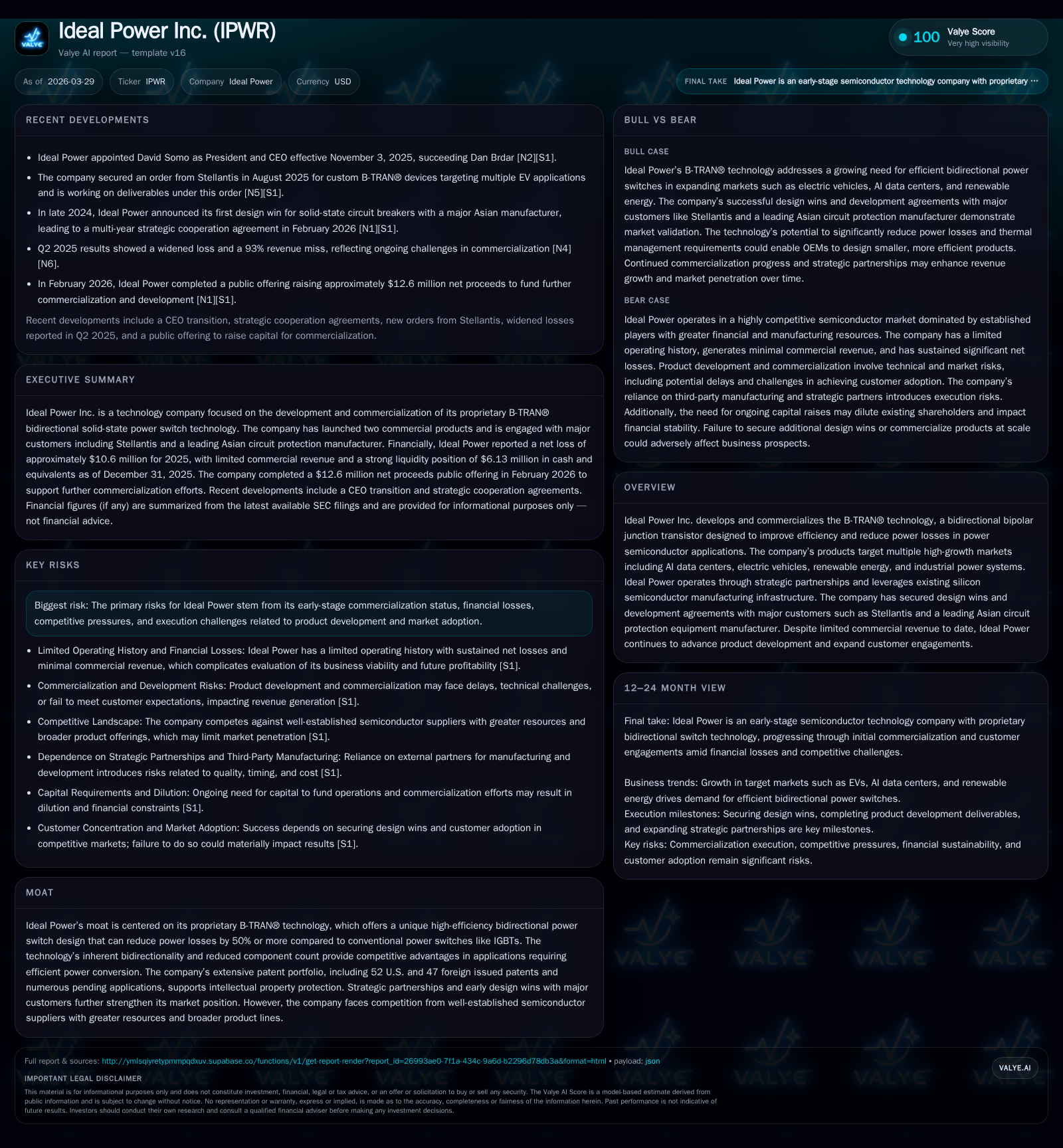

Ideal Power Advances B-TRAN® Commercialization While Managing Early-Stage Losses and Market Entry Risks

Ideal Power Inc. is progressing on its proprietary bidirectional bipolar junction transistor technology, targeting high-growth power semiconductor markets amid ongoing commercialization challenges.

Ideal Power Inc. is focused on developing and commercializing its patented B-TRAN® power semiconductor technology, which offers efficiency gains for bidirectional power conversion applications such as EVs, AI data centers, and renewable energy systems. The company remains early-stage with limited commercial revenue but has secured strategic design wins with major customers like Stellantis and a leading Asian circuit protection manufacturer, validating its potential. Despite operating losses exceeding $10 million annually and negative cash flow, Ideal Power leverages partnerships and existing fabrication infrastructure to advance product development while navigating competitive pressures from established semiconductor firms.

Company Overview

Ideal Power Inc., founded in 2007 and based in Texas with Delaware incorporation since 2013, is developing the B-TRAN® technology—a bidirectional bipolar junction transistor designed to enhance power conversion efficiency by reducing conduction losses by more than half relative to conventional insulated gate bipolar transistors (IGBTs) widely used in power semiconductors [S1][S26]. The firm leverages existing silicon wafer fabrication infrastructure through strategic partnerships rather than owning manufacturing facilities directly, enabling a focus on product development and customer engagements.

Historical Performance and Financial Summary

Since inception, Ideal Power has maintained a limited operating history primarily marked by ongoing R&D expenditure aimed at commercializing B-TRAN®. Revenues remain negligible, reflecting its pre-revenue stage nature: commercial sales were $37,728 in 2025 versus $86,032 in 2024 [S1]. Operating losses have been stable around $10 million annually (operating income -$10.9M in 2025 vs -$11.1M in 2024), consistent with sustained investment into prototypes, testing, and customer qualification activities [F1].

Cash flow from operations remains negative (-$9.1M in 2025), offset slightly by low capital expenditures (~$119K in 2025) given reliance on partner manufacturing [F1]. Year-end cash balances approximated $6.1M following a February 2026 equity raise netting ~$12.6M intended to fund ongoing commercialization [S9]. The balance sheet shows a strong current ratio near 6.7x reflecting low liabilities but modest equity at ~$7.9M due to accumulated losses [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | -9 | -11 | 119481 | -1.5% |

| 2024 | -10 | -9 | -11 | 197266 | -4.7% |

| 2023 | -10 | -7 | -10 | 240825 | -38.5% |

| 2022 | -7 | -6 | -7 | 182651 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -9 | -134.3 |

| 2024 | -9 | -58.3 |

| 2023 | -7 | -98.9 |

| 2022 | -7 | -40.1 |

Source: SEC companyfacts cache [F1].

Revenue growth is not meaningful due to early commercialization stage; operating losses reflect consistent R&D spend.

Technology and Market Positioning

The company’s proprietary B-TRAN® device integrates the functions of multiple conventional IGBTs and diodes into a single bidirectional switch element. This innovation promises system-level benefits including reduced voltage drops leading to higher efficiency and lower thermal dissipation requirements across multiple applications: electric vehicle contactors and drivetrain inverters, solid-state circuit breakers (SSCBs), AI data center power supplies, renewable energy converters, uninterruptible power supplies (UPS), static transfer switches (STS), among others [S23][S26].

This differentiated approach addresses inefficiencies inherent in traditional bidirectional circuits that require multiple discrete components arranged in complementary pairs, adding complexity and losses.

Supporting intellectual property includes an extensive portfolio with more than fifty U.S. patents issued plus foreign counterparts covering device design and manufacturing processes [S26][S18]. The company acknowledges competition from major semiconductor incumbents such as Infineon Technologies AG, Texas Instruments, STMicroelectronics NV among others; however, none currently offer a comparably efficient true bidirectional device at scale which presents Ideal Power with a potential niche moat [S26][S27].

Strategic Partnerships and Customers

Ideal Power has secured key partnerships illustrating progress towards market adoption:

Stellantis: A multi-phase development agreement initiated in 2022 focuses on using B-TRAN® modules within EV drivetrain inverter applications for Stellantis’ next-generation electric vehicles [S11][S23]. While prioritization recently shifted toward contactor applications over drivetrain inverter deployment due to program timing considerations [S11], this engagement demonstrates important credibility with a top-ten global automaker.

Asian Circuit Protection Equipment Manufacturer: Late-2024 saw the company score its first design win for SSCB products incorporating B-TRAN®, followed by successful prototype deliveries completed early in 2025 leading to a multi-year cooperation agreement signed in February 2026 [S9]. This includes joint product design and testing milestones confirming engineering viability prior to commercial launch.

Additional discussions continue with global automotive tier-one suppliers as well as channel partners such as module manufacturers poised to help distribute B-TRAN® based modules broadly [S15].

Growth Prospects and Risks

Growth Drivers:

- Conversion of design wins into volume commercial orders typically follows OEM validation cycles lasting approximately one to one-and-a-half years post-win announcement; automotive applications generally see even longer development lead times due to stringent certification standards [S23].

- Expansion into rapidly growing end-markets: EVs are expected to inject continuous demand for sophisticated power semiconductor devices; similarly accelerated deployments in AI data centers require efficient power electronics benefiting from B-TRAN’s bidirectionality.

- Successful licensing or distribution agreements beyond initial partners could accelerate market penetration without requiring heavy capital investment.

Risks:

- Early-stage commercialization entails inherent challenges including prototype manufacturing delays and driver circuit co-development complexities essential for reliable B-TRAN® integration [S20].

- Larger competitors possess deeper resources for patent litigation defense or technology duplication risks; enforcement of IP rights may be protracted or expensive impacting competitive positioning [S4][S21].

- Supply chain dependencies on third-party silicon wafer providers and packaging firms expose the business to external disruptions such as logistics bottlenecks or tariffs affecting product costs [S28][S10].

- Reduced governmental support for targeted sectors like electric vehicles under certain administrations may slow adoption velocity affecting addressable market expansion [S25][S22].

- Financially sustained losses necessitate continued capital raises which could dilute shareholders or constrain long-term operational viability absent revenue growth [F1][S7].

Capital Allocation & Returns

Ideal Power has not generated profits since inception nor paid dividends or engaged in buybacks; the board explicitly states all earnings will be reinvested into advancing B-TRAN® products and scaling business operations when possible [S7]. With no current path outlined toward profitability given reliance on emerging volumes yet to materialize from design wins under evaluation/testing phases, return metrics like ROE stand deeply negative (~ -134%) illustrating the nascent operational stage [F1].

Investments primarily target R&D expenses elaborating new product designs or qualifying wafers/processes rather than fixed assets given an outsourced production model (Capex approximately $119K in FY2025 down from prior years levels) [F1][S20]. This suggests a lean asset base suitable for innovation but sensitive to funding constraints.

Outlook & Key Milestones

The company's near-term outlook hinges on successfully moving from prototype shipments to full-scale production orders from key customers such as Stellantis or the Asian SSCB manufacturer—critical milestones indicating commercial traction [N1][S9][S11]. Additional announced design wins or licensing contracts would further validate technology acceptance across different power semiconductor submarkets.

Management’s ability to maintain adequate liquidity through timely capital raises under favorable terms will dictate operational continuity amid sustained operating losses [F1][S7]. Patent portfolio defense actions or potential infringement claims involving larger competitors could significantly impact legal costs or product availability.

Broader industry trends like commodity silicon wafer pricing shifts or geopolitical trade policies might materially affect cost structures further impacting gross margins once revenues ensue.

Conclusion

Ideal Power represents deep tech innovation within the power semiconductor space targeting transformative efficiency improvements through pioneering B-TRAN® devices tailored for directionally complex electricity switching needs found increasingly in electrified transportation and data infrastructure ecosystems. The company’s current status reflects typical characteristics of pre-revenue technology ventures: steady financial outflows backing advanced prototyping campaigns coupled with encouraging but nascent early adopter engagements.

The path forward depends heavily on execution precision—moving promising prototypes through stringent OEM validation hoops into production ramps—and managing financial runway amid escalating industry competition from entrenched semiconductor giants while safeguarding critical IP assets.

Disclaimer: This analysis is based solely on publicly available information up to March 29, 2026, including SEC filings and credible news sources cited herein. It is provided for informational purposes only without any recommendation for investment action.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments