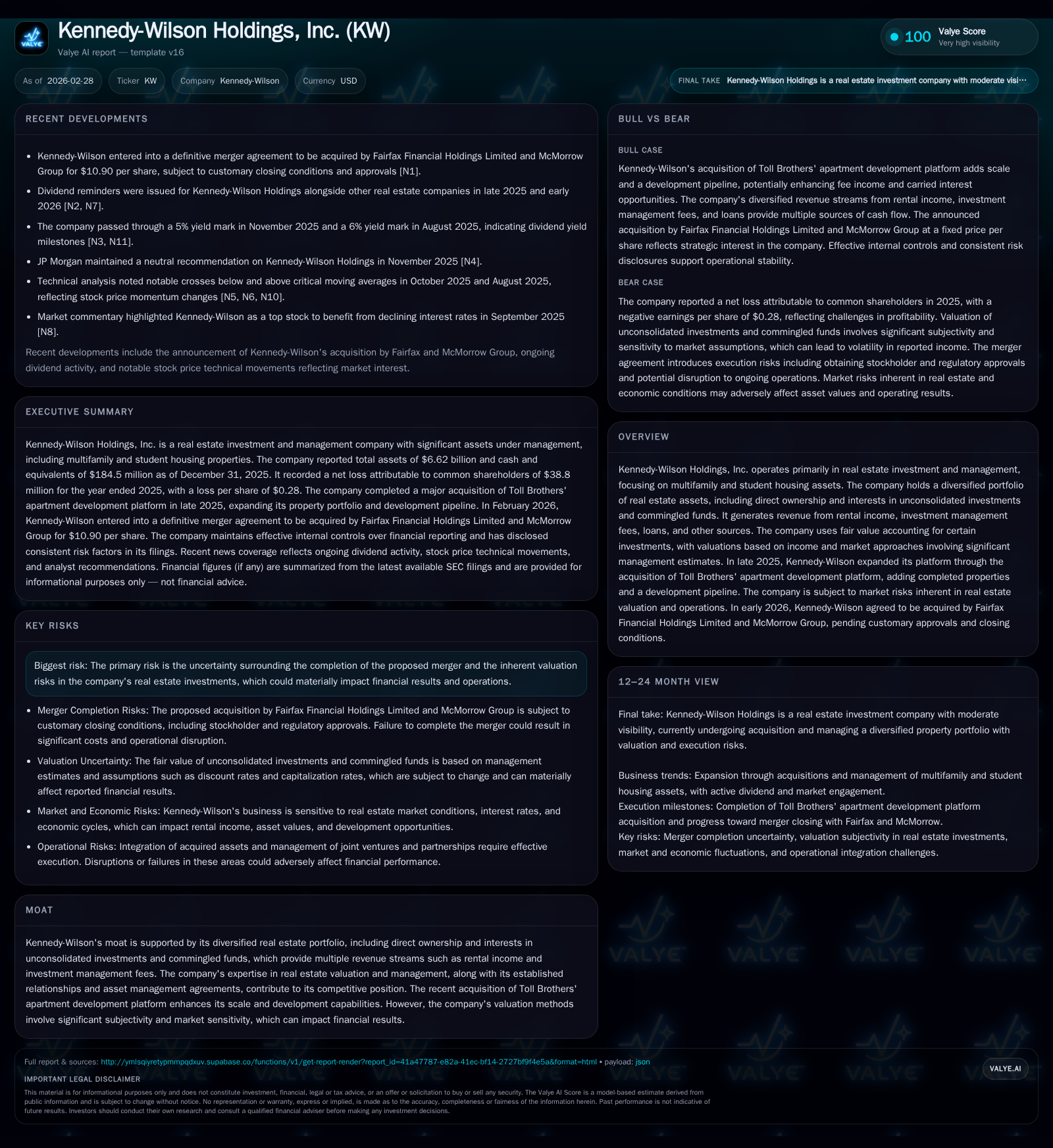

Kennedy-Wilson Holdings' Expansion and Acquisition Strategy Meet Market Risks and Pending Fairfax Takeover

Kennedy-Wilson broadens its multifamily footprint through Toll Brothers acquisition while facing valuation complexities and a pending buyout by Fairfax Financial.

Kennedy-Wilson Holdings, a real estate investment and management firm with $36.4 billion AUM, has historically grown by focusing on rental housing, student housing, and real estate loans primarily in the U.S. and Europe. In late 2025, it notably expanded its development pipeline by acquiring Toll Brothers' apartment platform. Despite robust investment management fee growth and a sizable multifamily portfolio, the company's 2025 operating income declined sharply from prior years, partially reflecting market uncertainties and accounting for fair value fluctuations. The firm faces risks related to the finalization of its acquisition by Fairfax Financial in early 2026. Capital returns have been moderated lately with modest buybacks and constrained free cash flow after capex.

Company Background and Business Model

Kennedy-Wilson Holdings, Inc. operates as an integrated real estate investment company paired with an asset management platform managing approximately $36.4 billion in assets under management as of December 31, 2025 [S1]. Its primary focus is rental housing—including market-rate and affordable multifamily units—and student housing across the United States, United Kingdom, and Ireland. The portfolio includes direct ownership interests alongside unconsolidated investments and commingled funds.

In addition to property investments, Kennedy-Wilson maintains a substantial real estate credit business focused on originating and servicing senior construction loans secured mainly by multifamily and student housing properties developed by institutional sponsors [S1]. This combination generates diversified revenue streams from rental income, asset management fees, loan interest income, development fees, carried interests, and property dispositions.

Historical Performance Drivers

The company's growth has been driven by expanding its rental housing footprint through acquisitions and repositioning assets to improve operating cash flows post-acquisition. Strategic origination of real estate loans has also contributed attractive risk-adjusted returns [S1]. The investment management platform has grown via co-investment arrangements that generate asset management fees and carried interest.

At year-end 2025, Kennedy-Wilson's portfolio included roughly 31,257 market-rate multifamily units, 13,195 affordable units, and nearly 2,000 single-family units either owned or financed by the company [S1]. This reflects a deliberate tilt toward residential rental sectors that typically exhibit less cyclicality than commercial office or retail segments.

A historical snapshot based on available financial data reveals variability influenced by fair value fluctuations:

Historical performance (annual)

| FY | CFO ($mm) | Capex ($mm) |

|---|---|---|

| 2025 | 11 | 3 |

| 2024 | 55 | 3 |

| 2023 | 49 | 6 |

| 2022 | 33 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 9 | 9 |

| 2024 | 15 | 53 |

| 2023 | 21 | 43 |

| 2022 | 31 | 29 |

Source: SEC companyfacts cache [F1].

Net income has shown volatility with spikes such as in FY2017 attributable to non-recurring valuation gains or tax effects typical in complex real estate accounting involving fair value adjustments [F1]. Operating income experienced a steep decline during this period indicating cyclical pressures or increased expenses.

This volatility partly arises from fair value accounting methodologies where assumptions about future rents, capitalization rates, and occupancy forecasts affect valuations significantly [S1]. The loan portfolio also carries floating rate exposure that is hedged primarily through interest rate caps.

Strategic Expansion via Toll Brothers Acquisition

In late 2025 Kennedy-Wilson expanded its rental housing development capabilities through the acquisition of Toll Brothers’ Apartment Living platform for approximately $379 million [S8][S16]. This transaction included:

- Ownership interests in four completed multifamily/student housing properties totaling over 5,000 units.

- A sizable future development pipeline comprising land acquisitions under contract expected to yield more than two dozen projects across key U.S. markets.

- Integration of key Toll employees including executive leadership into Kennedy-Wilson’s operations for ongoing asset management.

The acquisition is expected to close fully through early 2026 with equity partner capital combined with construction loans supporting ongoing development projects [S16]. This aligns with Kennedy-Wilson’s strategy emphasizing local market expertise combined with institutional capital to pursue off-market deals yielding strong long-term cash flows [S1].

The deal also includes asset management agreements generating fees from assets retained by Toll or third parties [S8].

Market Risks and Fair Value Accounting Impact

The use of income capitalization approaches for asset valuation introduces earnings volatility due to sensitivity around rent levels and cap rates affecting reported profits under fair value accounting applied to consolidated assets and unconsolidated investments [S1].

Interest rate risk remains significant given approximately 22% of debt is variable rate—with some portion uncapped—exposing the company to rising borrowing costs; however, about 78% is fixed rate reducing long-term cost variability [S1]. Interest rate caps expiring within roughly one year provide near-term protection against rate increases [S1].

Currency risk is concentrated in European operations representing around 13% of the portfolio but is monitored given exchange rate fluctuations [S1].

Operational risks include uncertainties related to integrating newly acquired platforms like Toll Brothers’ division amid macroeconomic factors affecting leasing activity and construction costs [S4][N1].

Pending Acquisition by Fairfax Financial

On February 17, 2026 Kennedy-Wilson entered into an agreement to be acquired by Fairfax Financial Holdings Limited alongside McMorrow Group at $10.90 per share in cash consideration—a premium relative to recent trading prices—subject to customary shareholder approvals and regulatory clearances [N1][S3][S6][S9].

Upon closing shareholders will no longer hold equity stakes but will receive merger consideration proceeds except for certain rollover shares held by insiders receiving equity units in the parent entity under different terms [S11][S23].

This ownership change could influence dividend policies and capital deployment priorities post-acquisition.

Capital Allocation Insights

Free cash flow generation after capital expenditures was modest at approximately $8.5 million for FY25 compared to substantially larger operating cash flows in prior years reflecting reinvestment emphasis over broad shareholder return programs [F1].

Dividend payments were meaningful during the mid-2010s but no recent amounts are explicitly disclosed post-2018; however modest share repurchases totaling about $9.2 million during FY25 indicate restrained capital return activity relative to prior years when buybacks were significantly higher [$20+ million annually pre-2024] [F1][S9][S19].

Equity declined seasonally from about $1.76 billion at end-2023 to roughly $1.54 billion at end-2025 reflecting distributions plus acquisitions offset by earnings impacted by valuation adjustments affecting comprehensive income [F1]. Return on equity approximates moderate single digits (~6.5%) based on latest net income relative to equity base but fluctuates due mainly to mark-to-market effects rather than purely operational results.

Outlook Considerations

Potential growth drivers include:

- Acceleration of development revenue streams from Toll Brothers platform integration including asset management fees and potential carried interest upside.

- Expansion of the loan portfolio focused on senior construction loans securing high-quality multifamily projects offering attractive yields amid rising rates.

- Possible operational synergies or capital support under Fairfax ownership following transaction close.

Challenges remain:

- Execution risks around merger closing timing along with associated transaction costs impacting near-term financials.

- Sensitivity to rising variable interest rates despite hedging could pressure margins if rates exceed cap levels or refinancing options become constrained.

- Real estate market dynamics influenced by inflationary pressures may moderate property appreciation affecting fair value gains.

- Complexity scaling large multi-jurisdictional development pipelines amid supply chain constraints.

Upcoming quarterly disclosures will be important for tracking rental income trends, loan portfolio performance, integration progress related to Toll Brothers acquisition, as well as updates on merger completion timing.

Conclusion

Kennedy-Wilson combines direct property ownership with diversified debt investments across geographies alongside an established asset-management platform generating recurring fee income supported by longstanding industry relationships. Its recent strategic expansion through acquiring Toll Brothers’ apartment development arm adds scale but also complexity amid economic uncertainty. The pending Fairfax acquisition presents ownership transition risks balanced against a premium offer while potentially positioning the company for longer-term stability under new control. Capital allocation points toward prudent reinvestment balanced against modest buybacks amid manageable leverage supported by mixed fixed/floating rate debt with partial hedging. Monitoring integration execution alongside valuation consistency under fair value accounting will be critical for assessing sustainable profitability as ownership changes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments