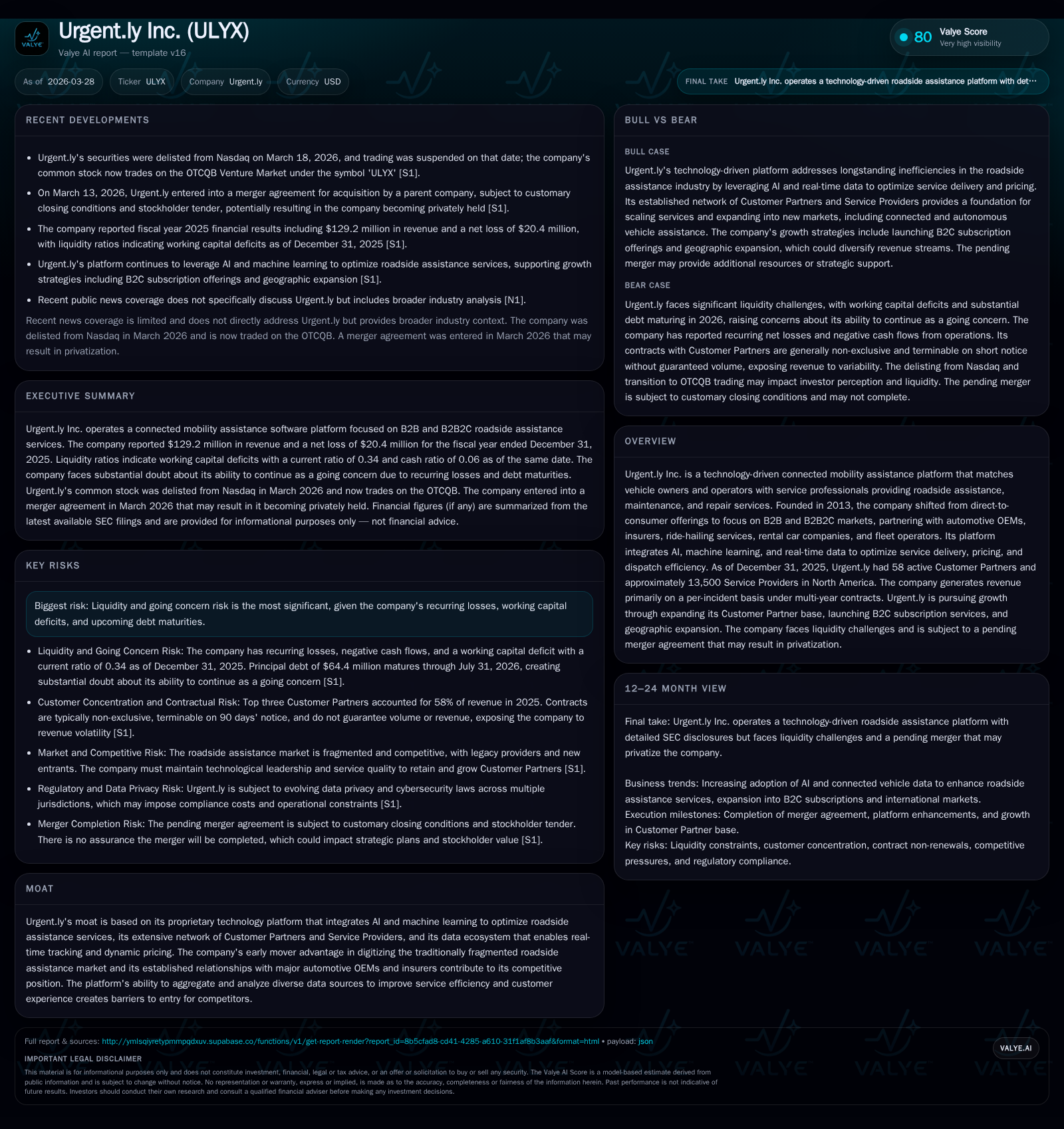

Urgent.ly Inc.: Market Leadership Amid Financial and Liquidity Challenges

Urgent.ly leverages advanced technology in roadside assistance with a strong enterprise footprint but faces significant liquidity constraints and near-term debt maturities.

Urgent.ly Inc. has transformed from a direct-to-consumer roadside assistance platform to a leading B2B/B2B2C provider serving major automotive OEMs, insurers, and fleet operators in North America. Its proprietary AI-driven platform optimizes dispatching and pricing, supporting a network of over 13,500 service providers. Despite gross margin improvements and reduced operating losses in 2025, the company experienced a nearly 10% revenue decline and continues to face working capital deficits, substantial debt of approximately $64 million maturing in 2026, and repeated covenant waivers, raising material going concern considerations.

Evolution from Direct-to-Consumer to Enterprise-Focused Mobility Assistance

Founded in 2013, Urgent.ly initially provided a digital platform allowing individual drivers direct access to roadside assistance services. The company quickly shifted its focus toward business-to-business (B2B) and business-to-business-to-consumer (B2B2C) models by partnering with original equipment manufacturers (OEMs), insurance companies, ride-hailing services, rental car companies, and fleet operators [S1]. This strategic pivot positioned Urgent.ly as a white-label or co-branded software provider enabling Customer Partners to offer seamless roadside assistance integrated within their broader mobility services.

As of December 31, 2025, Urgent.ly's ecosystem encompassed roughly 58 Customer Partners alongside approximately 13,500 contracted Service Providers across North America [S1]. These enterprise relationships underpin scalable growth through long-term contracts rather than relying on individual consumer transactions.

Financial Performance Overview Through Fiscal Year 2025

Urgent.ly's revenues declined from $184.7 million in FY2023 to $129.2 million in FY2025—a cumulative reduction influenced by industry competition and the post-merger integration with Otonomo Technologies Ltd. [F1]. Despite this contraction (9.6% year-over-year decrease in 2025), operating losses narrowed significantly from -$46.1 million in FY2023 to -$8.9 million in FY2025 due to cost rationalization efforts.

Net losses also improved markedly year-over-year from -$44.0 million in FY2024 to -$20.4 million in FY2025 [F1]. Operating cash flow losses decreased substantially from -$30.8 million to -$7.4 million over the same period.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 129 | -20 | -7 | -9 | -9.6% | +53.6% |

| 2024 | 143 | -44 | -31 | -27 | -22.6% | -158.9% |

| 2023 | 185 | 75 | -65 | -46 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 44.0 |

| 2024 | 139.0 |

| 2023 | 778.1 |

Source: SEC companyfacts cache [F1].

Table: Historical annual financial performance highlighting revenue decline alongside improving operating efficiency.

Higher revenue per dispatch driven by dynamic pricing strategies helped boost gross profit despite lower transaction volumes [S10].

Technological Edge: AI-Driven Dispatching and Platform Integration

Urgent.ly’s platform integrates artificial intelligence and machine learning algorithms that optimize roadside assistance operations by dynamically pricing services based on supply-demand conditions and intelligently dispatching appropriate Service Providers for timely responses [S1][S14][S21].

The platform supports a broad network of mostly small-to-medium-sized service providers managing multiple contracts, enhancing utilization rates while maintaining high customer satisfaction scores averaging around 4.6 out of 5 stars during 2025 [S1]. It also offers SaaS-based white-label solutions embedded within Customer Partner portals, facilitating broad reach without direct consumer marketing expenditures.

Real-time telematics data aggregation enables location tracking and predictive maintenance triggers—capabilities that differentiate Urgent.ly’s offer from traditional roadside assistance providers.

Operational Optimization Amid Revenue Decline

In fiscal year 2025, Urgent.ly implemented significant cost reductions post-Otonomo merger:

- Research & Development expenses dropped by approximately 48%, largely through eliminating overlapping efforts while focusing on core AI capabilities [S10].

- Sales & Marketing expenses fell by about half as outreach emphasized enterprise partner management over broad consumer acquisition [S10].

- Operations & Support costs decreased roughly by one quarter due to process automation and workforce adjustments [S10].

These measures contributed to an increase in gross margin from around 22% in FY2024 to about 25% in FY2025 despite decreasing overall volumes [S10][F1]. Operating losses were reduced accordingly.

Liquidity Constraints and Debt Maturity Risks

Urgent.ly’s balance sheet exhibits notable liquidity challenges:

- Current assets totaled approximately $30.6 million against current liabilities near $90 million at December 31, 2025, yielding a current ratio of about 0.34—indicating working capital pressure caused by faster payments to Service Providers relative to collections from Customer Partners [F1][S4][S5].

- Total debt amounted to roughly $64.4 million with maturities scheduled between July and November of 2026 across secured term loans and revolving credit facilities [F1][S4].

- The company has obtained multiple covenant amendments temporarily lowering minimum liquidity requirements from $5 million to $2 million amidst refinancing challenges [S6][S7][S20].

- Auditors expressed substantial doubt regarding Urgent.ly’s ability to continue as a going concern absent successful restructuring or capital raises [S7].

- Interest rates on term loans approximate or exceed 13%, increasing financing costs [S5][S21].

Together these factors underscore significant refinancing needs coupled with ongoing cash flow pressures.

Capital Allocation Focused on Technology Investment Amid Negative Free Cash Flow

Operating cash flow improved but remained negative at approximately -$7.4 million for FY2025 compared with prior years; estimated free cash flow remains negative near -$7.45 million after capital expenditures predominantly directed toward internal software development projects enhancing automation capabilities critical for scaling integrations efficiently without proportional headcount increases [F1][S10][S13][S15].

No dividends or share repurchases are planned as the company prioritizes liquidity preservation amidst net losses.

Outlook: Growth Opportunities Tempered by Market Risks and Capital Limitations

Management aims to grow via expanding its Customer Partner base beyond roughly 58 active contracts across OEMs, insurers, fleets, and emerging mobility platforms as well as by developing B2C subscription offerings complementing its core B2B model [N1][S1].

However:

- Many large Customer Partners retain termination rights on short notice without guaranteed volume commitments posing revenue volatility risks [S23].

- Competition from better-capitalized incumbents or new entrants may erode market share given low barriers among fragmented service providers [S21].

- Capital access constraints limit flexibility for strategic investments or weathering demand fluctuations despite the company's technological advantages.

- Legal and regulatory risks including cybersecurity compliance and evolving tax laws could impose additional burdens [S12][S16][S29].

Key Performance Indicators for Stakeholders Monitoring Trajectory

Critical metrics include:

- Monthly dispatch volumes reflecting service engagement trends relative to partner expansion goals.

- Consumer Satisfaction Scores maintaining industry-leading levels (~4.6/5).

- Renewal rates of long-term agreements with top-tier Customer Partners signaling revenue stability.

- Uptake levels of newly introduced B2C subscription products outside core enterprise channels.

- Quarterly liquidity disclosures detailing cash reserves versus upcoming maturities indicating refinancing prospects or distress signals.

Tracking these KPIs will clarify whether operational improvements translate into sustainable financial health amid structural debt obligations.

Disclaimer: This analysis is based solely on publicly available information as of March 28, 2026 ([F1],[S#],[N#]) without investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments