iSpecimen Inc. Faces Revenue Slump and Regulatory Challenges While Pursuing Cancer Specimen Market Growth

iSpecimen’s digital biospecimen platform confronts steep financial losses, legal hurdles, and compliance costs amid efforts to expand oncology-focused procurement.

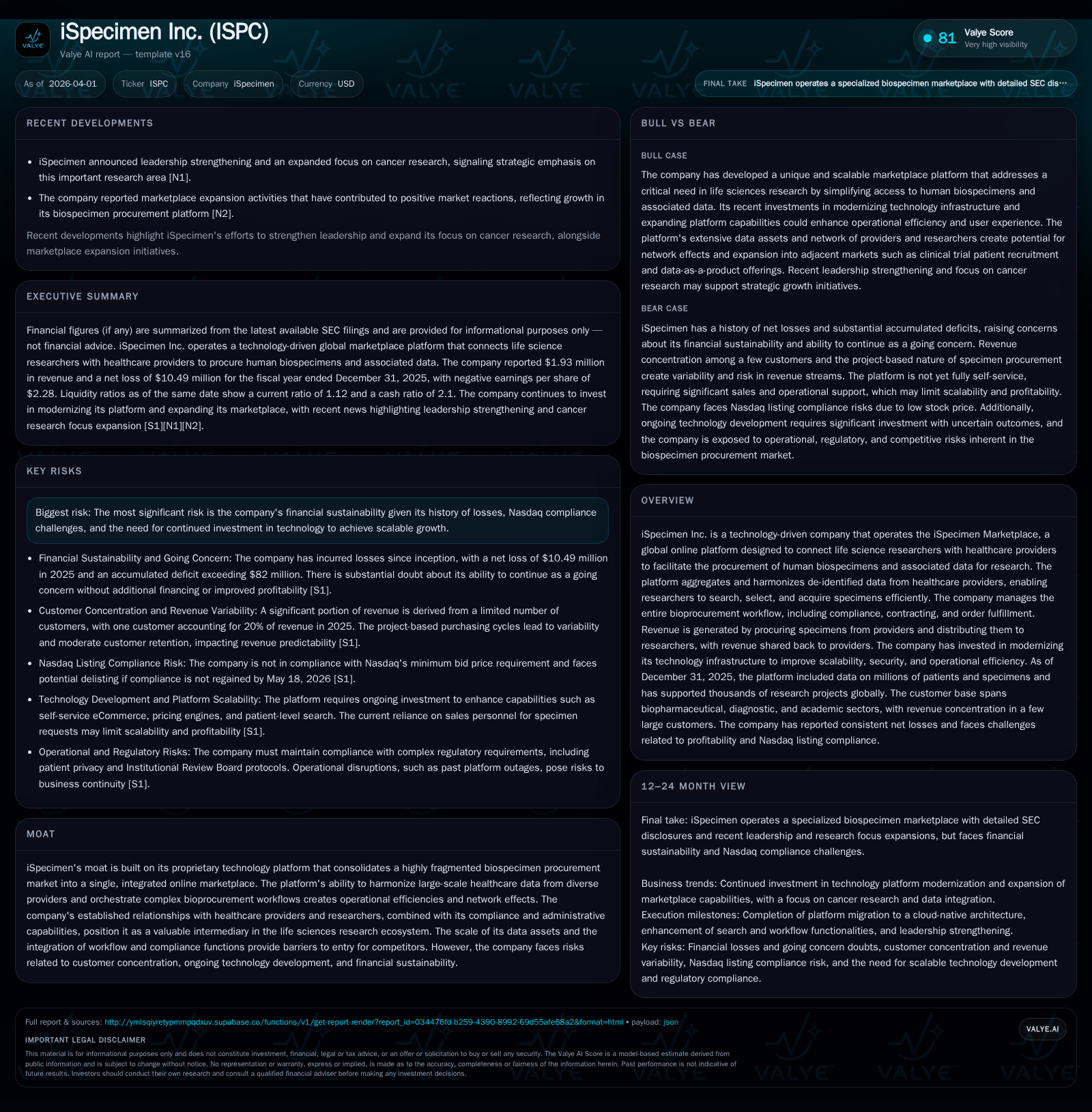

iSpecimen Inc. operates an innovative online marketplace connecting life science researchers with healthcare providers to facilitate biospecimen procurement, addressing a critical bottleneck in medical research. Despite recent leadership initiatives targeting cancer research expansion, the company faces steep revenue declines, ongoing operating losses, and complex regulatory environments that challenge near-term profitability and liquidity. Key risks include customer and supplier concentration, unresolved litigation impacting platform stability, compliance costs, and cash flow constraints.

Historical Financial Performance: Revenue Collapse Amid Continuing Losses

iSpecimen’s financials reveal mounting challenges in scaling its biospecimen marketplace. Revenue fell drastically from $9.29 million in FY2024 to $1.93 million in FY2025—a decline of approximately 79% [F1]. Operating losses narrowed from $12.73 million to $8.98 million over the same period but remain substantial [F1]. Net losses improved modestly from $12.50 million to $10.49 million but still reflect ongoing unprofitability [F1].

Operating cash flow remained negative at $4.24 million in FY2025 though improved relative to the prior year’s outflow of $8.26 million [F1]. Capital expenditures contracted sharply to just $454 in FY2025 from over $31,000 the prior year, indicating constrained reinvestment [F1]. The current ratio stood at approximately 1.12 at year-end 2025, signaling tight short-term liquidity coverage [F1]. Equity declined significantly with accumulated deficits exceeding $82 million as of December 31, 2025 [S1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -10 | -4 | -9 | -79.2% | +16.1% |

| 2024 | 9 | -12 | -8 | -13 | -12.6% | |

| 2023 | -11 | -6 | -11 | -8.3% | ||

| 2022 | -10 | -6 | -10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 52500 | -4 | -339.6 |

| 2024 | 52500 | -8 | -377.5 |

| 2023 | -6 | -113.9 | |

| 2022 | -6 | -50.4 |

Source: SEC companyfacts cache [F1].

The steep top-line contraction contrasts with a stabilization of operating losses likely driven by a combination of reduced sales volume and cost containment efforts.

Proprietary Marketplace Platform: Technology Enabling Market Consolidation

iSpecimen’s competitive edge lies in its proprietary iSpecimen Marketplace platform which addresses the inefficiency of fragmented biospecimen access across global healthcare providers [S11],[S4]. The platform harmonizes de-identified patient and specimen data sourced from electronic medical records, laboratory systems, and biobank inventories into a unified dataset enabling efficient search and procurement akin to consumer travel booking platforms [S11].

Features such as guided searches, cart-based ordering workflows, and online order management improve user experience over traditional manual processes [S11]. The marketplace benefits from network effects as it integrates specimens not only directly procured from healthcare organizations but also from competitor biobanks listing their inventories—a collaborative dynamic enhancing market reach and value for researchers [S4].

Compliance modules embedded within the platform manage complex regulatory requirements including IRB protocols and HIPAA protections while ensuring data provenance—a significant barrier to entry for competitors [S11]. However, full self-service e-commerce remains under development; currently all specimen requests require sales personnel support which may constrain scalability [S7].

Customer Concentration and Revenue Risks

iSpecimen’s customer base comprises biopharmaceutical companies, diagnostics developers, government agencies, and academic institutions totaling roughly 776 customers globally as of end-2025 [S4]. Revenue is heavily concentrated geographically in the Americas (~95% in FY2025), with limited penetration into Europe and Asia Pacific regions [S4].

A key risk factor is high revenue concentration: one customer accounted for about 20% of total revenue in FY2025 after representing nearly 30% in FY2024 [S7]. This exposes iSpecimen’s revenues to volatility linked to individual R&D cycles and project-based purchasing patterns typical within life sciences research [S7]. Specimens are procured "just-in-time" per project rather than via recurring contracts.

Additionally, many clients are privately held emerging biopharma firms without established profitability histories increasing credit risk when iSpecimen procures specimens before customer payments are received [S13]. These factors complicate revenue predictability despite technological advantages.

Strategic Focus on Cancer Research Expansion

Recent leadership appointments have underscored iSpecimen's strategic emphasis on expanding cancer biospecimen procurement—a segment commanding premium pricing due to clinical specificity and critical role in precision medicine development [N1],[N2]. This move aligns with growing demand driven by molecular diagnostics requiring richly annotated cancer specimens for biomarker discovery and companion diagnostic development [N1],[S8].

Since late 2019, iSpecimen has also targeted regenerative medicine applications broadening its addressable market beyond infectious disease or generic tissue banking sectors where competition is more entrenched [S4],[N2]. These initiatives aim to diversify revenue streams and deepen engagement with high-value research domains.

Regulatory Compliance and Legal Challenges

iSpecimen operates under multiple stringent regulatory frameworks governing human subject research including U.S federal laws such as the Common Rule (45 CFR Part 46), HIPAA privacy/security rules (45 CFR Parts 160–164), FDA regulations (21 CFR Parts 50 & 56), as well as international statutes like GDPR affecting European operations [S5],[S6],[S16],[S14]. These impose rigorous compliance obligations around consent management, data anonymization, export-import controls, and biospecimen handling safety.

In FY2025 audits revealed material weaknesses in internal financial controls raising concerns about Sarbanes-Oxley compliance which could affect investor confidence and reporting accuracy [S1]. Unresolved litigation with key IT vendors caused a platform outage lasting approximately six weeks early in 2025 necessitating third-party remediation at additional cost [S17],[S18].

Failure to maintain compliance with export controls administered by U.S Treasury’s Office of Foreign Assets Control and other foreign laws remains an ongoing risk given evolving regulatory landscapes worldwide [S6],[S9],[S14]. Such infractions could lead to fines or reputational damage detrimental to supply partnerships.

Capital Allocation: Cash Flow Management Amid Tight Liquidity

iSpecimen ended FY2025 with cash balances near $6.9 million alongside a current ratio around 1.12 indicating narrow working capital margins [F1],[S12]. Operating cash flow improved relative to prior years but remained negative at $4.24 million while capital expenditures were minimal at under $500 reflecting stringent cost controls or deferred investments [F1].

Equity dropped sharply to about $3 million by end-2025 with return on equity near negative 340%, highlighting difficulty generating shareholder value amid sustained losses [F1]. Share repurchases have been nominal historically; no dividends are paid consistent with growth-stage technology companies prioritizing platform development over shareholder returns thus far [F1],[S12].

Nasdaq listing compliance risks due to low share price add pressure for recapitalization or corporate actions such as reverse stock splits to maintain public market presence [S21]. Future financing will be critical to sustain operations given ongoing cash burn.

Outlook: Growth Opportunities Balanced Against Significant Risks

iSpecimen aims to improve profitability by expanding specimen verticals—particularly oncology—and advancing automation toward fully self-service marketplace capabilities reducing reliance on sales personnel intervention [N1],[N2],[S7]. Such scalability improvements would enhance adoption among researchers expecting digital transaction convenience.

However, these growth prospects face headwinds including persistent revenue concentration risks tied to few large customers’ project cycles; continuous regulatory compliance costs; unresolved litigation distractions; volatile public market conditions; and lack of recurring billing models increasing top-line unpredictability [N2],[S1],[S7].

Investors should closely monitor milestones including:

- Completion of enhanced self-service procurement features,

- Progress in diversifying customer base reducing concentration,

- New contract wins especially within oncology research,

- Resolution of material internal control weaknesses,

- Legal dispute settlements restoring full platform reliability,

- Nasdaq continued listing rule compliance or corporate recapitalization efforts,

- Cash runway balancing burn rate against financing activities [N1],[S3],[S1].

Failure across these dimensions could materially impair operational viability whereas progress would mark critical steps toward sustainable business model transformation.

This analysis synthesizes publicly filed disclosures, recent company news releases, and historical financial data without speculative forecasts or investment recommendations. Readers should consider inherent uncertainties typical for early-stage technology-enabled marketplaces operating within highly regulated life science sectors when evaluating iSpecimen Inc.’s outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments