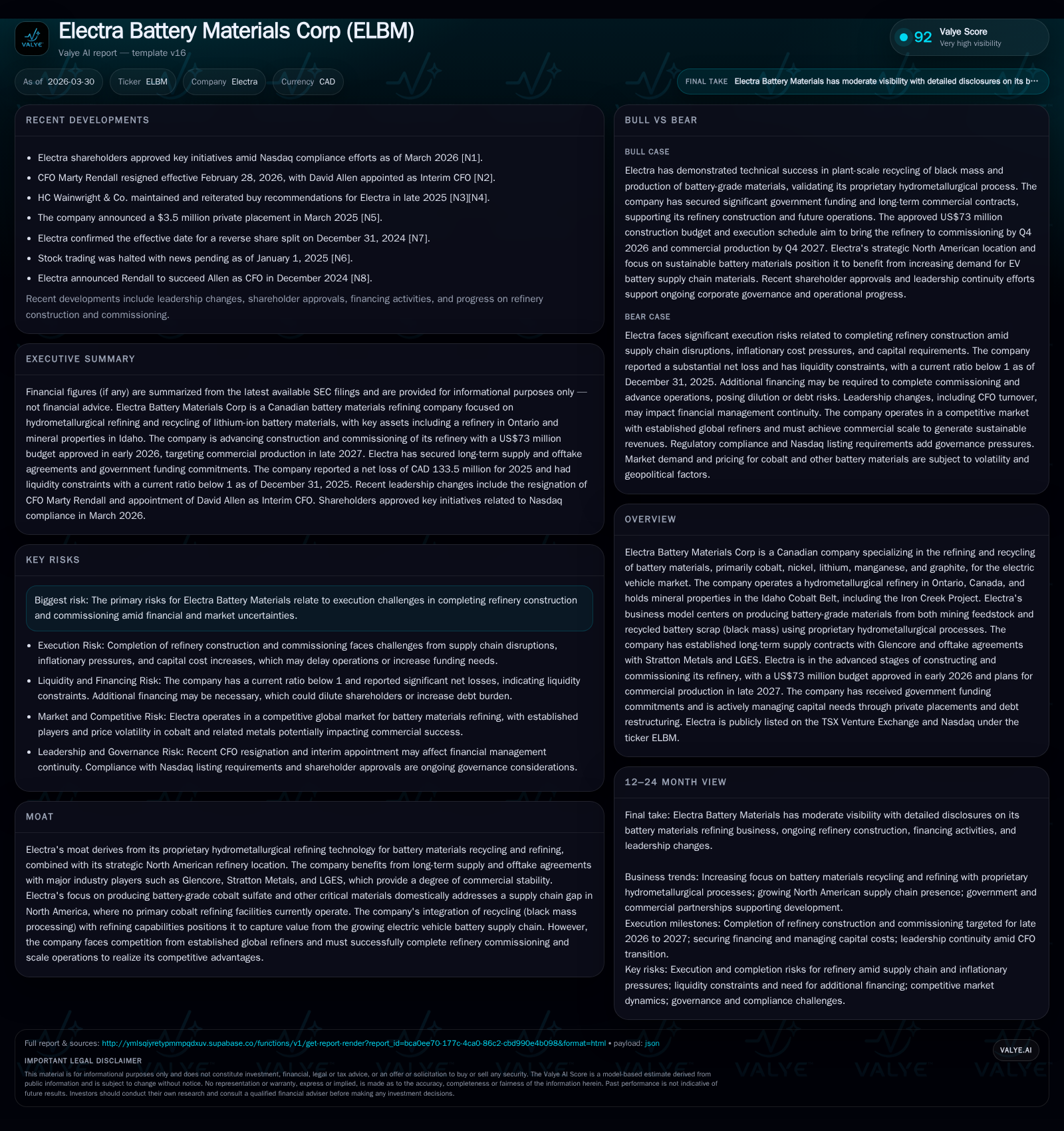

Electra Battery Materials Advances Ontario Refinery with Proprietary Processing Amid Capital Restructuring

Electra targets late 2027 commercial production at its North American cobalt refinery while managing financial losses and securing supply and offtake agreements.

Electra Battery Materials Corp is progressing on the construction and commissioning of its hydrometallurgical refinery in Ontario, targeting commercial production in late 2027. The company’s historical financials reflect heavy losses driven by development expenditures and operational ramp-up costs. Its strategic moat lies in proprietary hydrometallurgical processing combined with integrated battery recycling within North America’s nascent cobalt refining landscape. Continued execution on refinery completion and securing stable feedstock and offtake contracts underpin future growth, while recent capital restructuring and liquidity constraints remain key risks. Electra currently does not generate operational cash flows and expects no dividends in the near term.

Company Overview

Electra Battery Materials Corp (ticker: ELBM) is a Canadian company emerging as a strategic player in North America's battery materials supply chain. The company focuses on refining and recycling cobalt, nickel, lithium, manganese, and graphite primarily for electric vehicle batteries using proprietary hydrometallurgical processes. Electra operates a key hydrometallurgical refinery located in Temiskaming Shores, Ontario, Canada — the first primary cobalt refining facility planned in North America — alongside mineral assets in the Idaho Cobalt Belt including its flagship Iron Creek project [N1][S1].

Historical Performance

The company's financial results reflect its developmental stage with expanding losses due primarily to capital intensive construction activities and operational readiness efforts.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | -133 | -353.2% |

| 2024 | -29 | +54.5% |

| 2023 | -65 | -615.2% |

| 2022 | 13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -288.6 |

| 2024 | -45.8 |

| 2023 | -77.6 |

| 2022 | 9.9 |

Source: SEC companyfacts cache [F1].

Net income deteriorated sharply from a loss of CAD -29.4 million in 2024 to CAD -133.5 million in 2025 [F1]. This steep increase stems largely from intensified refinery construction expenses as well as expenses linked to scaling operational capabilities to handle both mined feedstock and recycled black mass battery scrap.

The negative return on equity of -289% for fiscal year 2025 highlights ongoing capital consumption without returns yet generated — typical for a company transitioning from development to production [F1]. Liquidity ratios are stressed with current liabilities outweighing current assets nearly twofold by end-2025.

Business Model & Competitive Moat

Electra's competitive advantage is anchored in its proprietary hydrometallurgical refining technology tailored for producing battery-grade materials suited to EV manufacturers' stringent standards. The company uniquely integrates refining from both mining feedstock and recycled black mass material within one domestic facility — a distinctive position given the absence of primary cobalt refineries in North America today [N1][S1].

Strategic partnerships augment this moat: long-term supply contracts with global miner Glencore secure feedstock reliability while offtake agreements with Stratton Metals and LG Energy Solution (LGES) underpin committed demand for Electra's refined materials through at least the end of the decade [N1][S24]. This vertical integration reduces exposure to supply chain disruptions prevalent in battery metals markets.

Environmental stewardship further differentiates Electra via its low carbon intensity hydro-powered refining operations—a claim substantiated by independent Life Cycle Assessment data showing substantially lower emissions relative to leading Chinese refiners [S1]. Its ESG commitments also include adherence to responsible sourcing frameworks like the Cobalt Industry Responsible Assessment Framework (CIRAF).

Growth Prospects

The near-term growth narrative hinges on completing construction and commissioning of the Ontario refinery within the $73 million approved budget targeting Q4 2026 commissioning and commercial production ramp-up during Q4 2027 [N1][S24]. Achieving operational scale will enable incremental revenue recognition from cobalt sulfate products alongside other battery chemicals.

Longer-term expansion could be catalyzed by ramping up domestically sourced cobalt supplies from its Idaho mineral properties including Iron Creek—currently undergoing advanced exploration—and expanding recycling capacity via partnerships such as Aki Battery Recycling focused on lithium-ion black mass procurement [S21].

Contractual commitments securing approximately 60% of refinery output through at least 2029 reduce commercialization risk while optional extensions may support sustained production beyond that horizon [N1][S24].

However, growth may be capped temporarily by external factors such as financing availability amid market volatility for battery metals prices as well as any delays or technical challenges during refinery startup.

Financial Outlook & Milestones

While explicit earnings guidance is not provided given the project development phase, critical forthcoming milestones include:

- Completion of final engineering re-baselining ensuring cost control across remaining build phases,

- Achievement of commissioning activities scheduled for Q4 2026,

- Commencement of commercial cobalt sulfate production planned for Q4 2027,

- Securing additional feedstock volumes through recycling partnerships to augment economics.

Investors should monitor construction progress reports closely along with updates regarding liquidity sufficiency given Electra’s dependence on external funding until refinery cash flows stabilize.

Capital Allocation & Returns Profile

Electra's capital structure underwent significant change following its October 2025 debt restructuring which converted sizeable portions (~60%) of convertible notes into equity units priced around US$0.75 per unit alongside issuance of new term loans bearing interest rates near 9% payable semiannually or PIK-style at management’s discretion [S5][S8][S11]. This improved immediate liquidity but increased leverage obligations tied to future cash flow generation.

As at end-2025 balance sheet showed limited cash near CAD $39 million against current liabilities exceeding CAD $88 million resulting in a stressed liquidity profile [F1]. No dividends have been paid historically nor are anticipated while debt remains outstanding—reflecting typical developmental-stage capital allocation focused on execution [S19][S29].

Equity dilution has accompanied multiple financings including private placements aggregating over $20 million since mid-2023 alongside multiple warrant issuances incentivizing creditors and investors aligned towards project delivery rather than short-term returns [S4][S7].

Risks & Challenges

Execution risk stands paramount with refinery commissioning complexity heightened by external inflationary pressures affecting inputs such as steel and labor rates noted during recent re-baseline efforts pushing total capital projections between $155-$167 million with $87 million already incurred as of late-2025 [S24]. Delays or cost overruns would strain financial resources further.

Market risk includes volatility in cobalt prices impacting revenue potential post-production start although long-term contracts mitigate sudden exposure.

Competitive pressures loom from established refiners globally with more mature technology platforms though Electra's North American presence aligns well with regional supply chain initiatives aimed at localizing critical minerals value chains.

Finally regulatory compliance around environmental permits remains critical especially given proximity to protected areas like Salmon National Forest near Idaho mining assets requiring ongoing monitoring plus reclamation obligations totaling above $3 million ensure responsible operations [S1].

Conclusion

Electra Battery Materials is positioned as an important emerging player aiming to fill strategic gaps in North America's battery metal refining capabilities through proprietary technology combined with integrated recycling solutions. Despite challenging financials reflecting deep developmental investment needs and strained liquidity ratios at present,[F1] the company's secured supply/offtake relationships along with government support enhance prospects for successful commercialization. Key near-term indicators will be progress against commissioning timelines and effective working capital management amid refinancing needs. While sizeable execution risks persist alongside competitive industry dynamics, Electra’s differentiated asset base centered on domestic cobalt sulfate production targets a compelling niche amidst accelerating EV electrification trends.

This analysis is prepared strictly for informational purposes without any form of investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments