Kingsoft Cloud Grows Enterprise Revenue 28% in 2025 Despite Operating Losses and Cost Challenges

Kingsoft Cloud’s fiscal 2025 results show strong enterprise service growth and improved cash flow amid regulatory risks and rising infrastructure expenses.

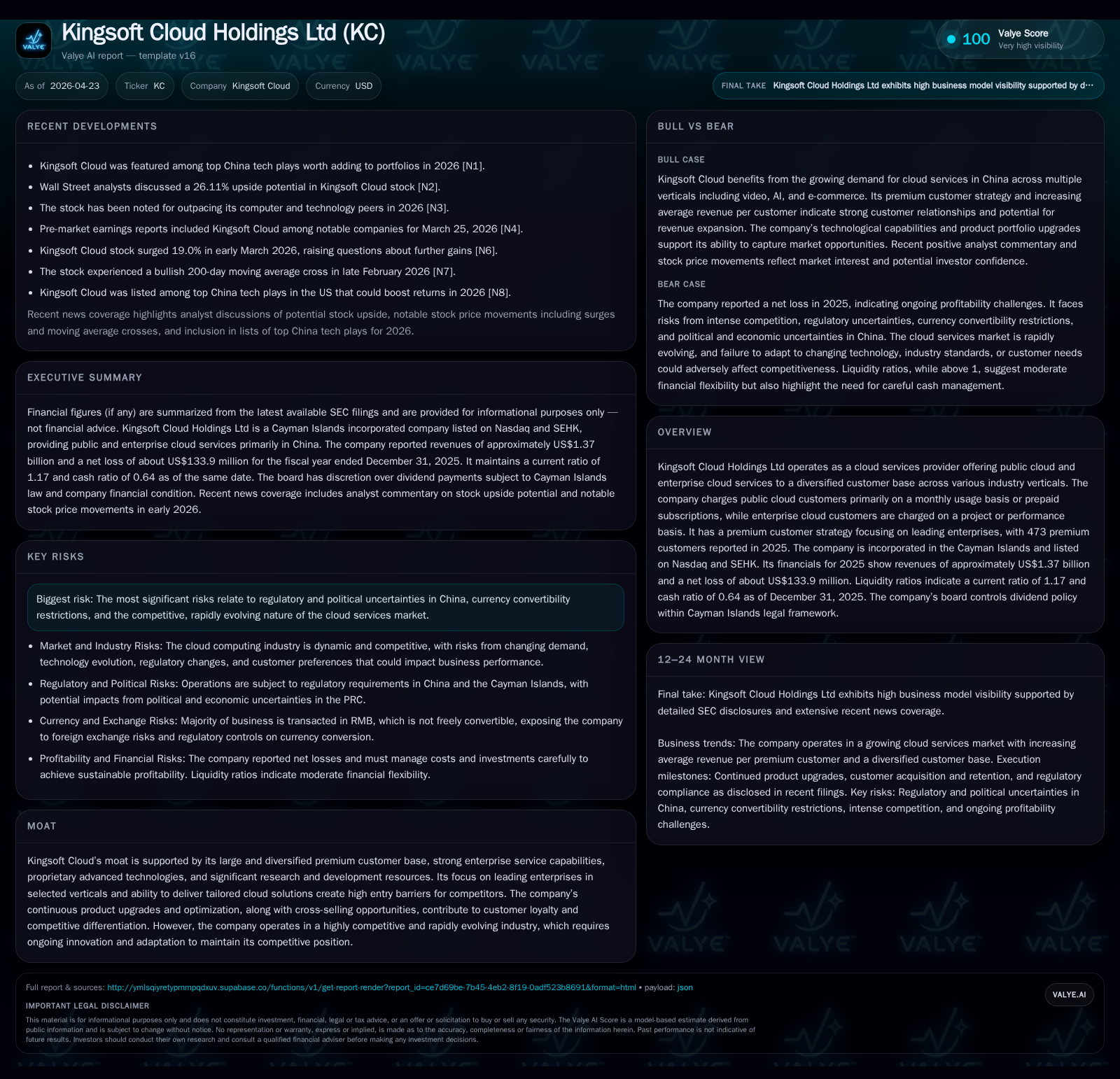

Kingsoft Cloud Holdings Ltd reported a 28% revenue increase in fiscal 2025, fueled primarily by expansion in its enterprise cloud customer base. However, the company continues to face operating losses despite improving cash flows. Its business model centers on catering to premium clients with tailored cloud solutions across diverse verticals, leveraging proprietary technologies and steady R&D investment. The Chinese cloud market’s rapid growth is a key driver, but regulatory uncertainties and intensifying competition remain challenges. Upcoming milestones include sustaining enterprise service expansions and managing infrastructure investments efficiently.

Recent Operating Update

Kingsoft Cloud’s latest update anchored in the April 23, 2026 Form 6-K filings reaffirms continued growth momentum into fiscal year 2025. The company disclosed it filed its annual report along with an Environmental, Social, and Governance (ESG) report highlighting operational transparency [S2]. Earlier April filings noted internal leadership transitions pertinent to company secretarial functions but did not impact operational disclosures [S3]. These filings solidify the current financial position and strategy described in the comprehensive 20-F annual report also filed on April 23 [S1].

Fiscal year 2025 revenues hit approximately US$1.37 billion, a sizeable increase from about US$1.07 billion in 2024—reflecting a robust year-on-year rise of roughly 28% [F1]. Despite this topline growth, KC reported a net loss narrowing to approximately $134 million from prior wider losses [F1]. Crucially, operating cash flow surged more than fivefold compared to the previous year, reaching over $543 million [F1]. The cash conversion strength stems from improved working capital management alongside strong revenue growth.

Business Model Analysis

Kingsoft Cloud operates primarily as a provider of cloud infrastructure services segmented between public cloud offerings and more specialized enterprise cloud solutions. Public cloud customers generally pay monthly based on resource usage or prepay for fixed subscription periods. Meanwhile, enterprise customers—often large or regulated organizations—engage in contracts priced project-wise or on performance metrics [S14].

The business emphasizes a "premium customer" strategy targeting leading enterprises across multiple verticals such as healthcare, finance, public services, e-commerce, intelligent mobility, and AI applications. This focus is evidenced by the concentrated revenue contribution wherein approximately 98% derives from premium customers [S9]. Although the total number of these customers declined slightly from 492 in 2024 to 473 at the end of 2025, average revenues per client notably increased—especially among public cloud users where average revenue jumped from RMB19.7 million to RMB30.3 million [S17].

Quality tailored offerings form Kingsoft Cloud’s strategic backbone. It differentiates itself with proprietary advanced technologies developed internally through significant R&D expenditure (over RMB810 million or ~$116 million in FY25), continual product upgrades, and high-touch client servicing capabilities rooted in longstanding relationships with affiliates like Kingsoft Group and Xiaomi [S10][S24]. The ecosystem adjacency provides unique insights into customer needs enhancing solution relevance.

Operational costs have grown as investments scale; overall operating expenses remain high due to both selling/marketing demands ($79 million) and general/admin expenses ($131 million), despite absence of asset impairments seen prior years [S4]. These elevated costs reflect deliberate capacity-building efforts essential for sustaining competitive advantage in China’s fast-evolving cloud market.

Industry Structure & Competitive Position

China’s cloud sector is characterized by several dominant players competing on technological innovation breadth, solution depth tailored for vertical industries, infrastructure scale (data centers, network coverage), security compliance rigor, and pricing flexibility. Kingsoft Cloud ranks among notable domestic competitors but contends against well-capitalized giants like Alibaba Cloud and Tencent Cloud.

KC’s moat is derived from its large diversified enterprise client base delivering recurring high-value contracts plus its ongoing investments in proprietary tech that deliver customized industry-specific solutions—creating high switching costs for customers [S10][S17]. This vertical specialization coupled with moderate scale allows it to carve market niches beyond one-size-fits-all public cloud commoditized services.

Nonetheless, competitive pressure remains intense especially with rapid advancements in AI-enabled cloud capabilities requiring continuous R&D spend. Also structural barriers such as government policy shifts regarding data localization or foreign investment regulation impose complexity unique to the Chinese market context [S1].

Growth Drivers & Constraints

Drivers:

- Accelerating digitalization across traditional industries favors adoption of KC’s enterprise cloud services which grew faster than public offerings.

- Government initiatives supporting new technology adoption drive demand for compliant data infrastructure.

- Rising integration of AI tools requires sophisticated scalable compute resources offered through Kingsoft Cloud platforms.

- Expanding ecosystems involving Kingsoft Group and Xiaomi generate cross-selling opportunities driving deeper wallet share among premium clients.

- Increasing average revenues per client indicate success at upselling higher-tier solutions.

Constraints:

- Regulatory uncertainty around variable interest entity arrangements applicable to many Chinese tech firms could disrupt operations or impose compliance costs.

- Currency convertibility restrictions may limit efficient offshore capital flow affecting liquidity deployment.

- Growing competition pressures pricing power; some customers adopting multi-cloud strategies reduce single provider reliance impacting usage levels.

- Infrastructure scaling requires sizable capital outlays although this capex has shown declines recently ($38.7M vs higher prior years) signaling possibly better efficiency or pausing expansion [F1][S20].

What To Watch Next

Key upcoming indicators will include:

- Trends in new premium customer additions or retention rates signaling success in market penetration amid evolving industry needs.

- Changes in operating margins as infrastructure leverage improves or cost management programs take effect.

- Regulatory developments related to corporate structure approvals or foreign investment impacts potentially influencing operational flexibility.

- Continued enhancement of product portfolio breadth especially AI-related offerings aligning with China’s large-scale technology push.

- Execution on network upgrades detailed as ongoing capital projects underpinning scalability [S1][S20].

- Liquidity management given working capital dynamics especially vis-à-vis payment cycles from large enterprise clients.

Financial Profile Summary

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1367 | -134 | 544 | -111 | +28.2% | +50.3% |

| 2024 | 1067 | -269 | 86 | -238 | +7.5% | +12.1% |

| 2023 | 993 | -307 | -24 | -297 | -16.3% | +20.5% |

| 2022 | 1186 | -385 | 27 | -326 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 505 | -10.0 | |

| 2024 | 0 | 38 | -38.1 |

| 2023 | -88 | -31.6 | |

| 2022 | 30 | 10 | -30.2 |

Source: SEC companyfacts cache [F1].

While profitability remains negative (approximate -10% ROE), the trend indicates narrowing losses concurrent with significant improvements in cash flows driven by operational efficiencies and top-line growth [F1]. Capital investment has moderated which may help support margin improvements going forward if sales maintain strength without proportional cost increases.

Conclusion

Kingsoft Cloud stands as a compelling player balancing rapid growth opportunities in China’s burgeoning cloud market against structural challenges typical of an emerging tech leader transitioning toward profitability. Its differentiated focus on premium enterprise solutions backed by sustained R&D investment builds meaningful competitive moats that should support long-term viability provided regulatory uncertainties are managed carefully.

Investors should monitor evolving dynamics around customer acquisition efficacy, cost control execution particularly related to infrastructure investments' scalability benefits, and policy developments impacting contractual arrangements critical for operating in China’s IT sector.

This analysis summarizes information extracted solely from publicly filed SEC documents dated through April 2026 combined with partial Nasdaq news references for contextual framing.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments