Hycroft Mining’s Transition from Production to Exploration Amid Significant Cash Reserves and Operational Uncertainty

Hycroft Mining Holding Corp is focused on redeveloping its Nevada gold-silver mine, balancing exploration advances against the challenge of resuming commercial production.

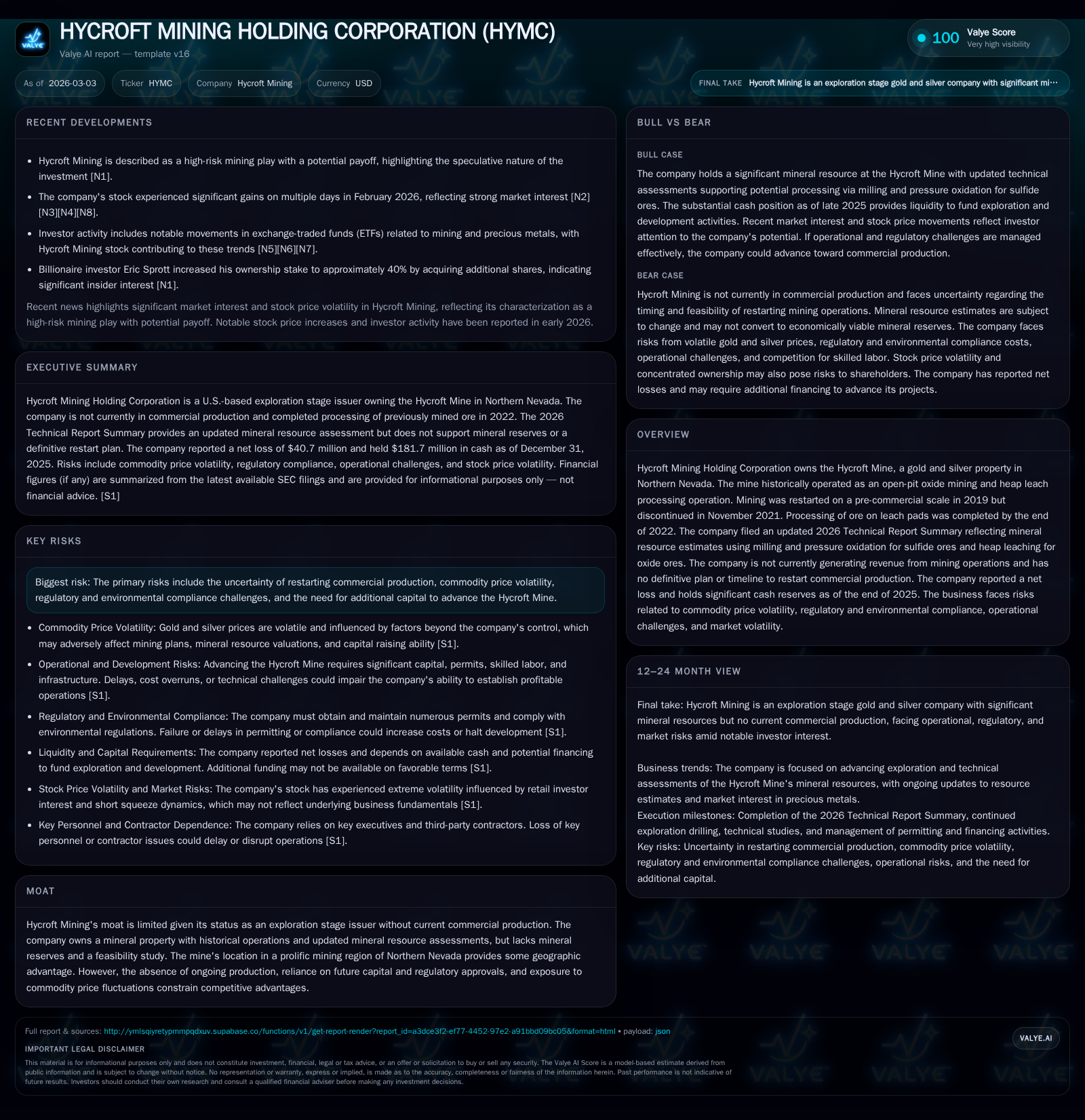

Hycroft Mining Holding Corp owns the Hycroft Mine in Northern Nevada, a historically productive gold and silver property that ceased commercial operations in late 2021. Since then, the company has transitioned to an exploration and development stage firm, emphasizing technical studies and mineral resource reassessment while maintaining a substantial cash position exceeding $180 million at the end of 2025. Despite the updated 2026 Technical Report Summary presenting an initial assessment for sulfide ore milling and pressure oxidation processing, Hycroft lacks mineral reserves or a feasibility study, underscoring uncertainty about commercial viability and timing of potential mine restart. The business faces operational, regulatory, and commodity price risks that currently cap near-term growth prospects.

Company Overview and Historical Performance

Hycroft Mining Holding Corporation (NASDAQ: HYMC) owns the Hycroft Mine—a gold and silver mining property located approximately 54 miles northwest of Winnemucca in Northern Nevada's prolific mining belt. The mine historically operated as an open-pit oxide mining asset utilizing heap leach processing.

Mining restarted on a pre-commercial basis in 2019 following prior production cessation but was discontinued in November 2021. Post-mining processing of ore already placed on leach pads was completed by December 31, 2022 [S1]. No subsequent commercial mining operations have taken place since.

Financially, Hycroft reflects its shift to an exploration stage company with no revenue reported from mining operations since before 2019 [F1]. The most recent full-year results for FY2025 reveal continued operating losses totaling approximately $44.5 million alongside a net loss of roughly $40.7 million. This marks a slight improvement in net loss compared to prior years but underscores ongoing cash burn to sustain corporate functions and advance technical evaluations rather than generate cash flow from production [F1].

Operating cash flow remains negative across recent years: -$82.9 million in FY2025 alone versus a capex spend of just $0.56 million suggests a focus on maintenance costs and selective drilling activities versus large-scale development or capital projects [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -41 | -83 | -44 | 564000 | +33.2% |

| 2024 | -61 | -36 | -44 | 1253000 | -10.7% |

| 2023 | -55 | -41 | -46 | 1070000 | +9.5% |

| 2022 | -61 | -35 | -53 | 951000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -83 | -19.0 |

| 2024 | -37 | 182.2 |

| 2023 | -43 | -434.8 |

| 2022 | -36 | -96.1 |

Source: SEC companyfacts cache [F1].

Financials presented in USD millions; losses reflect continued focus on exploration/study over production.

Equity values shifted from positive $63 million at end-2022 to negative $33 million at end-2024 before recovering strongly to roughly $214 million by year-end 2025—likely reflecting capital raises or mark-to-market adjustments [F1]. This equity volatility aligns with notable stock price swings during this period driven partly by speculative retail interest as described below.

Future Growth Prospects

The company recently filed an updated Technical Report Summary ("TRS") dated January 21, 2026—the "2026 Hycroft TRS"—which supersedes the previous version from March 27, 2023. This new report integrates drilling data through late-2024 and associated assay results received through March 17, 2025.

Critically, it presents an initial assessment of mineral resources using a combined processing approach: milling plus pressure oxidation (POX) for sulfide ores and heap leaching for oxide ores—a departure from historical heap leaching alone [S1], [S18], [S26]. This engineering evaluation seeks to unlock additional value from sulfide mineralization previously uneconomical to treat by conventional methods.

However, despite this advancement:

- The TRS does not support disclosure of mineral reserves.

- No preliminary feasibility or feasibility study has been completed.

- There is no definitive timeline to resume commercial production.

- Mineral resource estimates remain subject to volatility based on metal prices set (gold at $3,100/oz; silver at $36/oz), processing assumptions, and further exploratory success.

- Metallurgical recoveries established via small-scale tests have not yet been confirmed at production scale.

The company emphasizes that restarting mining will depend heavily on factors beyond its direct control—including commodity prices for gold and silver, access to affordable development capital amid market conditions, environmental permitting outcomes, regulatory approvals including several levels of state and federal oversight given its Nevada location on lands involving both private mineral rights and Bureau of Land Management claims—and successful demonstration that sulfide processing technologies can be economically implemented [S1], [S4], [S10], [S20], [S25].

Management has articulated plans for targeted exploration focused toward higher-grade zones within the Hycroft deposit coupled with trade-off studies analyzing alternatives such as roasting vs POX processes for sulfides during calendar year 2026 but remains cautious about timelines given inherent uncertainties [S25].

These investments aim to ultimately support submission of a feasibility study requisite for defining mineral reserves—which under SEC rules requires demonstrated economic viability—and provide a pathway back into commercial-scale production if justified.

Returns and Capital Allocation

Because no commercial mining revenue is currently generated nor are operational profits realized given care-and-maintenance status:

- Operating losses are sustained year-over-year with no near-term positive cash flows expected.

- Operating cash outflows expanded sharply to nearly $83 million in FY2025 versus sizable but smaller outflows previously.

- Capital expenditures remain negligible in comparison ($564 thousand), underscoring minimal ongoing physical asset development but continuing spending on geological evaluation efforts or corporate activities.

- The company possesses liquidity strength with over $181 million cash equivalents at year-end providing runway for exploration work and corporate expenses absent revenue inflows [F1], [S13].

- No dividends have been paid historically nor are declared—appropriate given reinvestment needs amid exploration status; also consistent with regulatory filings cautioning investors around expectations for distributions given financial position [S11].

- No share repurchases were noted in recent filings; focus has instead been raising equity capital when required leading up to new equity incentive plans finally authorized late in 2025 aiming to re-align management compensation with shareholder interests following prior limited awards due to share availability constraints [S27].

Return on Equity based on net loss relative to December-end equity suggests a negative ROE near -19% for FY2025 highlighting current destruction of book value consistent with exploration-stage companies without revenue streams yet realized [F1].

Eric Sprott’s affiliated entity holds approximately a 38% stake in voting securities potentially influencing governance decisions including financing strategy or sale options which may impact capital allocation choices going forward amid industry volatility [S14].

Industry Context and Investment Considerations

The precious metals mining sector remains intrinsically tied to volatile commodity cycles influenced by macroeconomic drivers such as inflation expectations, currency movements (notably USD strength), geopolitical risk premiums impacting safe-haven demand for gold and silver metals. Processing technologies also impose significant capital intensity hurdles as mines transition from oxide ores treatable by heap leach methods toward sulfide deposits requiring complex metallurgical treatments like pressure oxidation or roasting—a costly undertaking laden with technical risk.

Moreover regulatory scrutiny around environmental compliance including water resource management at heap leach facilities—as well as mine reclamation funding obligations—adds further cost layers often underestimated early in redevelopment phases. Hycroft’s legal history involving warrant holder litigation introduces additional governance noise though presently judged unlikely materially adverse financially but nonetheless capable of distracting management bandwidth and possibly limiting financial flexibility during critical phases of asset advancement [S4], [S5], [S6], [S14].

Retail investor activity reflected through market volatility appears decoupled from fundamental performance with documented episodes of short squeezes driving share price swings disproportionate even against favorable gold price trends—underscoring elevated trading risk unrelated strictly to operational progress or financial health metrics essential for valuation discipline at this time [S8], [S16], [S19], .

Milestones To Watch

Absent explicit guidance on development staging timelines provided by management within available disclosures:

- Completion and publication of an updated Technical Report including feasibility study outcomes will be paramount.

- Successful demonstration of economically viable sulfide ore treatment technologies could unlock large portions of the mineral resource base into proven reserves needed for financing transition into construction.

- Receipt or renewal of requisite state/federal permits signaling regulatory comfort level will reduce execution risks.

- Market conditions governing precious metals prices will directly influence project economics sufficient to merit restarting operations.

- Capital raising efforts—whether via equity issuance or debt facilities—to fund these next-stage activities will bear watching given historical cash burn rates exceeding operating losses reflecting intensive exploration expenditure mandates.

Final Observations

Hycroft Mining Holding Corp represents a classic case study of a well-capitalized exploration-stage miner possessing considerable measured resources but hamstrung by technological complexity inherent transitioning from oxide heap leach operations towards sulfide milling processes requiring pressure oxidation or similar treatments without finalized engineering studies confirming economic viability.

While having successfully maintained liquidity buffers nearing $182 million provides critical runway flexibility amid uncertain commodity cycles plus regulatory/quasi-litigation risks stemming from outstanding litigation matters relating to warrants management has flagged prominently—the absence so far of any commercial producing mineral reserves caps short-to-medium term valuation uplift potential pending demonstrable technological breakthroughs supported by positive economic studies catalyzing restart decisions.

Investors should therefore expect continuing high volatility driven primarily by trading sentiment rather than fundamental operating transformations at this juncture as management focuses resources on scientific evaluation steps necessary before resuming mine construction schedules that would underpin sustainable cash flow generation long-term.

This analysis synthesizes public filings and market observations relevant inside buy-side frameworks considering early-stage precious metals opportunities such as Hycroft Mining Holding Corporation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments