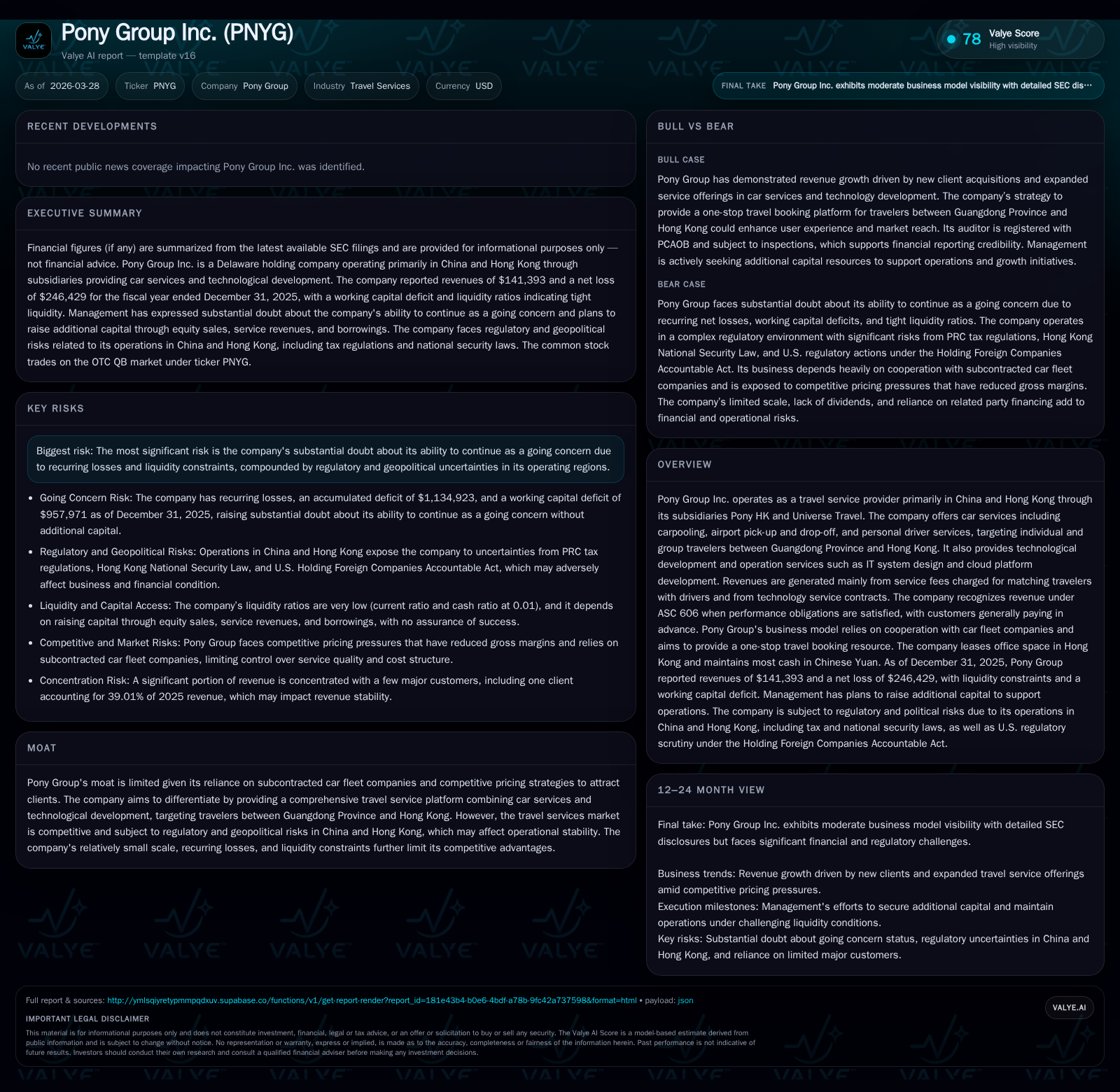

Pony Group Inc. Pursues Growth Despite Persistent Losses and Capital Constraints

The company expands its travel service platform spanning Guangdong and Hong Kong, while liquidity and margin pressures persist.

Pony Group Inc. operates a travel service model linking Guangdong Province and Hong Kong, combining car services through subcontracted fleets with a technology-driven one-stop platform. The company achieved 45% revenue growth in 2025 driven by new clients but saw gross margin erosion due to competitive pricing strategies. Operating losses widened amid increased accrued consulting fees, and cash flow remained negative, signaling liquidity strain with a working capital deficit near $958K. Management’s ability to continue operating hinges on securing additional financing, as substantial doubt about going concern remains pronounced.

Business Model and Market Footprint

Pony Group Inc., through subsidiaries Pony HK and Universe Travel, offers travel-related car services mainly targeting individual and group travelers between Guangdong Province and Hong Kong [S1]. Services include carpooling networks, airport pick-up/drop-off, and personal driver arrangements facilitated via subcontracted vehicle fleet companies. Revenue is recognized under ASC 606 when contractual performance obligations are met, typically upon completion of rides with customers generally prepaying for services [S1][S22]. Alongside these offerings, Pony Group develops technology platforms including IT system design and cloud infrastructure aimed at providing an integrated travel booking experience [S1]. Operations span mainland China and Hong Kong jurisdictions, introducing complex regulatory compliance challenges.

Revenue Growth and Margin Compression

From FY2024 to FY2025, Pony Group's revenue grew approximately 45%, increasing from $97.4K to $141.4K [F1], significantly influenced by new client Benfu Development Ltd., which contributed about $55.2K in car service revenue in 2025 [S1]. Despite this growth, gross margin declined from about 43% in FY2024 to 33% in FY2025 due to aggressive pricing strategies aimed at client acquisition amid competitive pressures [S1][F1].

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 141393 | -246429 | -101270 | -245660 | +45.2% | -50.2% |

| 2024 | 97394 | -164074 | -148977 | -163036 | -45.2% | -10.5% |

| 2023 | 177570 | -148521 | -152949 | -147838 | +57.4% | +44.8% |

| 2022 | 112844 | -269078 | -325329 | -274625 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 25.9 |

| 2024 | 24.3 |

| 2023 | 28.7 |

| 2022 | 75.7 |

Source: SEC companyfacts cache [F1].

*Year-over-year percentages relative to prior year.

Operating losses increased substantially alongside margin compression despite revenue gains [F1]. This reflects limited operating leverage amid rising costs.

Client Concentration and Supplier Dependence

Benfu Development Ltd. accounted for roughly 39% of total revenue in FY2025 with another individual customer contributing about 19%, indicating significant client concentration risk [S6]. On the supplier side, nearly 78% of subcontracted vehicle services were sourced from Yahong Business Limited during FY2025 [S6], highlighting vendor concentration that could impact operational stability.

This dual concentration underscores vulnerability to shifts in demand or service disruptions among key clients or suppliers.

Cost Structure and Operating Loss Drivers

Operating expenses rose approximately 43% year-over-year to about $293K in FY2025 from roughly $205K in FY2024 [S1][F1], primarily driven by accrued but unpaid consulting fees—a non-cash expense affecting reported results [S8]. Fixed administrative overheads combined with volume-based subcontracted service costs limited operating leverage benefits.

These dynamics reflect ongoing efforts to balance growth investments—including technology development—with cost control under tight financial constraints.

Capital Structure and Liquidity Challenges

As of December 31, 2025, current assets totaled about $13.7K against current liabilities near $972K—a current ratio around 0.01—signaling acute liquidity pressure [F1][S24]. Cash reserves were approximately $9.7K at year-end [F1]. Related party payables reached $770K owed mainly to founder Wenxian Fan who provided interest-free loans covering salaries and supplier payments [S6].

A working capital deficit near $958K coupled with recurring negative operating cash flows (-$101K in FY2025) underscores critical dependence on external capital infusions for ongoing operations [F1][S3][S4][S16]. Management has acknowledged substantial doubt regarding the company's ability to continue as a going concern absent successful financing [S3][S4][S18].

Going Concern Considerations and Funding Plans

The company’s audited financial statements were prepared assuming continuation as a going concern despite accumulated deficits exceeding $1.13 million as of FY2025 end and net losses nearing $246K during the year [F1][S3]. Management plans include raising capital through equity sales, bank borrowings (short- and long-term), related party loans, and strategic collaborations [S3][S6].

However, there is no assurance these efforts will sufficiently address liquidity challenges imminently [S14]. Operating cash flow burn remains significant relative to available resources.

Technology Development: 'Lets Go' App Initiative

Since January 2019 Pony Group has developed the "Lets Go" mobile app featuring a multilingual interface offering integrated travel bookings targeted initially at foreign visitors traveling within China [S1][S20]. The app supports carpooling along with car rentals and airport transfers; enhancements include English language support and payment integration like PayPal.

This platform aims to diversify beyond traditional services toward broader market penetration including international users—a potential medium-term growth driver amid current financial headwinds.

Regulatory Risks and Geopolitical Factors

Operating chiefly through subsidiaries registered in mainland China and Hong Kong exposes Pony Group to complex regulatory environments including PRC tax rules on indirect equity transfers (Bulletin No.7), limitations on cross-border enforcement affecting shareholder rights abroad, and evolving securities regulations impacting audit transparency due to PCAOB oversight restrictions [S1][S5][S19][S23][S27].

Geopolitical tensions affecting China-Hong Kong corridors add operational uncertainty potentially disrupting fleet availability or traveler demand.

Investor Considerations: Milestones and Capital Allocation Outlook

Absent detailed forward guidance beyond disclosed financing initiatives [N/A][S10][S11], key investor focus areas include successful capital raises via equity or debt that can alleviate liquidity stress.

Operational milestones include restoring gross margins through pricing power recovery post client diversification; expanding the customer base beyond major clients; broadening capabilities via the Lets Go app; reducing accrued expenses; and achieving sustainable positive operating cash flow trends.

No dividends or share repurchases are planned given ongoing losses; capital allocation priorities remain focused on operational survival and strategic growth investments aligned with long-term objectives [S10][F1].

This analysis is based solely on publicly filed regulatory documents ([F1], [S#]) without forecasts or investment recommendations. Pony Group Inc.’s persistent losses combined with severe liquidity constraints highlight critical reliance on effective capital management alongside strategic execution amid complex market conditions around China-Hong Kong travel services.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments