J.B. Hunt’s First Quarter Momentum: Scalability and Financial Resilience Drive Forward

Latest quarterly results highlight operational stability and liquidity strength underpinning J.B. Hunt’s competitive positioning in transport and logistics.

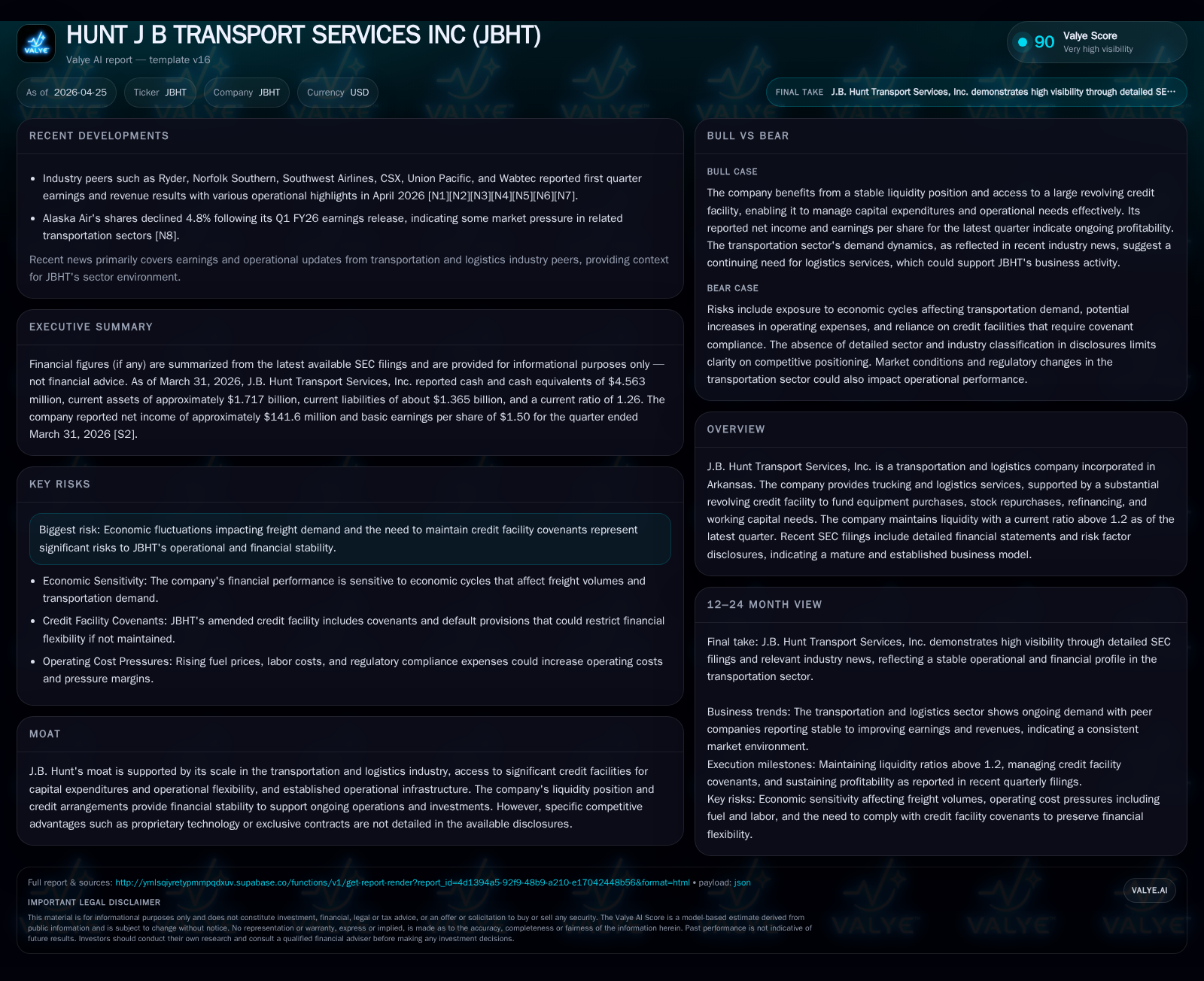

J.B. Hunt Transport Services, Inc. reported solid operational performance in Q1 2026, supported by a healthy current ratio of 1.26 and stable liquidity. The company continues to leverage its scale and credit capacity to maintain fleet efficiency and asset flexibility, navigating industry cyclicality with disciplined capital deployment. While freight demand sensitivity and a lack of proprietary technology present challenges, JBHT remains well-positioned amidst evolving sector dynamics. Key upcoming milestones include executing on growth initiatives and monitoring demand trends amid competitive pressures.

Q1 2026 Operating Highlights and Changes

J.B. Hunt Transport Services’ latest quarterly filing (10-Q dated April 24, 2026 [S2]) reflects a continuation of stable operational performance into early 2026. Management’s Discussion and Analysis signals steady revenue streams aligned with historical patterns without notable anomalies or significant shifts in segmental contribution. The company reported a current ratio of approximately 1.26 as of March 31, 2026 ([F1]), indicating ample short-term liquidity to cover operational needs.

Concurrently, the April 23 shareholder meeting (filing 8-K [S3]) confirmed the election of directors per standard corporate governance practices with no material proxy battles or structural upheavals noted. This event underscores management continuity and investor confidence ahead.

Operationally, the quarterly commentary reinforces the company's measured approach to capital deployment amid a mixed macro freight environment, maintaining fleet utilization amidst sector-wide pressures. No revisions were made to full-year guidance explicitly in the filing.

Core Business Model and Service Offering Analysis

Per the latest annual report (10-K dated February 24, 2026 [S1]), J.B. Hunt operates predominantly across two synergistic segments: asset-heavy trucking services complemented by asset-light logistics solutions including intermodal transport coordination and dedicated contract carriage.

Revenue derives primarily through freight hauling fees negotiated via contractual agreements or spot-market contracts across diverse industries with concentration in consumer goods, retail, manufacturing, and e-commerce sectors. The company's extensive capital base supports a sizeable owned fleet while supplementing capacity through third-party carriers when advantageous.

A substantial revolving credit facility facilitates equipment acquisitions, working capital requirements, stock repurchases, and refinancing activities (Valye report excerpt). Strategic management of fleet renewal cycles alongside technology-enabled route optimization enhances cost control and margin preservation.

Importantly, the dual model mitigates asset utilization risk inherent in trucking alone by leveraging logistics services that generate higher margin but lower capital intensity revenues.

Competitive Environment and Industry Structural Overview

Within the broader transportation/logistics industry landscape ([S1], news industry comparisons [N12][N13]), J.B. Hunt competes alongside peers such as Ryder System Inc. and FedEx in adjacent parcel logistics. Although industry consolidation has intensified scale-driven competitive advantages, commoditized pricing pressure persists due to fragmented customer bases and availability of alternative carriers.

Pricing power is tempered by customer bargaining sophistication with moderately elastic demand influenced by economic cycles. Fuel cost volatility remains a salient input risk affecting operating margins absent significant fuel surcharges or hedging strategies disclosed.

Switching costs for customers are moderate; long-term contracts can provide stability but spot-market exposure introduces variability. JBHT’s competitive moat largely rests on scale economies—optimizing route density, minimizing deadhead miles—and capital access enabling rapid equipment replacement or fleet expansion relative to smaller competitors.

Regulatory headwinds including environmental mandates increase compliance complexity but have not fundamentally shifted competitive hierarchy to date. The lack of exclusive proprietary technology platforms limits differentiation versus some tech-forward integrators.

Growth Opportunities Powered by Scale and Capital Access

Growth vectors for J.B. Hunt revolve around increasing freight volumes fueled by sustained e-commerce penetration and evolving supply chain demands captured via flexible dedicated contract carriage solutions ([S2],[S1]).

Ongoing investment in routing technologies promises incremental margin improvement through better load planning and reduced fuel consumption relative to traditional dispatch methods.

The company’s revolving credit line provides valuable financial agility for fleet upgrades—crucial given the industry's capital-intensive nature wherein aging vehicles impact maintenance costs and service reliability.

Capital expenditure guidance in FY2025 trended modestly lower year-over-year ([F1]), reflecting efficiency gains rather than retrenchment and supporting a positive free cash flow outlook when coupled with solid operating cash flow generation.

Moreover, strategic partnerships across intermodal networks enhance multimodal service offerings extending reach without proportional capital needs.

Challenges and Risks Moderating Growth Prospects

The company openly acknowledges key risks including economic cyclicality which directly impacts freight demand sensitivity ([S1],[S2]). As industrial production slows or retail inventories adjust downward, spot-market rates decline dampening revenue growth potential.

Fuel price spikes compress margins particularly when contractual fuel pass-through mechanisms lag market movements or are absent.

Leverage metrics remain a consideration—a net debt position near $973 million based on most recent available data ([F1]) necessitates ongoing covenant vigilance to avoid restrictions on financial flexibility.

Operational risks span driver availability constraints common across trucking markets influencing capacity utilization rates plus potential supply chain bottlenecks affecting equipment procurement timing.

While scale creates resilience to commodity swings, JBHT’s moat is somewhat limited by absence of strong proprietary IT systems or exclusive long-term contracts highlighted—an area where peers have increasingly differentiated offerings via platform digitization initiatives [N12].

Key Upcoming Milestones and What To Monitor

Investors should track execution against Q2 shipment volume targets to validate continuing momentum post-earnings release ([S2],[S3]). Monitoring operating cost ratios alongside fuel expense trends will be instructive on margin trajectory given volatile input costs.

Progression on technology adoption—particularly improvements in telematics integration or AI-augmented route planning—will be key value drivers if realized at scale.

Further shareholder engagement metrics following annual meeting votes may reveal subtle shifts in governance priorities or board dynamics but none were apparent recently ([S3]).

Additionally, contract renewals within dedicated carriage segments will serve as barometers for customer retention strength amid pricing environment shifts.

Consolidated Financial Profile and Liquidity Insights

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 598 | 1678 | 865 | 731 | +4.8% |

| 2024 | 571 | 1483 | 831 | 865 | -21.6% |

| 2023 | 728 | 1745 | 993 | 1862 | -24.9% |

| 2022 | 969 | 1777 | 1332 | 1541 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 171 | 923 | 948 |

| 2024 | 176 | 514 | 618 |

| 2023 | 174 | 160 | -118 |

| 2022 | 167 | 300 | 236 |

Source: SEC companyfacts cache [F1].

J.B. Hunt maintains sound financial health supported by solid liquidity as evidenced by $4.56 million in cash & equivalents against current liabilities approximating $1.37 billion resulting in a current ratio of approximately 1.26 ([F1]). Current assets totaled roughly $1.72 billion at quarter-end providing buffer for short-term obligations.

Annual revenue stood near $2 billion historically ([F1]) with operating income trending around $865 million most recently showing slight year-over-year increases (4.1% operating income growth FY2025 over FY2024). Net income similarly grew modestly (+4.8%).

Operating cash flow remains robust ($1.68 billion FY2025) comfortably covering capital expenditures ($730 million FY2025), indicating positive free cash flow (~$948 million) which sustains dividend payments ($171 million FY2025) alongside substantial share repurchases ($923 million FY2025).

Leverage measured conservatively within an investment-grade profile although net debt levels necessitate monitoring given inherent cyclical freight volatility risks.

Overall financial discipline aligns with strategic execution priorities underscoring JBHT's balanced approach between growth investment and shareholder return commitment.

Disclaimer: This analysis is prepared solely for informational purposes reflecting publicly available data from SEC filings [S1,S2,S3], companyfacts snapshot [F1], and industry news sources [N12,N13]. It does not constitute financial advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments