Planet 13 Holdings’ Scale and Struggles in US Cannabis Markets

Planet 13’s multi-state vertical integration offers scale advantages yet persistent losses and regulatory hurdles cloud its financial outlook.

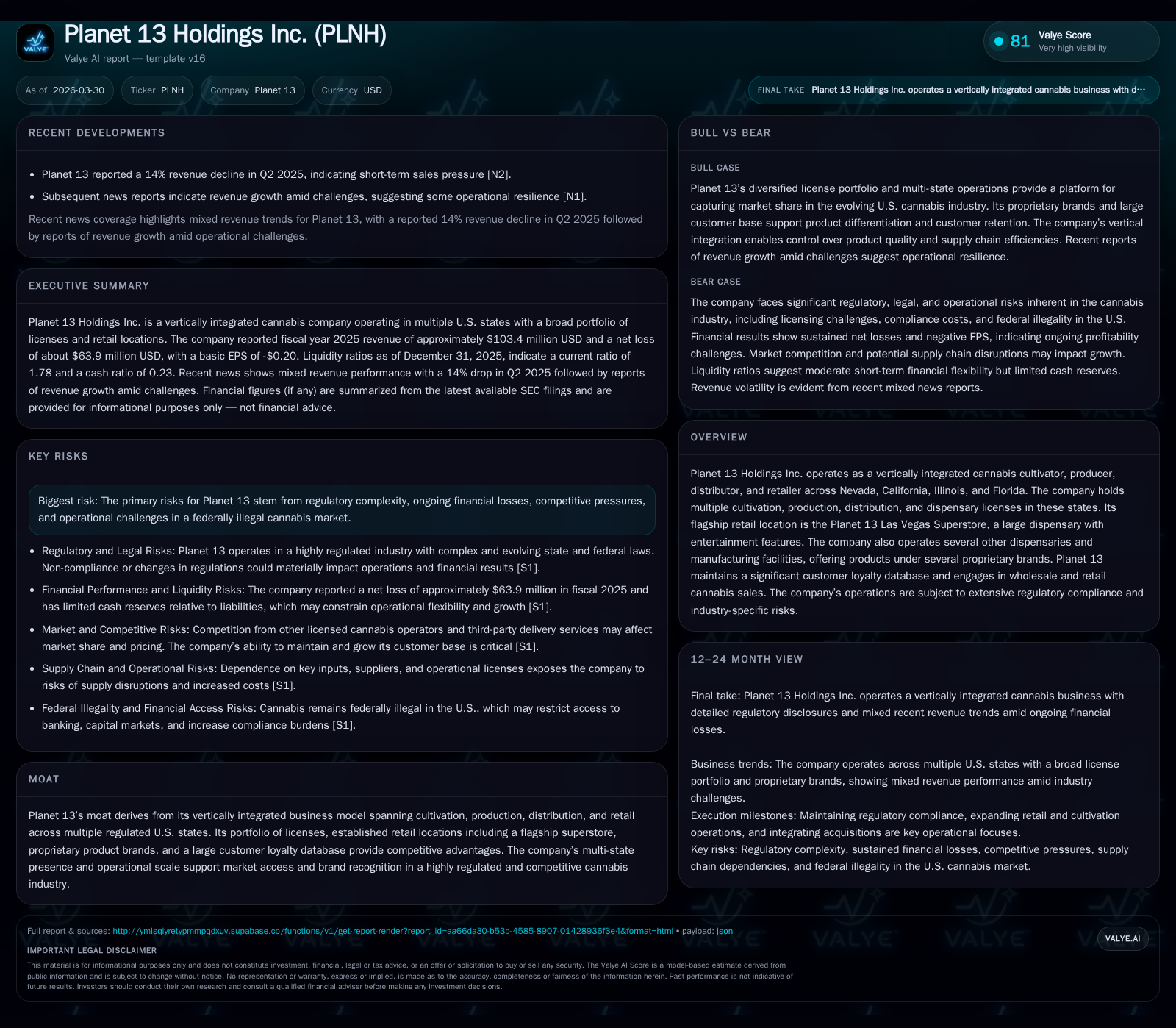

Planet 13 Holdings Inc. operates an extensive vertically integrated cannabis business across Nevada, California, Illinois, and Florida, anchored by its flagship Las Vegas superstore and multiple cultivation, production, and dispensary licenses. Despite a revenue decline to $103M in 2025 from 2024 levels, the company faces widening net losses deepening to over $63M, pressured by regulatory costs and competitive challenges. Its moat stems from proprietary brands and a customer loyalty database exceeding 485,000 members, but federal illegality of cannabis and complex state regulations restrain operational flexibility and financing options. Capital expenditures have been scaled back amid cash flow deficits nearing $21M in 2025. Growth opportunities include expanding dispensaries in Florida and scaling manufacturing capabilities, though ongoing litigation and compliance risks add uncertainty.

Historical Growth Trajectory and Revenue Dynamics

Planet 13’s revenue trajectory over the four fiscal years ending 2025 shows notable volatility amid a rapidly evolving US cannabis industry landscape. The company reached a peak revenue of approximately $116.4 million in FY2024 but declined by over 11% to around $103.4 million in FY2025 [F1]. This reversal contrasts prior growth that lifted revenue from $98.5 million in FY2023. The decline reflects intensified competition across licensed states coupled with regulatory cost pressures that constrain top-line expansion.

Concurrently, net losses have expanded sharply despite the scale attained; losses deepened to nearly $63.9 million in FY2025 from about $47.8 million the prior year, a deterioration exceeding one-third YoY [F1]. The widening deficit underscores challenges with operating leverage where higher fixed costs tied to cultivation and retail infrastructure offset gains from incremental sales.

Operating cash flow also displays a jagged pattern: a positive inflow of $5.2 million was recorded for FY2024 but turned abruptly negative by approximately $14.2 million for FY2025 — representing a near tripling of cash burn from operating activities [F1]. This swing reflects timing effects of working capital alongside increased payments for compliance and administrative functions necessitated by multi-state operations.

Capital expenditures have been curtailed from double-digit millions (over $12 million in FY2024) down to about $6.6 million in FY2025 as Planet 13 moderates its infrastructure investments amid tighter liquidity conditions [F1]. This reduction points to a more cautious spending posture aligned with the need to conserve cash.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 103 | -64 | -14 | 7 | -11.2% | -33.7% |

| 2024 | 116 | -48 | 5 | 12 | +18.2% | +35.1% |

| 2023 | 99 | -74 | -12 | 8 | -5.8% | -23.6% |

| 2022 | 105 | -60 | -7 | 17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | -125.0 |

| 2024 | -7 | -42.4 |

| 2023 | -20 | -68.4 |

| 2022 | -23 | -33.6 |

Source: SEC companyfacts cache [F1].

The data reflects a company striving for scale but grappling with profitability challenges intrinsic to the cannabis sector's regulatory and operational complexity.

Vertical Integration: Core Competitive Advantages and Driver Analysis

Planet 13 is a vertically integrated cannabis operator encompassing cultivation through retail across key US markets including Nevada (its largest base), California, Illinois and Florida [S14]. This extensive license portfolio features six cultivation licenses under Nevada regulation—equally split between medical and adult-use—and permits ownership of multiple production facilities alongside three dispensaries including its hallmark Planet 13 Las Vegas Superstore.

This flagship location combines retail experience with entertainment elements such as interactive product displays and education zones which serve not just transactional purposes but build strong brand engagement—an approach that aligns well with experiential retail trends emerging in regulated cannabis commerce [N1]. Additionally, Planet 13 offers proprietary product lines like HaHa gummies/beverages; Dreamland chocolates; TRENDI flower,vapes,and concentrates; Medizin branded flower,vapes,and concentrates; plus Leaf & Vine floral offerings—all reinforcing brand identity within a fragmented market.

A critical intangible asset lies within its customer loyalty program boasting over 485,000 registered consumers—a sizable database for targeted marketing campaigns that fuels recurring sales volume while enhancing customer retention[S14]. Such scale economies across upstream cultivation through downstream retail support cost management benefits albeit constrained within tight regulatory frameworks.

However,costs related to maintaining this integration — particularly regulatory compliance staffing,this multistate license management,and inventory controls— can weigh heavily on margins compared with single-function operators unable to exploit similar synergies.[S14,N1]

Regulatory Challenges Impacting Operations and Market Access

The largest systemic headwind for Planet 13 remains the discord between state legalization frameworks—which underpin its licensing—and overarching federal prohibition under the U.S Controlled Substances Act (CSA)[S1]. Cannabis remains classified federally as Schedule I,a designation entailing stringent law enforcement risks despite state-law compliance.This discrepancy results not only in legal scrutiny but also substantial practical impacts including:

- Exposure to potential federal enforcement actions which could impose fines,seizures or criminal liability on operations or personnel[S16],

- Severe tax burdens driven by Section 280E Code restrictions disallowing typical business expense deductions limiting effective net income[S1],

- Difficulty accessing banking services forcing reliance on cash-intensive models which increase risk exposure[S1,S23],

- Barriers to interstate commerce due to absence of consistent federal policy obstructing scale efficiencies,

- Costs imposed by state-specific licensure renewals,audits,and environmental regulations necessitating robust compliance programs[S4,S5,S17].

Additionally,the company faces product recall risks inherent in cannabis ingestibles due to contamination or labeling disputes which can lead both to direct recall damages plus reputational harm[S4,S5].The cumulative effect is a high cost burden characteristic of emerging regulated sectors where evolving norms require dynamic adaptation.[S6]

Current Financial Health: Cash Flows, Equity and Capital Structure

At year-end FY2025 Planet 13 reported cash equivalents of approximately $5.3 million against current liabilities near $23 million yielding a current ratio around a modestly comfortable level of approximately 1.78[F1]. Nonetheless,the company’s equity base shrank substantially from about $112 million at end-FY24 down to roughly $51 million at end-FY25 reflecting accumulated net losses eroding book value[F1].

Return metrics remain severely negative with approximate ROE near minus -125%, given persistent net income deficits leveraged against declining equity bases[F1]. Meanwhile,cash flow analysis reveals operating cash outflows deepening sharply by over threefold into negative territory approaching -$14 million last year,[F1] which combined with sustained capital expenditures around $6.6 million nets into a free cash flow deficit north of $20 million indicating continued funding reliance beyond core business operations[F1].

Liquidity disclosures acknowledge ongoing dependence on equity/debt raises while highlighting risk factors concerning access constraints linked explicitly to federal law inconsistencies impeding traditional banking avenues[S10,S18]. The flux in CFO reflects evolving operational cycles particularly inventory management alongside payments for enhanced compliance infrastructures marking a maturing but costly phase for Planet 13.[S15]

Capital Allocation Strategy: Balancing Investment With Shareholder Returns

Capital deployment has pivoted toward more conservative levels with capex nearly halving from values exceeding $12 million preceding year down closer to $6.6 million across fiscal year FY25[F1]. This adjustment demonstrates an emphasis on preserving liquidity amid protracted loss-making although management continues reinvestment primarily focused on facility expansions and efficiency enhancement rather than shareholder distributions.[S7,S8]

No dividends or share repurchase programs have been undertaken nor announced given current financial stressors which is customary for cannabis firms still achieving scale profitability thresholds[S9,F1]. Shareholders face dilution risks linked both organically via equity raises necessitated for cash flow coverage[S7] as well as warrants issued during financings diluting voting/executive control.[S8]

From an analyst perspective,the lack of capital returns is rational yet restricts attractiveness to yield-oriented investors emphasizing price appreciation contingent upon operational turnaround.[S24]

Exploring Growth Opportunities Across Licensed States

Planet 13’s geographically diversified license footprint presents avenues for expansion that could diversify revenue streams albeit subject always to regional regulatory frameworks.Since its subsidiary holds a Medical Marijuana Treatment Center license permitting unlimited medical dispensaries throughout Florida—with thirty-three locations active as of December 31st 2025—this market constitutes significant growth potential relative to adult-use restricted locales.[S14]

The company continues developing Florida cultivation facilities operational approval supporting supply chain vertical integration there,[S14] along with manufacturing site scaling efforts poised to enhance product availability.State-level initiatives also aim at penetrating Illinois adult-use markets leveraging single dispensing licenses held.[N1,S14]

However,growth is capped by fluctuating local policy run-rates,state-mandated ownership limits,and the cost intensiveness of regulatory compliance limiting rapid scalability.Monitoring changes e.g., potential relaxations that may facilitate inter-state logistics or federal rescheduling reform remains imperative.[N1]

Operational and Legal Risks: Litigation and Compliance Costs

Several litigation matters pose material threats including ongoing suits regarding fiduciary misconduct involving investment manager El Capitan resulting initially in claims near $16.5 million but followed by partial recoveries totaling approximately $10.5 million inclusive of real estate asset settlements slated for disposition[S4]. Such cases absorb substantial management bandwidth and drain financial resources.Secondarily,risk exposure arises through product liability concerns connected partly to the ingestion nature of cannabis goods risking lawsuits or recalls even absent fault[S5].

Data security laws like CCPA compound cost burdens relating not only to data privacy enforcement but also reputational effects triggered by any breach incidents further escalating expenditure patterns required for compliance readiness[S6].

Given the overlapping licensing requirements across multiple jurisdictions,Plaenet 13 must perpetually calibrate operations per each state's evolving framework adding layers of administrative burden incurring significant recurring spend possibly compressing margins further[S17,S28,S29].

Key Performance Metrics to Monitor for Investment Decisions

Investors seeking insight into Planet 13’s trajectory should focus on several critical indicators:

- Stabilization or reversal of recent revenue declines signaling improved market traction[N1],

- Traction toward EBITDA margin improvement reflecting better cost control or pricing power,[N1,S3],

- Transitioning operating cash flow back into positive territory implying sustainable underlying profitability,[F1],

- Modulation of capex aligned with organic expansion without liquidity strain,[F1],

- Regulatory developments especially any substantive shifts in federal scheduling status facilitating broader market participation,[S3],

- License accretions or losses particularly within Florida's Medical Marijuana Treatment Center program signaling footprint growth potential,[N1],

- Resolution outcomes regarding outstanding litigation affecting both capital availability and reputational metrics[S4].

These metrics collectively will underpin assessments surrounding long-term viability amid persistent sector-specific headwinds.

This report presents factual analysis grounded exclusively on filings via SEC forms supplemented by recent news items [N1] without offering investment advice or price targets respectively.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments