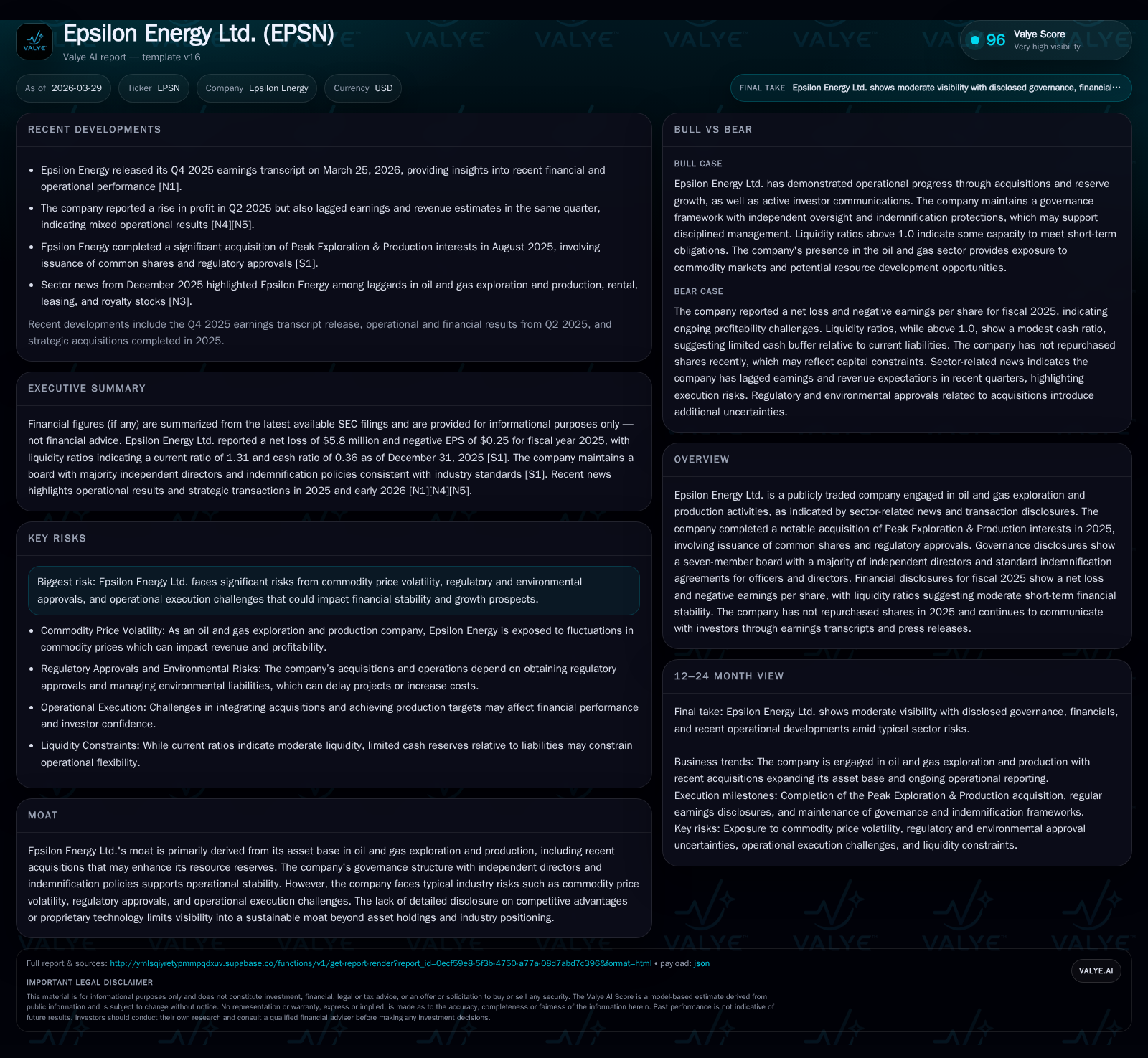

Epsilon Energy’s Asset Expansion and Profitability Challenges in 2025

The 2025 fiscal year marked a pivotal period for Epsilon Energy Ltd., characterized by significant asset growth via acquisition but offset by steep operating losses and liquidity balancing.

Epsilon Energy Ltd.’s 2025 financial results reveal a stark profitability reversal despite expanding its asset base through the acquisition of Peak Exploration & Production interests. The company reported a sharp operating income decline of over 400% year-over-year, resulting in sizeable net losses. Nevertheless, operating cash flows increased by more than 22%, supported by reserve-based lending secured through a new $47.5 million credit facility. Governance strength and recent board additions underpin the strategic transition, though commodity price volatility and regulatory complexities pose ongoing risks. Capital allocation disciplined by negative returns and an absence of share repurchases mark a cautious approach to balancing growth with financial stability.

Historical Performance Highlights: From Profit to Operating Loss

Epsilon Energy Ltd. experienced a dramatic shift in its financial performance in fiscal year 2025 compared to the preceding three years. Operating income deteriorated sharply from positive $3.4 million in FY2024 to a loss of approximately $10.5 million in FY2025—representing a year-over-year decline exceeding 400% [F1]. Correspondingly, net income swung from a profit of nearly $1.9 million in FY2024 to a loss approaching $5.8 million in FY2025, mirroring the operating income trajectory.

Interestingly, the company's operating cash flow (CFO) showed resilience amid the accounting loss environment, increasing by over 22% year-over-year to roughly $20.6 million in FY2025 [F1]. This divergence suggests strong underlying cash generation from core upstream operations despite non-cash charges or integration costs impacting net earnings.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -6 | 21 | -11 | -400.8% |

| 2024 | 2 | 17 | 3 | -72.2% |

| 2023 | 7 | 18 | 5 | -80.4% |

| 2022 | 35 | 38 | 47 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | -4.6 |

| 2024 | 2 | 2.0 |

| 2023 | 6 | 6.9 |

| 2022 | 6 | 33.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is insufficiently available for annual comparisons.

Impact of the Peak Exploration Acquisition on Asset Base and Financials

In November 2025, Epsilon Energy consummated the acquisition of interests from Peak Exploration & Production LLC as well as Peak BLM Lease LLC [S21]. The purchase consideration involved issuing over five million common shares along with contingent shares subject to subsequent regulatory approvals [S20][S25]. Strategically, this transaction aimed at expanding the company's reserve-backed asset base in U.S. upstream oil and gas operations.

While this acquisition broadens Epsilon’s resource holdings, it also introduced integration complexities that likely contributed to the notable deterioration in operating profitability seen in FY2025. The timing late within the fiscal year implies limited contribution toward full-year earnings but likely elevated expenses related to transaction costs and initial consolidation activities.

Regulatory approvals including environmental and title reviews remain key conditions tied with the acquisition agreements adding near-term uncertainty [S24]. Shareholder authorization was secured to allow issuance of consideration shares per NASDAQ requirements evidencing governance diligence surrounding this transaction [S21].

Liquidity and Capital Structure: New Credit Facility Terms Amid Growth

In parallel with its acquisition strategy, Epsilon Energy arranged a new senior secured reserve-based revolving credit facility totaling $47.5 million as of October 2025 [S4][S6]. This facility replaces a predecessor line and extends maturity to October 2029 with co-borrowers including Epsilon USA Inc.

Key credit terms include interest tied to the three-month SOFR index plus a margin ranging from three to four percent depending on utilization levels [S4]. Borrowing capacity is subject to semiannual redetermination updates capturing changes in reserve valuations — standard practice in upstream finance managing borrowing base leverage ratios linked directly to proved oil and gas assets.

As of year-end liquidity metrics indicate moderate short-term stability: a current ratio near 1.31 derived from current assets of approximately $32.6 million versus current liabilities around $24.9 million [F1]. Cash and equivalents alone stood at about $9 million [F1], supporting working capital needs while maintaining flexibility for ongoing investment or debt servicing.

Risks from Commodity Volatility and Regulatory Hurdles

As typical for exploration and production companies like Epsilon Energy, exposures to commodity price volatility present material downside risk to margins and cash flows [S7][S9]. The absence of detailed hedging strategies disclosed amplifies sensitivity to unpredictable energy markets.

Additionally, regulatory compliance burdens including environmental approvals can delay project timelines post-acquisition or impede reserve development plans [S7][S10]. The company faces "reserve replacement risk" inherent in upstream operators needing continual capital reinvestment to maintain production profiles.

Operational execution challenges linked with integrating acquired assets introduce potential cost overruns or deferments which could exacerbate profitability pressures noted in recent financial results.

Governance Quality as a Foundation for Stability

Epsilon Energy maintains governance standards aligning with NASDAQ listing rules featuring a seven-member Board composed predominantly (>50%) of independent directors [S1]. Independent members such as John Lovoi and Nicola Maddox contribute diverse sector experience critical for overseeing strategic transactions like the Peak acquisition.

Indemnification provisions under Alberta Business Corporations Act protect directors/officers against liabilities incurred acting honestly and in good faith on company behalf [S1][S6][S7]. These protections facilitate prudent decision-making necessary during phases of organizational transformation while limiting personal risk for board members.

The governance framework provides an essential bulwark against execution risks and ensures shareholder interests receive vigilant oversight during this expansion phase.

Capital Allocation Review: Cash Flows, Dividends, and Share Repurchases

Despite net losses recorded in FY2025 operating cash flows grew substantially (+22.5%) reflecting robust resource cash generation net of working capital effects [F1]. Yet return on equity suffered at approximately -4.6%, signaling capital productivity struggles amid profitability setbacks [F1].

No dividends were declared or paid throughout fiscal year 2025 consistent with preserving capital flexibility amid industry cyclicality and acquisition-related expenditures [S3][S8]. Share repurchases halted completely after modest buybacks totaling around $1.8 million in prior year FY2024 contrasted against higher historical activity above $6 million annually earlier [F1][S16].

This cautious deployment suggests management prioritizes debt repayment capacity or reinvestment into projects over shareholder distributions given the challenging earnings environment.

Outlook: Operational Milestones to Watch Post-Acquisition

Looking forward progress metrics worth monitoring include semiannual borrowing base redeterminations which will reflect operational performance of newly acquired assets under varying commodity price cycles [N1]. Integration milestones such as streamlining operational synergies or completing regulatory approval steps will be critical signals for reversing recent profitability trends.

Management commentary highlights focus on increasing production rates at Peak assets alongside maintaining strict discipline on project economics amidst volatile oil prices [N1]. Achieving operational break-even pricing thresholds remains pivotal for restoring sustainable earnings trajectories.

Navigating these dynamics requires balancing capital preservation with opportunistic growth investments aligned with evolving market conditions — an enduring challenge for mid-cap independents like Epsilon Energy.

This report is prepared solely for informational purposes based on publicly available data extracted from SEC filings and company disclosures as of March 29, 2026. It does not constitute investment advice or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments