insurance premium increases.

Financial Structure & Capital Allocation

Heartland Express carries substantial indebtedness related largely to acquisitions such as CFI and Smith Transport; debt covenants limit leverage ratio to below approximately 2.75x EBITDA with other restrictions on distributions and additional borrowings [S9], [S10]. Such constraints force careful capital management prioritizing required fleet renewals while sustaining liquidity.

Balance sheet data as of December 31st shows equity declined slightly YoY to around $755 million; current ratio near unity (1.04) points to working capital tightness given liabilities slightly exceeding current assets by a small margin [F1], [S9]. Cash on hand stands around $18 million – adequate for near-term requirements but susceptible if operating conditions worsen further.

Capital returns continue at a moderate scale: dividends were consistent at approximately $6.2 million paid for FY2025 while share repurchases resumed totaling just under $10.4 million following no buybacks earlier; this demonstrates some confidence balanced against liquidity preservation needs [F1], [S12], .

Governance & Ownership Dynamics

Concentrated ownership with the Gerdin family controlling roughly 45% of common stock consolidates decision-making power significantly; Michael J. Gerdin serves simultaneously as CEO/President/Chairman reinforcing executive influence over corporate governance structures [S15].

While this arrangement simplifies leadership continuity amid external pressures it poses possible conflicts of interest risks between majority owners and minority shareholders particularly regarding strategic directions or sustainability initiatives.

Future Outlook & Considerations (Analysis)

Looking ahead into calendar year 2026 and beyond:

- Sustaining profitability depends heavily on navigating tighter freight markets possibly intensified by macroeconomic slowdowns impacting load volumes.

- Rising capital expenditure needs driven by environmental mandates may pressure free cash flow absent offsetting pricing power or cost efficiencies.

- Successful mitigation or resolution of litigation matters would reduce financial uncertainty.

- Ongoing supply chain volatility for new trucks will remain a challenge; ability to optimize asset deployment critically important.

- Regulatory shifts toward zero-emission vehicles could spur future capex spikes or disrupt current operating models.

- Monitoring covenant compliance will be essential to avoid restrictions constraining acquisitions or dividend policies.

- Investor sentiment may be influenced by ESG ratings reflecting environmental risk posture given growing prominence of sustainability considerations among stakeholders.

No specific forward guidance was disclosed recently beyond qualitative remarks regarding continuing investments in fleet renewal and risk mitigation efforts [N1], [N2], [S1]. Given the sharp revenue decline coupled with elevated costs apparent from recent reporting periods ([F1]), watching upcoming quarterly earnings releases for signs of stabilization or further deterioration will be key milestones.

Conclusion

Heartland Express faces significant near-term headwinds from declining freight volumes reflected in falling revenue alongside material pressure from accelerated capital expenditures necessary to maintain its fleet quality amid increasingly stringent emissions regulations and challenging market dynamics for used equipment sales. Coupled with litigation exposures and debt covenant constraints stemming from prior acquisitions this environment demands disciplined financial management. Governance stability under concentrated ownership offers leadership consistency yet may create frictions regarding shareholder interests alignment going forward.

Investors should closely monitor regulatory developments affecting internal combustion engine usage across states as well as legal outcomes related to labor claims that could materially affect earnings prospects beyond operational performance metrics reported through fiscal year-end results in early 2026.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of March 3rd ,2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments