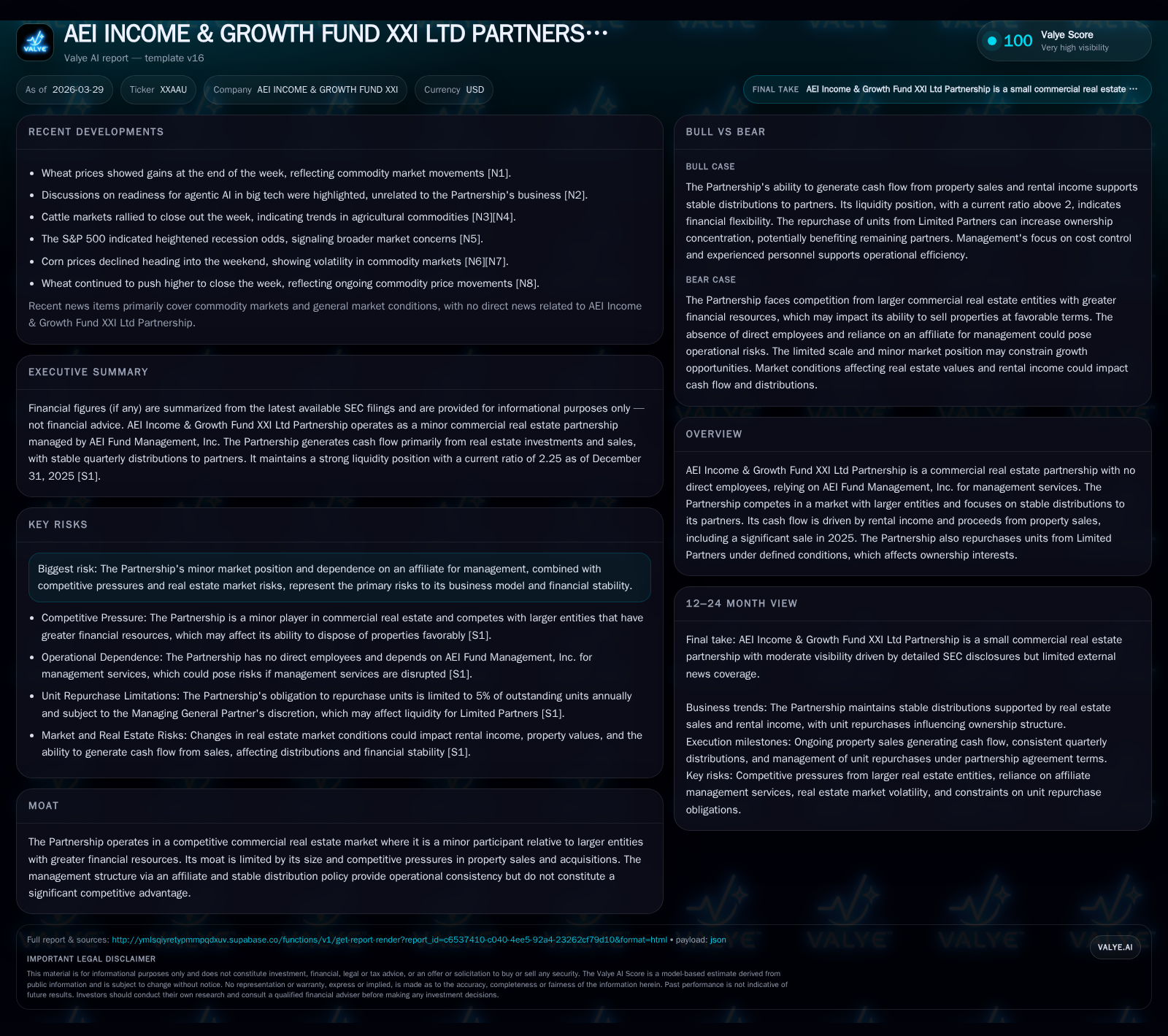

AEI Income & Growth Fund XXI's Modest Scale and Stable Distributions Highlighted by 2025 Property Sale

AEI Income & Growth Fund XXI Ltd Partnership operates as a small commercial real estate partnership reliant on rental income and property sales, with a focus on maintaining stable partner distributions amid competitive pressures.

AEI Income & Growth Fund XXI Ltd Partnership, a minor player in the commercial real estate sector, relies heavily on rental income and proceeds from a significant property sale in 2025 to generate cash flow. Despite shrinking revenue and operating income in 2025, net income surged due to one-time gains from the property sale. The partnership maintains its distribution policy with stable quarterly payouts and employs unit repurchases to increase remaining partners' interests. Operating through an affiliate management company without direct employees, AEI faces competitive market risks attributable to its comparatively small scale.

Overview

AEI Income & Growth Fund XXI Ltd Partnership is a specialized commercial real estate investment vehicle relying on AEI Fund Management, Inc. for operational management services. Notably, the Partnership employs no direct employees and focuses on generating stable distributions for its partners primarily through rental revenues and occasional property dispositions. In January 2025, it executed a pivotal transaction by selling its 40% interest in the Jared Jewelry property located in Auburn Hills, Michigan.

Historical Financial Performance

The Partnership's financial profile reveals steady revenue generation predominantly derived from rental properties; however, top-line figures have declined slightly due to market dynamics and asset sales. The following table summarizes key financial metrics for fiscal years ended 2022 through 2025:

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 896248 | 1059863 | 708715 | 221632 | -10.4% | +307.0% |

| 2024 | 999825 | 260390 | 752432 | 256567 | +0.2% | +7.7% |

| 2023 | 997334 | 241882 | 678624 | 238743 | +23.6% | -84.2% |

| 2022 | 807075 | 1531185 | 816752 | 260589 |

Source: SEC companyfacts cache [F1].

Note: Buyback volumes reflect units exchanged rather than dollar amounts except for limited data from SEC filings which notes repurchase costs.

Revenue peaked around FY24 before retreating due partly to the absence of property acquisitions and stable leasing yields. Operating income has followed this lower trajectory aligned with slight margin contraction. However, net income shows volatile swings influenced prominently by non-recurring gains—most notably a substantial capital gain recognized upon the March 2025 sale of the Auburn Hills property yielding net proceeds of $1.35 million and a book gain exceeding $825K [S1][S3][S4]. Cash flow from operations remains positive yet marginally softer in absolute terms.

Distributions declared consistently rose from $693K in FY24 to $872K in FY25 as the Partnership maintains a policy geared toward stability and reflects improved cash availability post-sale [S6]. Concurrently, share repurchases were initiated for the first time in FY25 at scale — approximately over one thousand units acquired across two tender offers — increasing residual ownership concentration [S2][S9].

Growth Prospects and Constraints

Future growth opportunities for AEI Income & Growth Fund XXI appear inherently modest given its described status as a "minor factor" within a highly competitive commercial real estate market dominated by larger firms with deeper capitalization [S1][S16]. The absence of direct employee personnel internally places execution reliance squarely on AEI Fund Management's affiliate resources — itself having trimmed headcount recently [S1].

The intrinsic growth drivers hinge primarily on continuing rent collection from existing assets alongside selective property dispositions that enable capital recycling into either buybacks or new investments when strategically justified [S6][S2]. However, the partnership agreement restricts annual unit repurchases to no more than five percent of outstanding units at January each year and caps obligation based on capital preservation criteria determined by managing general partners [S1][S9], thereby tempering aggressive capital return strategies.

Key Forecasts and Milestones

AEI has not provided formal forward guidance beyond reaffirming its commitment to stable distributions paid quarterly shortly after each period end [S1][S6]. Investors should monitor announced property sales or acquisitions as inflection points that may influence cash flow profiles along with quarterly distribution declarations signaling operational stability.

The ongoing capability to repurchase tendered Units at discounts remains an important tactical lever influencing partner ownership dynamics while potentially enhancing per-unit distributions over time.

Capital Allocation and Returns

Examining returns requires parsing limited data: explicit ROE is undisclosed; however notable is that net income far exceeded operating profits in FY25 due chiefly to asset sale gains rather than recurring operations [F1]. This episodic profitability spike underscores sensitivity regarding sustainable earnings power.

Operating cash flow consistently generates mid-to-high six-figure inflows annually supporting distribution payments above $800K most recently and providing liquidity for unit repurchases totaling $794K in FY25 [S3][F1]. No dividends are declared separate from these distributions.

Capital deployment has prioritized returning value directly to partners via distributions combined with opportunistic unit repurchase programs which began only recently [S6]. The latter strategy incrementally raises ownership percentages among remaining unit holders potentially enhancing intrinsic value absent major portfolio expansion.

Importantly, there are no material off-balance sheet liabilities which suggests conservative risk exposure levels relative to sector counterparts [S3][S8].

Industry Context Analysis

Although AEI operates outside major concentrated institutional platforms possessing multi-billion dollar asset pools and vertically integrated leasing-management arms common among leading REITs or private equity funds focused on commercial real estate, it exploits niche stability via consistent landlord roles and disciplined capital recycling—a typical posture for smaller partnerships lacking scale advantages.

The commercial real estate market’s cyclical nature poses infusion risk especially linked to broader macroeconomic shifts impacting tenant demand or financing costs—a factor AEI presumably mitigates somewhat by conservative leverage levels implied but unstated explicitly here [F1],[S3],[S4]. With no substantial employee base nor direct developmental initiatives documented, growth is unlikely through portfolio expansion absent external capital injection or mergers.

Risks Summary

Key risks acknowledged center around competitive disadvantages tied to size relative to larger peers competing vigorously for both buyers when divesting assets and tenants when investing capital anew. Dependency on an affiliated management company creates potential agency risks though mitigated somewhat by experienced personnel and standardized conduct codes mandated throughout management staff [S1][S16]. Consistent quarterly distribution policies constrain flexibility during downturns but enhance predictability for investors.

No legal proceedings currently impact operations supporting a clean regulatory standing as per disclosures through early-2026 filings [S7].

Conclusion

AEI Income & Growth Fund XXI Ltd Partnership functions modestly within the commercial real estate landscape focusing on generating reliable rental income supplemented by occasional strategic asset sales exemplified by its sizable gain in early-2025. While revenue trends reflect some contraction alongside falling operating profits compared with recent highs—net income gains via property sales buoy overall results significantly.

The Partnership’s capital allocation principle balances stable distributions alongside measured buybacks restricted by contractual limits ensuring maintenance of capital adequacy.

Despite competitive constraints rooted in smaller size and externalized management dependencies limiting rapid growth potential or market influence, the fund emphasizes continuity coupled with tactical portfolio adjustments aimed at sustaining partner returns over time.

Disclaimer: This report is prepared solely for informational purposes without any recommendation or investment advice concerning securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments