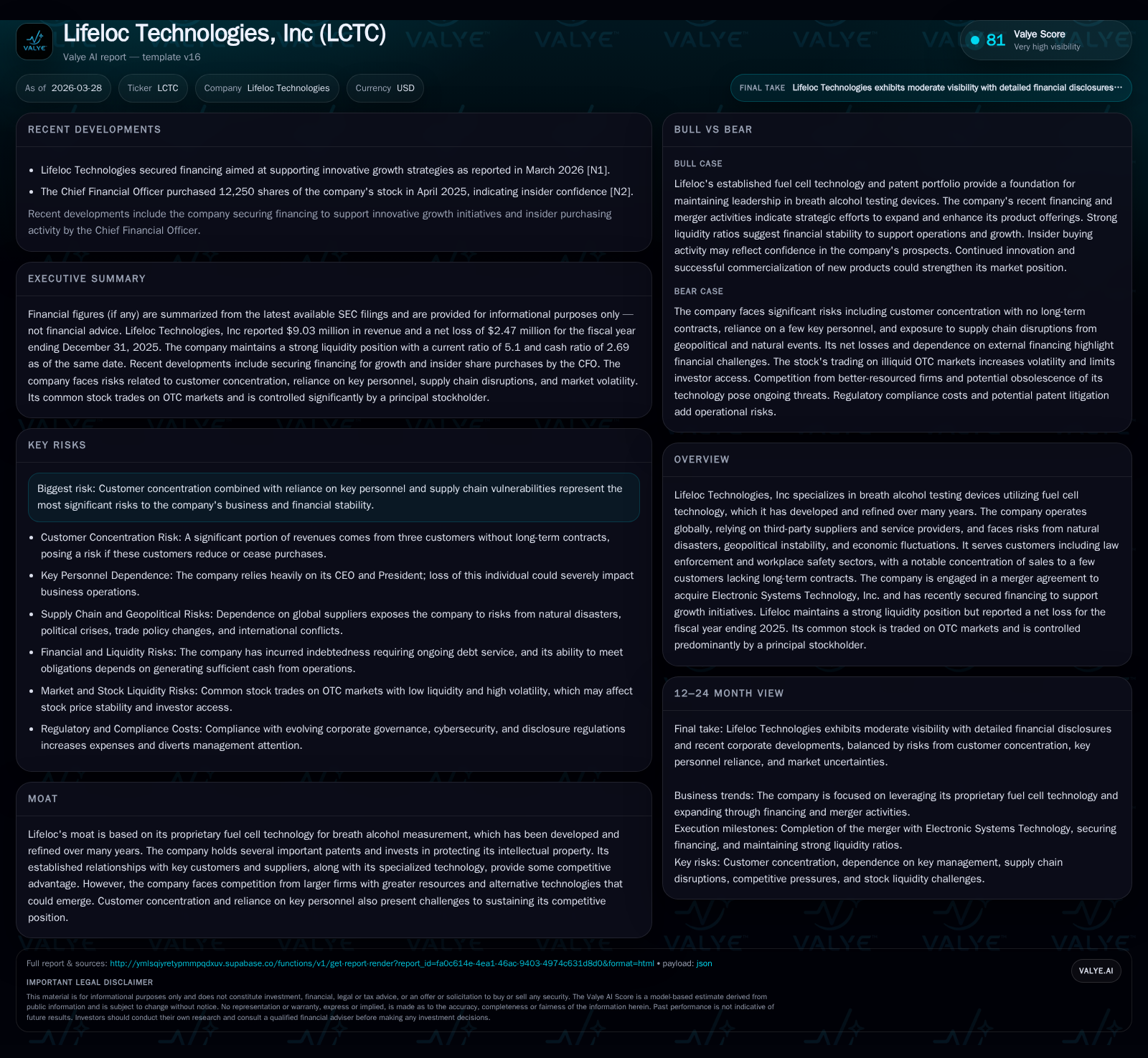

Lifeloc Technologies: Balancing Innovation and Financial Challenges Amid Growth Initiatives

Lifeloc’s patented fuel cell breath alcohol technology supports its market niche despite persistent losses and external risks, with recent financing fueling growth ambitions.

Lifeloc Technologies, Inc continues to lead in breath alcohol testing devices based on proprietary fuel cell sensors, backed by DOT regulatory approvals. From 2022 to 2025, the company experienced modest revenue growth alongside widening operating losses and negative net income, reflecting structural cost pressures and customer concentration risks. Recent merger plans with Electronic Systems Technology Inc. and new financing secured in early 2026 aim to enhance product development and expand market reach. While liquidity remains strong with a current ratio above 5x, ongoing negative free cash flow and geopolitical supply chain vulnerabilities challenge operational stability. Monitoring patent protection efforts, regulatory compliance, and customer diversification will be key for future performance.

Historical Financial Performance

Lifeloc Technologies’ financial results from FY2022 through FY2025 illustrate modest revenue growth accompanied by increasing operating losses. Revenue rose from $8.48 million in 2022 to $9.03 million in 2025, reflecting a compound annual growth rate of approximately 0.7%, though with notable year-to-year variability including a peak at $9.33 million in 2023 [F1]. Despite this top-line trend, operating income declined further into negative territory, moving from a loss of $650 thousand in 2022 to $1.23 million in 2025, evidencing mounting cost pressures.

Net income followed an uneven path: after a loss of $456 thousand in 2022, the company achieved a positive net income of $206 thousand in 2023 before returning to a significant loss of $2.47 million in 2025 [F1]. This volatility suggests episodic factors but primarily points to ongoing margin challenges.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | -2 | -499319 | -1230020 | +5.7% | -134.6% |

| 2024 | 9 | -1 | -1327691 | -1408217 | -8.5% | -612.1% |

| 2023 | 9 | 0 | -525740 | -191135 | +10.0% | +145.1% |

| 2022 | 8 | 0 | 54325 | -650345 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -962112 | -60.2 |

| 2024 | -1867422 | -16.9 |

| 2023 | -532551 | 3.2 |

| 2022 | -158881 | -7.4 |

Source: SEC companyfacts cache [F1].

*Smaller increase in operating losses year-over-year; **Net income deterioration reflecting increased losses.

Customer Concentration and Supply Chain Risks

The company’s revenue base exhibits notable customer concentration: three customers accounted for around 18% of product sales in fiscal year 2025 without binding long-term purchase contracts [S10]. The largest single customer represented nearly half of accounts receivable at year-end. This concentration increases exposure to fluctuations in purchasing behavior.

Supply chain dependencies center on specialized fuel cell components sourced from limited suppliers [S14]. Geopolitical tensions—including conflicts impacting trade routes and tariffs—and natural disasters present risks to procurement continuity and cost stability [S1], [S15]. These factors could disrupt manufacturing schedules or raise input costs amid competitive pricing pressures.

Technological Edge Supported by Patents

Lifeloc’s core competitive advantage lies in its proprietary fuel cell sensor technology used for breath alcohol detection devices compliant with Department of Transportation standards [S4], [S21]. Its products such as the FC10 series are listed on the DOT's Conforming Products List (CPL), validating their evidential use.

Patent protections underpin this technological moat but require active enforcement to prevent infringement risks that could divert resources or limit usage rights [S6]. Continued innovation and regulatory approvals remain vital as competitors explore alternative sensing technologies.

Regulatory Environment

Operations are subject to rigorous federal oversight primarily via the DOT Office of Drug & Alcohol Policy & Compliance. Certification processes ensure devices meet evidentiary standards required for law enforcement applications [S21]. Compliance with evolving biometric data privacy laws and cybersecurity regulations also demands ongoing investment [S4], [S29].

State-level variations in DUI laws add complexity to market acceptance across jurisdictions.

Growth Outlook: Merger and Financing

A recently announced merger agreement with Electronic Systems Technology Inc., supported by new financing secured in March 2026 aims to bolster Lifeloc’s product portfolio and market reach while providing capital for expanded R&D and manufacturing capacity enhancements [N1], [S3].

While promising potential scale benefits and innovation acceleration, integration execution risks remain.

Capital Allocation and Liquidity Position

Despite recurring net losses and negative free cash flow (approximately -$962K in FY2025 calculated as operating cash flow minus capital expenditures), Lifeloc maintains strong liquidity with a current ratio exceeding five times as of year-end 2025 [F1], [S11].

The company carries subordinated debt totaling $825K at an interest rate above 8%, with balloon payments due in later years adding financial obligations requiring sustained cash generation capability [S11], [S28].

No dividends or share repurchases have been declared; capital allocation focuses on preserving liquidity and funding growth initiatives rather than shareholder returns at this stage [S7], [S22].

Key Personnel and Talent Retention

Retention of key leadership—particularly the CEO—and attraction of specialized scientific talent are emphasized as crucial for maintaining innovation momentum and operational effectiveness.

Summary and Forward-Looking Considerations

Lifeloc Technologies is positioned at the intersection of proven technology leadership supported by patents and regulatory certifications alongside financial headwinds characterized by sustained losses and concentrated customer exposure.

Key areas for monitoring include:

- Successful integration of the merger partner and effective deployment of newly raised capital toward product development,

- Progress on patent portfolio management amid competitive technological advancements,

- Operational resilience against supply chain disruptions exacerbated by geopolitical uncertainties,

- Diversification efforts reducing reliance on major customers lacking contractual commitments,

- Ongoing compliance with complex regulatory frameworks ensuring market access,

- Capital structure management balancing debt servicing against liquidity preservation.

This analysis relies exclusively on publicly available SEC filings ([F1],[S#]) and recent news disclosures ([N1]) without speculative extrapolation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments