MODIV Industrial’s Lease Extensions Bolster Stability as Profit Margins Narrow

Long-term lease renewals and interest rate hedges underpin MODIV Industrial’s rental income stability despite compressed profitability.

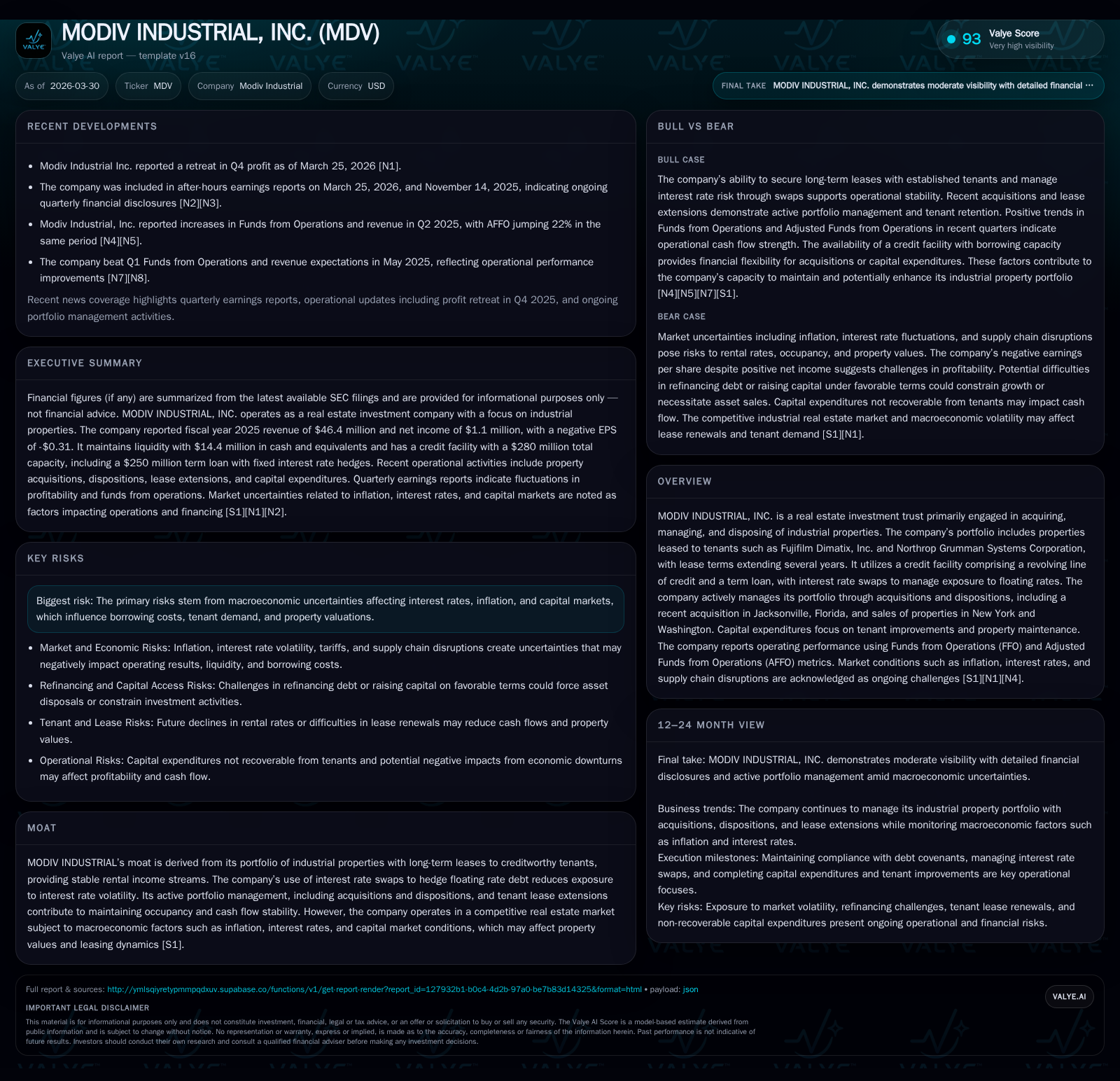

MODIV Industrial, Inc. experienced revenue contraction and considerable declines in profitability for fiscal year 2025, reflecting margin pressures within a challenging macroeconomic environment. The company secured multi-year lease extensions with key tenants Fujifilm Dimatix and Northrop Grumman, which alongside interest rate swaps fixing borrowing costs, provide a defensive income foundation. Capital structure adjustments including credit facility amendments and preferred stock repurchases form part of an active capital management approach amid inflation and interest rate headwinds. Investors should monitor upcoming lease expirations, effectiveness of hedging beyond 2026, and leasing market dynamics that could affect cash flow stability.

From Rapid Growth to Profit Pressure: Historical Performance at MODIV Industrial

MODIV Industrial has demonstrated significant growth over recent years in its industrial property portfolio but confronted sharp profit margin pressures heading into FY2025. Revenue peaked near $46.8 million in FY2024 but slightly declined by approximately 0.8% to $46.4 million in FY2025 [F1]. Despite stable topline figures, operating income contracted by 28%, falling from about $21.9 million in FY2024 to $15.8 million in FY2025. Net income decline was even more pronounced at over 82%, dropping to just around $1.07 million [F1]. This decoupling signals meaningful compression across operating margins likely reflecting increased expenses or less favorable lease economics.

In contrast to earnings softness, operating cash flow sustained at nearly $15 million in FY2025 (down roughly 18% from FY2024's $18.2 million), indicating continued positive core operational cash conversion albeit at reduced scale [F1]. Inflationary pressures on maintenance and administrative costs combined with macro-driven challenges have squeezed earnings despite the resilient rent roll.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 46 | 1 | 15 | 16 | -0.8% | -82.3% |

| 2024 | 47 | 6 | 18 | 22 | +191.0% | |

| 2023 | -7 | 17 | 2 | -101.1% | ||

| 2022 | -3 | 17 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 0.7 |

| 2024 | 12 | 3.2 |

| 2023 | 1 | -4.6 |

| 2022 | 4 | -2.1 |

Source: SEC companyfacts cache [F1].

Lease Renewal Success and Hedge Strategies: Anchoring Portfolio Stability

The company reinforced its core portfolio stability via significant lease renewals during calendar year 2025: Fujifilm Dimatix agreed to a ten-year extension through March 2036 on its Santa Clara property, while Northrop Grumman Systems Corporation extended for five years through mid-2031 [S1]. These renewals cover major portions of annual base rent (ABR), reducing rollover risk substantially over the near-to-medium term.

Hedging stands as a further bulwark against rising interest costs amid volatile monetary policy environments. MODIV utilizes pay-fixed, receive-floating interest rate swaps aligned with its Term Loan facility ($250 million principal). Initially entered into two swap agreements in January 2025 locking SOFR at approximately 2.45% for that year resulting in an all-in fixed borrowing cost around 4.25%. In January 2026, these were replaced with three new contracts similarly fixing SOFR for the calendar year at the same level but achieving a slightly lower effective fixed rate of about 4.15% due to leverage-based pricing grid benefits [S1][S4][S9]. The swaps are designated as cash flow hedges under GAAP, mitigating quarterly earnings volatility caused by floating rates fluctuations; premiums paid ($2.7 million aggregate) are amortized across the hedge period increasing quarterly interest expense moderately [S1][S9].

This approach reflects prudent risk management common among industrial REITs facing historically elevated rates post-Fed hikes, balancing debt cost with predictable cash flows.

Macroeconomic Headwinds and Their Impact on Future Growth Prospects

Persistent inflation and uncertain Federal Reserve monetary tightening cycles form material headwinds detailed extensively in risk disclosures [S1][S11][S24]. Elevated inflation elevates certain property operating costs—taxes, maintenance—that tenants typically reimburse yet can strain landlord expense control when reimbursements lag market escalation or leases cap increases conservatively.

Moreover, longer-term leases may not adjust sufficiently quickly to keep pace with prevailing market rents under sustained inflation scenarios, limiting upside potential from contractual escalators embedded within existing leases [S1]. Rental concessions or free rent periods may increase if market rents soften or economic downturns modestly depress tenant demand.

The company reports only a single lease scheduled for expiration within a foreseeable horizon beyond calendar year end—namely June 30, 2027 on the Husqvarna-leased Charlotte location—which reduces immediate rollover risk but places spotlight on mid-term tenant retention challenges [S1]. Volatility persists regarding capital market access which influences refinancing costs or asset valuations potentially capping valuation appreciation.

Capital Structure Maneuvers Amid Interest Rate Volatility

MODIV’s credit facility amounts to $280 million split into a $30 million revolving line of credit and a $250 million term loan bearing floating rates indexed to SOFR plus spreads that vary based on leverage ratio performance [S4][S6]. An amendment executed in January 2026 extended facility maturity from January 2027 to July 18, 2028 while removing a small SOFR basis point adjustment enhancing cost predictability [S4]. No revolver borrowings were outstanding as of December 31, 2025 ensuring liquidity flexibility [S4].

The facility incorporates customary representations and covenants; collateral includes operating partnership interests in specific entity-owned properties securing debt instruments [S20]. The weighted average fixed rate on all indebtedness equals approximately 4.14% facilitated by the combination of mortgage fixed-rate notes maturing post-September 2027 plus interest rate swaps fully hedging Term Loan SOFR exposure throughout calendar year 2026 [S9].

However, prepayment fees (notably a $0.7 million fee paid coincident with asset disposition), derivative amortization expenses quarterly totaling ~$0.6 million, and potential refinancing risks underscore the ongoing need for tactical capital steering under uncertain macro conditions [S7][S9][S13].

Dividend Policy, Cash Flows, and Share Repurchase Trends

Capital allocation emphasizes steady distributions alongside opportunistic preferred stock repurchases rather than common share buybacks post-2024 [F1][S5][S12][S15]. Common stock buybacks ceased entirely during FY25 after aggregate prior-year purchases exceeding $11 million [F1]. Instead, proceeds from equity offerings fund partial preferred stock repurchases—for example, nearly $7.1 million of Series A Preferred shares repurchased between March–December 2025—and the repurchase program was extended through December 31, 2027 capped at about $49.6 million cumulative authorization [S12][S15].

Dividend increases were moderate: the board authorized raises from an annualized distribution of $1.15/share to $1.17/share beginning January 31, 2025 then further to $1.20/share effective early 2026 paying monthly installments of about $0.10/share reflecting stable payout policy amid margin compression [S12][S22][S27].

Operating cash flow generation is robust relative to capital expenditures—calculated free cash flow approximates $13.96 million (CFO minus capex)—supporting dividend sustainability despite tightened earnings in FY25 [F1][S16]. Tenant improvements adapt properties competitively rather than expanding footprint extravagantly aligning with industrial REIT best practices focused on enhancing tenant satisfaction without diluting financial resilience.

Key Metrics to Watch: What Investors Should Monitor Next

Important future indicators include:

- Timing and results of potential new hedging contracts extending beyond December 31, 2026 as current swaps expire; inability to renew swaps under similar terms could raise cost volatility exposures [N1][N2][S1].

- Lease expiration schedules beyond calendar year-end highlighting the Husqvarna lease mid-2027 plus any emerging vacancy or renewal challenges.

- Occupancy levels and rental concession patterns serving as leading signals of tenant demand strength or emerging competitive pressures.

- Leverage ratio movements influencing Credit Facility spread tier changes impacting borrowing costs per the pricing grid framework [S4][S9].

- Capital markets environment affecting refinancing opportunities or disposition pricing should asset sales become necessary under liquidity constraints.

Notably the lack of formal earnings guidance necessitates close tracking of quarterly operational disclosures for timely signs of directional shifts; sector cyclicality suggests ongoing caution compatible with proactive portfolio & capital management.

Balancing Opportunistic Acquisitions and Portfolio Pruning

Portfolio optimization remains active with focus on acquiring industrial assets featuring stable long-term tenants while disposing non-core properties where appropriate [F1][S16]. A notable acquisition is the Jacksonville property finalized in early March 2025 purchased partially via Class C OP Units issuance alongside nominal cash consideration; this asset benefits from existing long-duration tenant leases with CPI-linked escalations enhancing organic growth prospects under inflationary backdrops [S16][S27].

In contrast legacy assets in New York and Washington were sold as part of portfolio pruning efforts intended to shift capital toward higher-yielding or strategically aligned industrial properties consistent with evolving portfolio strategy standards typical across industrial REITs focusing on logistics hubs or innovation clusters.

Capital expenditures remain disciplined focusing primarily on tenant improvements enabling retention/lease-up rather than heavy redevelopment investments that could strain margins or liquidity given current market uncertainty risks.[F1][S16]

Disclaimer: This analysis is based solely on information available from public filings and news releases cited herein up through March 30, 2026. It does not constitute investment advice or recommendation but aims to provide an informed assessment of MODIV Industrial’s recent performance trajectory, strategic actions, financial structure dynamics, risks, and key metrics relevant for analysts monitoring this industrial real estate entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments