Critical Factors Shaping Aptevo Therapeutics’ Pipeline and Financial Outlook

Aptevo Therapeutics confronts capital constraints and clinical-stage risks while advancing its immunotherapeutic candidates developed on the ADAPTIR platform.

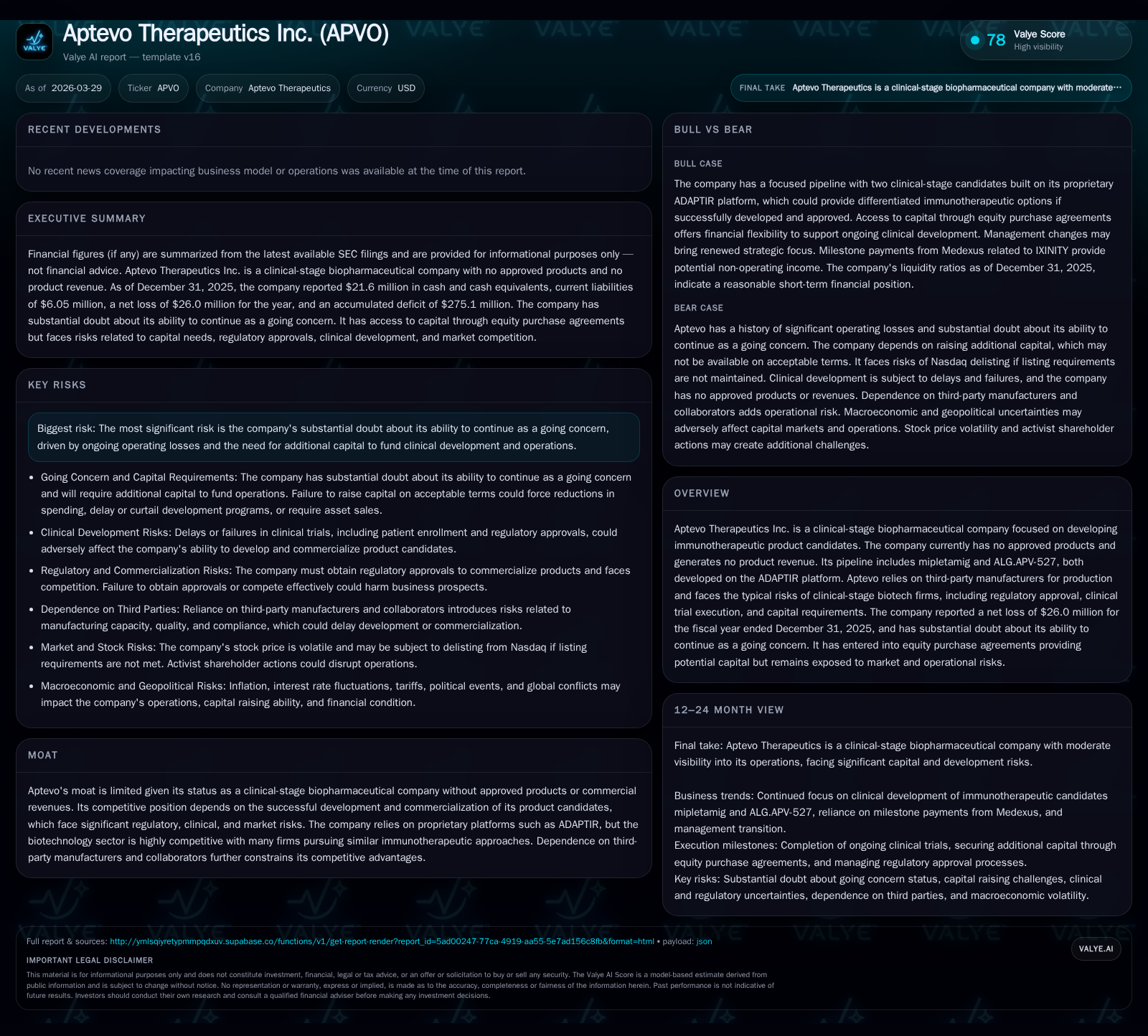

Aptevo Therapeutics remains a clinical-stage biotech without revenue from approved products, facing substantial operating losses and ongoing capital needs that raise going concern issues. The company’s development efforts center on immunotherapy candidates mipletamig and ALG.APV-527, leveraging its proprietary ADAPTIR platform amid significant regulatory and clinical execution risks. Expanding operating deficits and negative cash flows underscore reliance on equity purchase agreements to sustain R&D activities. Future progress hinges on successful trial milestones alongside proactive liquidity management in a competitive immunotherapy landscape.

Historical Financial Trajectory Highlights Expanding Operating Deficits

Aptevo Therapeutics’ financial history illustrates the typical trajectory of a clinical-stage biopharma firm intensely focused on R&D with no approved products or commercial sales. The company reported revenues of approximately $14.7 million in FY2017, representing a significant increase from $8.8 million in FY2016 [F1]. Despite stable or growing top-line figures during earlier years, these revenues do not stem from product sales but rather from license fees, collaborations, or milestone payments tied to existing agreements.

Operating income has remained persistently negative throughout recent years, with a loss of $26.3 million recorded for FY2025, a deterioration compared to prior years (FY2024: -$24.6 million; FY2023: -$28.9 million) [F1]. Net income follows a similar trend, with FY2025 losses near $25.97 million, reflecting an operating environment marked by high development costs and absent commercial revenue streams.

The operating cash flow deficit has also steepened, reaching -$25.6 million in FY2025 compared to -$23.8 million in FY2024, revealing escalating cash consumption congruent with clinical advancement activities [F1]. Capital expenditures remain minimal — only about $29,000 annually in recent years — emphasizing that outlays are primarily tied to product development rather than fixed asset investments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -26 | -26 | -26 | -7.6% | |

| 2024 | -24 | -24 | -25 | -38.6% | |

| 2023 | -17 | -12 | -29 | 29000 | -316.9% |

| 2022 | 8 | -21 | -29 | 29000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -149.4 | |

| 2024 | -507.5 | |

| 2023 | -12 | -142.5 |

| 2022 | -21 | 44.7 |

Source: SEC companyfacts cache [F1].

Note: Data for the years outside those specified above was unavailable.

These metrics underscore Aptevo’s widening operational deficits even as revenue remains largely unchanged at a modest scale relative to expenses.

Pipeline Development: Leveraging ADAPTIR Amid High Clinical Risk

Aptevo’s developmental efforts concentrate on the ADAPTIR platform—a proprietary modular immunotherapy technology geared toward producing bispecific antibodies designed to stimulate targeted immune responses against cancers [S1][S20]. This platform underpins two principal investigational assets: mipletamig and ALG.APV-527.

Neither candidate has garnered regulatory approval; accordingly, Aptevo does not generate product revenue from these programs [N1][S1]. Progress through clinical phases exposes the company to inherent risks prevalent in biotech: delayed patient enrollment or site initiation can push back critical readouts; adverse safety signals could halt trials; and FDA or equivalent bodies may withhold approvals if data fail to meet stringent efficacy or safety standards [S1][S17].

Past experiences have informed platform refinements—APVO414 and APVO210 were discontinued following immunogenicity concerns related to anti-drug antibodies (ADA), illustrating the difficulty in balancing efficacy with patient safety within this modality [S17]. As the company advances the current pipeline candidates through Phase 1b/2 trials for mipletamig and Phase 1 trials for ALG.APV-527 [N1], meticulous trial execution and robust regulatory interaction remain paramount.

Dependence on third parties is notable—contract research organizations conduct clinical trial activities while manufacturers produce drug supply under Good Manufacturing Practice (GMP) guidelines—a structural hurdle that tempers operational control but is standard within early-stage biopharma [S1].

Capital Structure and Liquidity: Navigating Going Concern Doubts

A salient financial red flag is company management's explicit statement of "substantial doubt" about Aptevo’s ability to continue as a going concern—a direct consequence of recurring net losses eroding equity and limited cash reserves [S19][F1].

As of December 31, 2025, Aptevo held roughly $21.6 million in cash and equivalents against current liabilities totaling approximately $6 million—translating into a relatively robust current ratio of about 3.82x [F1]. While this measure reflects short-term liquidity adequacy at the reporting date, it must be contextualized with operating cash flow burn rates exceeding $25 million annually.

To address funding requirements for ongoing clinical trials and general operations beyond current cash reserves, Aptevo has secured standby equity purchase agreements (SEPAs) totaling up to $85 million over three years—comprising $25 million from mid-2025 and another $60 million executed in early 2026—with approximately $67.5 million capacity still available as of filing [S19][S21]. These facilities provide flexibility but underscore unresolved structural financing risks given dependence on capital markets or investor willingness.

The inability to secure acceptable terms on additional financing could compel cost reductions including scaling back R&D programs or relinquishing commercialization rights—all scenarios potentially detrimental to strategic objectives [S19][S21].

Regulatory and Compliance Challenges in Immunotherapeutics

Aptevo faces multilayered regulatory hurdles endemic to biotechnology drug development. FDA approval necessitates expansive data packages evidencing safety and efficacy derived from adequate Phase-controlled studies; failure at any stage halts progression [S4][S26]. Moreover, post-approval surveillance obligations impose ongoing compliance costs rarely paralleled in other sectors.

Healthcare fraud-related laws compound operational strictures. The federal Anti-Kickback Statute broadly proscribes remuneration intended to induce referrals involving federally funded programs like Medicare or Medicaid—extending constraints onto marketing practices and pricing policies [S5][S7]. Recent legislative amendments under the Affordable Care Act further lowered thresholds for proving violations by removing intent requirements [S5].

Relatedly, provisions like the False Claims Act expose Aptevo to civil whistleblower suits even absent government intervention—an operational threat magnified by evolving interpretive uncertainties around compliance obligations [S6][S9]. Additionally important are privacy laws such as HIPAA/HITECH statutes governing protected health information security standards affecting clinical data handling practices [S8][S13].

State-level regulations require transparency in payments made to healthcare providers under statutes paralleling federal laws (e.g., Physician Payments Sunshine Act), heightening administrative burdens further complicating commercial preparation [S13][S14].

Noncompliance penalties are material—ranging from fines to exclusion from federal health programs—which would severely disrupt prospective commercialization pathways if triggered.

Competition Landscape and Platform Differentiators

The immuno-oncology sector is characterized by intense competition encompassing major pharmaceutical conglomerates alongside nimble biotechs innovating bispecific antibody modalities similar or adjacent to Aptevo’s ADAPTIR technology [N1][S20]. Key competitors include industry leaders such as Amgen, Genentech (Roche), Bristol Myers Squibb along with numerous specialized developers like Macrogenics or Xencor who advance similar bispecific formats.

Market penetration will depend heavily on differentiation factors including efficacy attributes evaluated through rigorous comparative analysis versus existing therapies; cost-effectiveness assessments; safety profiles; and ease-of-administration considerations critical for clinician adoption [S20]. Aptevo’s standing is constrained by absence of approved products limiting its brand recognition or customer relationships relative to incumbents who also leverage extensive commercialization capabilities.

Moreover third-party manufacturing reliance imposes operational dependency risks that could impede timely supply scaling necessary upon regulatory approval—a nontrivial factor influencing competitive agility in oncology biologics markets.

Forecast Pathways: Clinical Milestones to Watch and Analytical Perspectives

Explicit forward guidance regarding anticipated clinical milestone timelines is not disclosed in filings examined [N1][S3], necessitating careful monitoring of trial updates as primary indicators of value inflection points.

Key developmental events include anticipated Phase 1b/2 data readouts for mipletamig addressing safety signals and preliminary efficacy markers essential for progressing towards pivotal studies. Likewise initiation and progress along Phase 1 dosing escalation for ALG.APV-527 bear scrutiny given their early-stage status [N1].

Regulatory submission timing remains uncertain pending clinical outcomes but will dictate future de-risking phases enabling potential partnerships or licensing discussions accelerating commercialization potential.

Analytically speaking, successful demonstrable proof-of-concept combined with prudent cash management represents pivotal junctures shaping sustainability prospects concurrently with financing environment volatility.

Management’s Capital Allocation Strategy: Cash Flow Burn, Equity Raises, and Returns

Aptevo’s recurrent operating cash flow deficits exceeding $25 million illustrate substantial burn rates commensurate with costly clinical-stage development programs without offsetting revenue streams [F1]. The company allocates minimal capital toward fixed assets (capex approximately $29 thousand recently), affirming focus strictly on R&D activities rather than infrastructure expansion.

With no evidence pointing toward dividend issuance or share repurchase plans—as typical among precommercial biopharmas—the company's shareholder returns are currently nonexistent reflecting a growth-at-all-costs posture centered on pipeline maturation before monetization possibilities emerge [F1].

Return on equity metrics paint a stark picture: approximately -149% ROE for FY2025 measuring large losses against a modest equity base around $17.4 million illustrating acute financial stress yet emphasizing shareholder dilution risk inherent with continued equity financings needed to fund operations [F1][S19].

Continued reliance on standby equity purchase agreements conveys commitment toward preserving operational runway though it entails potential dilution amplifying importance of achieving upcoming value catalysts promptly.

This analysis synthesizes publicly filed financial data alongside detailed regulatory disclosures without speculation beyond documented milestones or guidance statements. Aptevo Therapeutics typifies challenges common among small-cap clinical-stage biopharmaceutical companies striving to advance promising pipelines amid funding constraints odd regulatory complexities. Stakeholders should maintain vigilance regarding clinical trial outcomes alongside evolving capital market conditions that will decisively influence the company's strategic trajectory going forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments