JATT II Acquisition Corp Stakes $60 Million IPO Proceeds as SPAC Countdown Begins

JATT II Acquisition Corp closes its $60 million IPO, setting the stage for a critical 24-month window to execute a timely business combination with strategic capital securely held in trust.

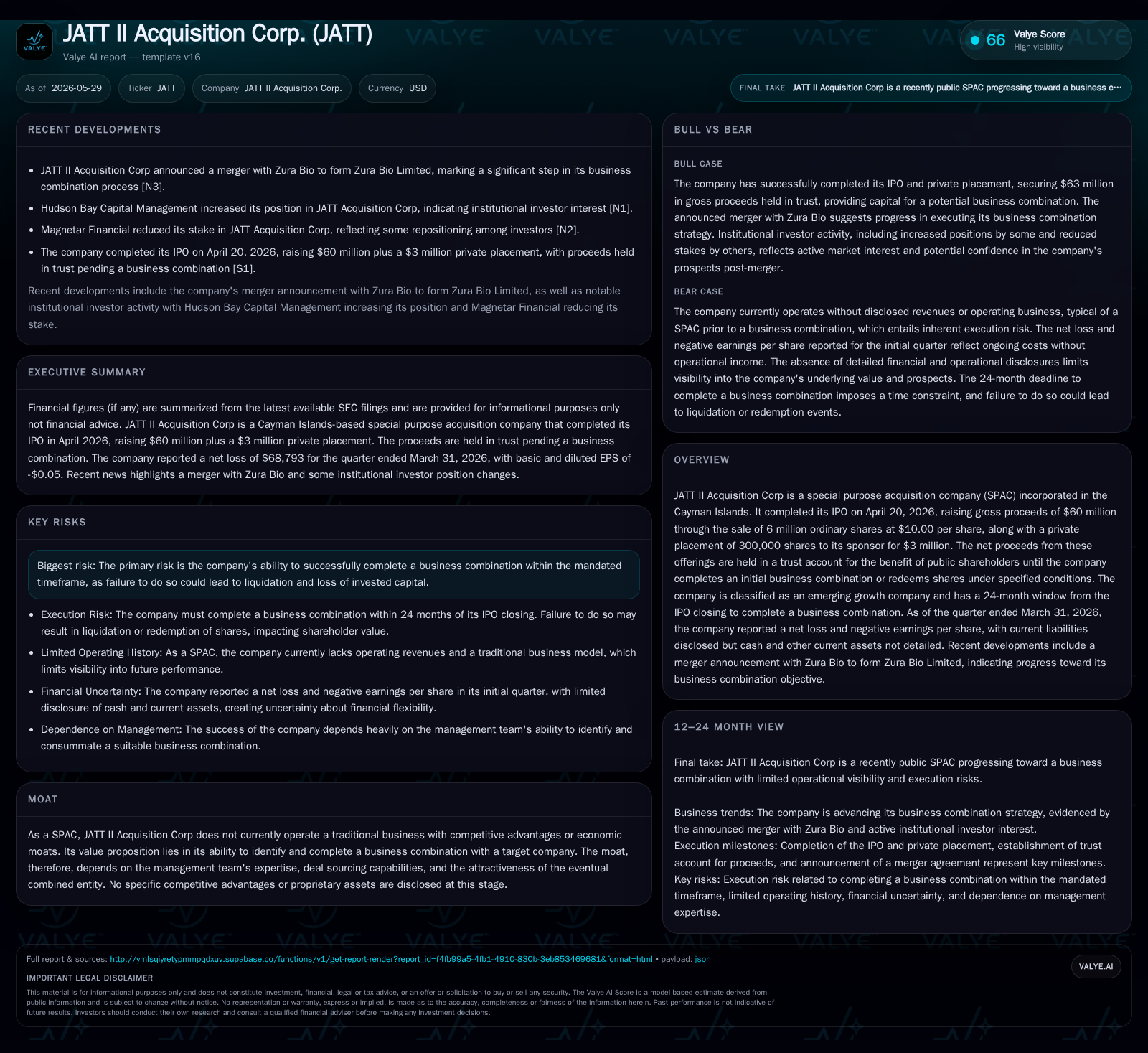

JATT II Acquisition Corp completed its initial public offering on April 20, 2026, raising $60 million plus a $3 million private placement to sponsor affiliates. The proceeds are held in a trust account pending a business combination, which the company must complete within 24 months or face liquidation. The latest quarterly filing confirms operating losses typical for the pre-combination phase and a financial position tightly linked to the trust funds. The company's growth hinges exclusively on management’s ability to identify and close an attractive deal swiftly amid competitive and regulatory pressures inherent to the SPAC market.

Latest Quarterly Development Highlights IPO Capital and Operating Position

JATT II Acquisition Corp finalized its initial public offering (IPO) on April 20, 2026, raising gross proceeds of $60 million from six million ordinary shares priced at $10 each [S3][S4][S7]. Concurrently, the company completed a private placement of 300,000 shares at $10 per share to its sponsor affiliate, JATT Ventures II L.P., generating an additional $3 million [S3][S7]. After underwriting fees and expenses, approximately $60 million was deposited into a U.S.-based trust account managed under an Investment Management Trust Agreement to preserve capital for public shareholders pending an initial business combination [S3][S6].

The quarterly report filed May 29, 2026, covering the period ended March 31, 2026, shows JATT II incurred a net operating loss of approximately $68,800 consistent with typical administrative costs prior to any business combination activity [F1]. Total debt stood near $106,000 and current liabilities were about $205,000 as of quarter-end; these liabilities reflect financing arrangements related to the IPO rather than operational leverage [F1]. The company operates as an emerging growth entity with reporting flexibility but remains compliant with SEC regulations [S3]. Overall, JATT II’s near-term financial posture centers on capital preservation within fiduciary constraints imposed by the trust account framework.

Business Model: SPAC Structure Focused on Timely Business Combination

JATT II Acquisition Corp is structured as a special purpose acquisition company (SPAC) incorporated in the Cayman Islands to raise capital through its IPO for acquiring one or more target businesses within a prescribed 24-month window following IPO closing [S3]. Until consummation of such an initial business combination, JATT II lacks traditional revenue streams or operations and incurs only minimal administrative expenses.

Value generation depends entirely on management's ability to identify suitable acquisition targets and negotiate transactions creating shareholder value while securing required approvals. Funds raised are held in trust earning interest but largely unavailable for operational deployment beyond limited expenses such as taxes or dissolution costs capped at $100,000 if necessary [S7]. Shareholders retain redemption rights if no qualifying acquisition occurs within the timeline or if amendments materially alter redemption terms [S7]. Sponsor private placement shares carry registration rights but are subject to transfer restrictions until after the business combination lock-up period expires [S13]. These features align sponsor incentives closely with successful deal execution rather than conventional operations.

Industry Environment: Competitive SPAC Market Amid Heightened Regulatory Oversight

The SPAC sector remains highly active but increasingly competitive due to market saturation and intensified SEC scrutiny. Numerous SPACs vie for attractive private companies seeking public markets via de-SPAC transactions. This environment pressures JATT II’s management team to source compelling targets rapidly at valuations acceptable to both shareholders and regulators.

SEC oversight emphasizes disclosure adequacy, governance standards including independent board composition (all four directors appointed upon IPO closing are independent), and robust investor protections embedded in corporate charters and redemption mechanisms [S14]. These regulatory requirements necessitate transparent communications and strict adherence to deadlines detailed in JATT II’s amended charter filed concurrently with the IPO close [S10]. Failure to comply may jeopardize transaction feasibility or invite shareholder challenges.

Given JATT II holds no operating assets pre-combination, differentiation depends primarily on sponsor reputation and network strength rather than structural moats or proprietary advantages.

Management Capability: Critical Factor in Deal Sourcing and Value Creation

While specific industry focus or track record details are not disclosed explicitly in filings, JATT II’s potential value realization hinges on its founders’ ability to leverage sector expertise, strategic connections, and negotiation acumen typical of successful SPAC sponsors. The appointment of four independent directors overseeing audit, compensation, and governance committees further supports disciplined deal evaluation and risk mitigation frameworks [S14].

Until an acquisition closes, investment thesis remains aspirational; without proprietary assets or clearly differentiated sourcing channels documented publicly, stakeholders must monitor incremental disclosures over time for pipeline quality signals.

Growth Drivers: Execution of Initial Business Combination Milestones

Growth prospects are transactional rather than organic. Success depends exclusively on milestones linked to executing an initial business combination: identifying promising targets amenable to public listing via merger; negotiating favorable terms aligned with shareholder interests; meeting regulatory filing requirements including merger proxies; securing shareholder approvals; then managing post-merger integration as a combined public entity.

Recent filings confirm absence of revenue or operational diversification prior to transaction closure [S2], underscoring that growth drivers equate mainly to M&A progress rather than traditional sales metrics. Post-combination lockup expirations will also influence share liquidity dynamics impacting price stability.

Risks: Finite Timeline and Execution Challenges

A critical risk is JATT II’s required completion of a business combination within twenty-four months from IPO closing (by April 20, 2028), failing which it must liquidate trust assets returning capital less expenses—effectively resetting shareholder investments without upside participation [S7]. Market conditions unfavorable for deals during this window compound risk.

Dilution risks arise from possible redemptions where public shareholders opt out by redeeming shares for pro-rata trust balances—potentially reducing deal economics if redemption levels are substantial. Pre-deal operational losses accrue from administrative overhead despite budget caps. Liquidity is predominantly restricted within trustee-controlled funds limiting discretionary use until deal closure [F1][S7]. This creates a high-pressure environment requiring balanced speed and diligence amid external factors.

Upcoming Milestones: Progress Toward Value Realization

Key near-term checkpoints include:

- Identification or announcement of prospective business combination targets

- Filing merger-related SEC documents including proxy statements detailing transaction terms

- Scheduling shareholder votes for approval

- Monitoring underwriters’ over-allotment option expiration impacting capital structure

- Ensuring compliance with redemption rights deadlines Investor sentiment reflected in secondary market trading may provide early indicators of deal likelihood.

Each milestone is pivotal in transitioning value from capital custody toward operational enterprise.

Financial Summary: Typical Pre-Combination Profile Reflecting Capital Stewardship

As reported for the quarter ending March 31, 2026 [F1] with supporting balance sheet exhibits dated April 20, 2026 [S3], JATT II operates with minimal cash outflows related to administrative functions absent revenues. Net loss approximated $68,800 primarily reflects legal, accounting, governance expenses preceding any transaction-generated income. Total debt near $106,000 relates mostly to contractual obligations linked to IPO activities rather than leveraged financing structures. Current liabilities around $205,000 represent accrued short-term obligations under normal operating cycles.

Nearly all liquid assets reside in restricted trust accounts holding over $60 million earmarked exclusively for deployment upon successful business combination or refunding scenarios subject to redemption rights provisions [S7]. Thus, while headline cash balances appear robust within trustee control frameworks actual discretionary use is constrained until deal completion.

This financial posture typifies early-stage SPACs prioritizing fiduciary stewardship over active capital deployment pending commercial scale formation post-merger.

This analysis strictly reflects publicly available information without extrapolation beyond documented evidence. No investment advice is offered or implied herein.

Financial position in context

As of 2026-03-31, companyfacts shows $106141 of total debt [F1]. Companyfacts also indicates net debt of roughly $106141 for the latest available period [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments