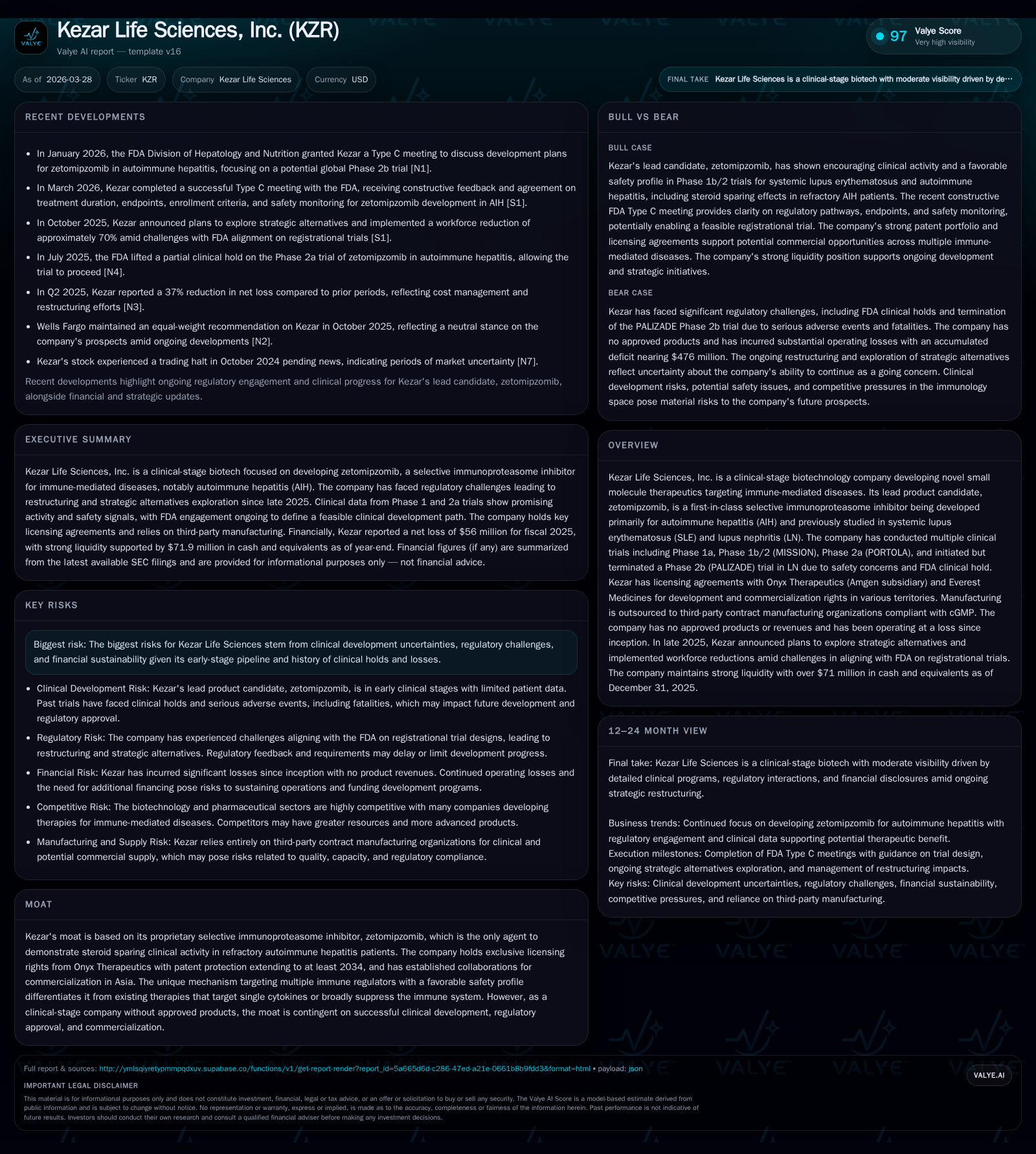

Kezar Life Sciences Charts Path Forward After Strategic Reset in Autoimmune Therapy

Kezar Life Sciences is recalibrating its zetomipzomib development amid FDA feedback and financial pressures while emphasizing focused clinical execution.

Kezar Life Sciences, a clinical-stage biotech focused on selective immunoproteasome inhibition, has faced significant regulatory and clinical trial hurdles, including an FDA clinical hold that halted its Phase 2b lupus nephritis trial. The company is now pursuing a strategic reset centered exclusively on zetomipzomib for autoimmune hepatitis, leveraging constructive FDA Type C meeting guidance to design feasible Phase 2b studies. Financially, Kezar’s losses are narrowing but remain substantial, with cash reserves offering runway through at least 12 months. The company’s ability to optimize its proprietary immunoproteasome asset, manage clinical and regulatory risks, and secure additional capital will be critical to sustaining its early-stage biotech trajectory.

Historical Financial Performance and Operational Trajectory

From fiscal year 2022 through 2025, Kezar Life Sciences has shown notable progress in reducing its operating losses although it remains far from profitability. Operating income improved from a negative $71.2 million in FY2022 to $-59.1 million in FY2025, a year-over-year improvement of nearly 35% indicating measured efficiency gains or cost containment [F1]. Net income followed a similar pattern declining from a loss of $68.2 million in FY2022 to $56 million in FY2025. Operating cash flow outflows have been consistently negative reflecting the capital-intensive nature of clinical-stage R&D activities—FY2025 saw $51.8 million outflow despite a steep reduction relative to prior years. Capital expenditures reduced sharply after FY2023 with only $8 thousand spent in FY2025 versus nearly $1.8 million previously.

This relentless cash burn underpins the company's reliance on external financing strategies and operational restructuring efforts that culminated in workforce reductions and portfolio narrowing announced during late 2025 [S1,S17]. Shareholder equity decreased significantly from $270 million (FY2022) to just over $70 million (FY2025), consistent with ongoing operating losses that yield an approximate return on equity of -80%. Kezar has not engaged in dividends or share buybacks which is typical for early-stage biotechs prioritizing capital preservation for R&D.[F1]

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -56 | -52 | -59 | 8000 | +33.1% |

| 2024 | -84 | -74 | -91 | 29000 | +17.8% |

| 2023 | -102 | -82 | -111 | 1810000 | -49.3% |

| 2022 | -68 | -59 | -71 | 1578000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -52 | -80.0 |

| 2024 | 0 | -74 | -71.6 |

| 2023 | 0 | -83 | -54.3 |

| 2022 | 0 | -60 | -25.3 |

Source: SEC companyfacts cache [F1].

Zetomipzomib: Clinical Development Journey and Regulatory Interactions

Kezar's lead asset zetomipzomib represents an innovative approach via selective immunoproteasome inhibition targeting immune-mediated diseases like autoimmune hepatitis (AIH). This small molecule uniquely modulates multiple immune regulators rather than individual cytokine targets typical of existing therapies . Its clinical profile includes steroid sparing effects observed in refractory AIH patients intolerant or unresponsive to standard care—a key differentiator seeking regulatory validation.

The company advanced zetomipzomib through several clinical trials: Phase 1a/b/2 MISSION study exploring safety/tolerability; Phase 2a PORTOLA study focused on AIH efficacy; however its Phase 2b PALIZADE lupus nephritis trial was abruptly terminated following FDA safety concerns leading to a clinical hold [S1]. These events exposed intrinsic developmental risks endemic to immunomodulatory agents where pharmacovigilance is critical.

In early 2026 Kezar successfully completed a Type C meeting with the FDA Division of Hepatology and Nutrition where regulatory authorities provided constructive guidance concerning trial design parameters for a new global randomized Phase 2b AIH study. Protocol agreement was reached on treatment duration aligned with intended endpoints and enrollment criteria refined for patient population homogeneity. Importantly safety monitoring requirements were relaxed substantially—from initially mandated continuous inpatient monitoring over 48 hours to more pragmatic monitoring protocols—enhancing trial operational feasibility while addressing risk mitigation [S1,S3].

Strategic Rationales Behind Portfolio Restructuring and Asset Divestitures

Confronted by constrained resources and mounting operating losses exceeding $50 million annually [F1], Kezar moved decisively to shutter its Sec61-based oncology program represented by KZR-261 after preliminary Phase 1 data failed to justify continued investment [S3]. This strategic divestiture concluded with an asset purchase agreement signed March 6th, 2026 transferring all Sec61 intellectual property rights to Enodia Therapeutics [S3].

This divestment allows Kezar management to sharply focus limited R&D funding toward advancing zetomipzomib's challenging clinical path with the prospect of crafting shareholder value around a flagship immunoproteasome candidate. While this increases pipeline concentration risk typical among emerging biotechs it reflects a pragmatic tradeoff favoring resource allocation within cash constraints exacerbated by regulatory delays.

Path Forward: Upcoming Clinical Milestones and Regulatory Strategy

Though publicly disclosed updates are sparse beyond the recent FDA meeting outcomes [S1], one should monitor initiation timelines for the proposed global randomized Phase 2b AIH trial as per FDA alignment—enrollment speed will be critical given past difficulties recruiting rare autoimmune disease patients documented during previous studies .

Key milestones will include finalization of protocol based on agreed endpoints emphasizing steroid sparing efficacy measures alongside safety outcomes tailored per the updated FDA risk-mitigation framework facilitating outpatient monitoring protocols likely essential for enrollment feasibility.

Analysts should watch closely any signals arising from upcoming pre-ind or IND-enabling communications as well as additional pharmacokinetic hepatic impairment studies recently proposed by Kezar—both integral components supporting registrational intent study design scalability.[S1]

Capital Structure, Cash Runway, and Capital Allocation Policies

As of December 31st 2025 Kezar reported cash and cash equivalents of approximately $71.9 million underpinning robust liquidity illustrated by a current ratio exceeding 11x—a buffer sufficient for near-term operational funding excluding substantial unexpected costs [F1].

Notably the company fully repaid its outstanding term loans totaling around $6.3 million in October 2025 releasing pledged asset liens attached under the previous loan agreements thereby reducing interest expenses which had been modest—approximately $0.3 million quarterly prior—and improving financial flexibility [S4,S6,S8,S14].

Kezar maintains no dividend payments nor share repurchases consistent with typical biotech capital allocation rationales that prioritize funding clinical development activities above shareholder distributions owing to high reinvestment needs and uncertain timelines [F1,S20]. Conservatively managing burn rate post-restructuring coupled with divestiture proceeds partially supports planned future investments though further equity or partnership financings remain probable.

Risks: Clinical, Regulatory, and Financial Challenges Ahead

Clinical development hazards constitute foremost risks: inability to recruit adequate patient cohorts timely could delay studies indefinitely; adverse safety events may prompt renewed regulatory holds derailing progress; incomplete pharmacovigilance capacity heightens exposure especially given previous concerns prompting trial aborts [S1,S5,S10].

Regulatory complexity amplifies risk—strict adherence not only to FDA clinical mandates but also evolving healthcare fraud/abuse laws plus data privacy regulations increase compliance costs substantially while potential penalties pose financial strain if violations occur inadvertently [S10,S11]. Rising product liability insurance premiums further inflate expenditure forecasts prohibitive without successful product commercialization backing.[S5]

From a financial perspective dependence on continued capital infusions introduces dilutionary pressure that can adversely affect shareholders’ stakes while adverse macroeconomic conditions could complicate fundraising timing or valuation terms [S19,S26]. Historically significant operating losses exacerbate concerns about durable path toward profitability impacting market perception negatively.

Assessing Moat Sustainability Through IP, Licensing, and Competitive Positioning

The core of Kezar’s competitive advantage lies within its patent-protected novel small molecule selectively inhibiting the immunoproteasome—a target validated mechanistically yet clinically underexplored compared to blockbuster biologics targeting singular cytokines such as TNF-alpha inhibitors or IL-17 blockers prevalent in autoimmune therapeutics.

Exclusive license rights secured from Onyx Therapeutics grant patent protection extending beyond 2034 creating long-term barriers against generic competition while international licensing agreements notably with Everest Medicines enable broad geographic development reach across Asia’s highly strategic pharma markets enhancing monetization prospects via milestone payments and royalties contingent on success .

However this moat is fragile conditioned upon successful navigation through late-stage clinical trials demonstrating clear safety-efficacy balance plus regulatory approval milestones unlocking value realization; failure at any juncture would erode these advantages swiftly.

This analysis synthesizes disclosed financials from SEC filings alongside management commentary to provide an integrated view without constituting investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments