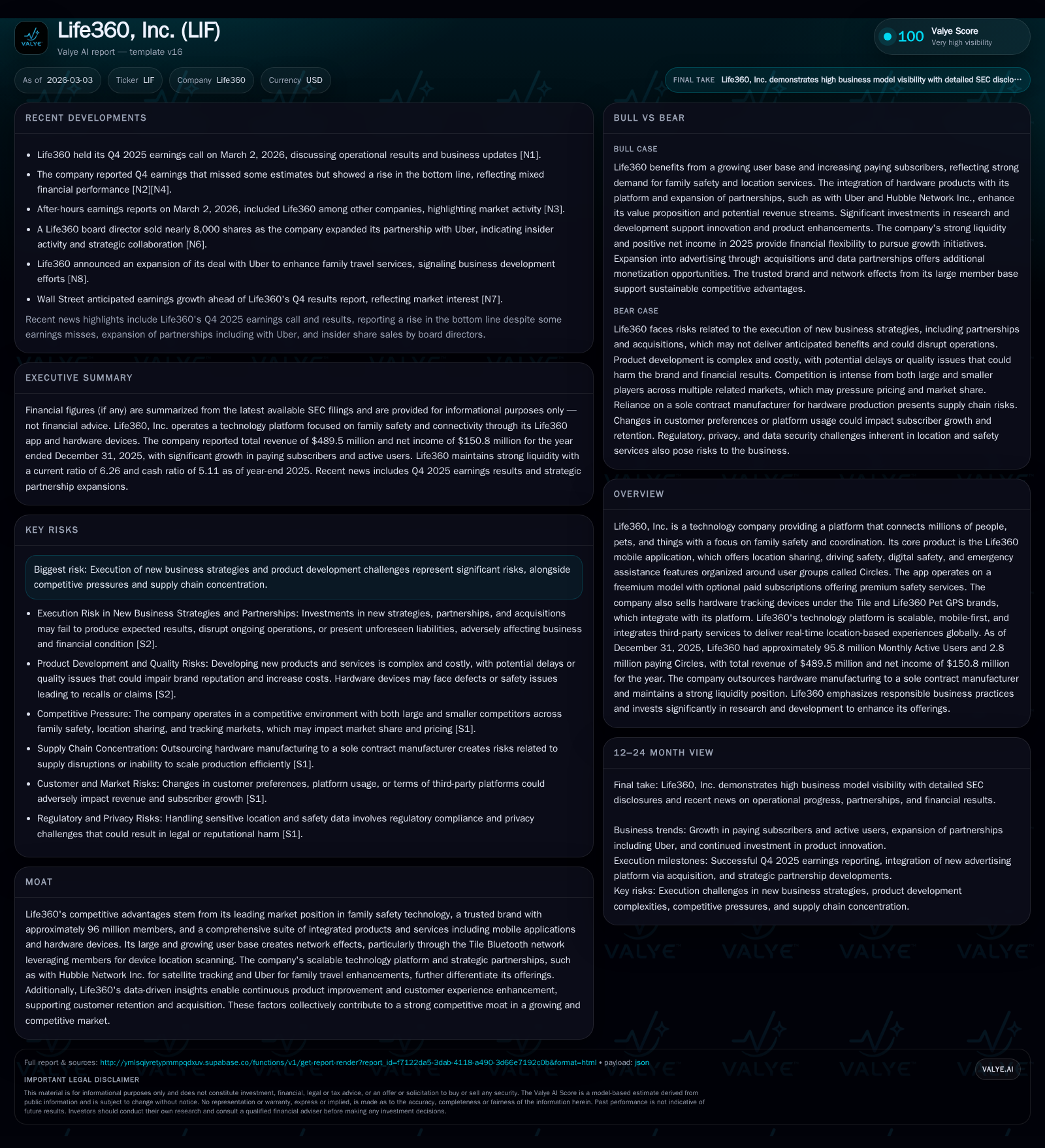

Life360’s Rapid Expansion and Profitability Leap in Family Safety Tech

Analyzing Life360’s impressive financial turnaround driven by subscriber growth, hardware integration, and strategic partnerships.

Life360 transformed from significant multi-year losses into generating robust profits by FY2025, fueled by rapid subscriber expansion and diversification through hardware products like Tile and Pet GPS. Strategic alliances with Uber and Hubble Network support service enhancements and monetization opportunities. Strong cash flow generation and operational leverage underpin solid capital discipline, while risks tied to brand trust, competition, and supply chain concentration remain. Monitoring future member growth, ARPPC trends, and product innovation will be key to sustaining momentum.

From Losses to Profits: Life360’s Historical Growth Trajectory

Life360 has undergone a striking financial evolution over recent years, pivoting from deep operating losses to robust profitability by the close of fiscal year (FY) 2025. Total revenues surged roughly 61% from $304.5 million in 2023 to $489.5 million in 2025 [F1]. Operating income shifted from negative $30 million in 2023 to positive $18.8 million by 2025; net income swung dramatically—from a net loss of $28.2 million in 2023 to net income of $150.8 million in 2025—a year-over-year increase surpassing 3400% [F1]. Operating cash flows (CFO) grew impressively to $88.6 million in 2025 compared with $7.5 million in 2023, underscoring improving underlying cash generation alongside the profit turnaround.

The trajectory reflects substantial gains across subscription revenues complemented by steady contributions from hardware sales and other revenue streams linked to partnerships and data insights [S1]. Capital expenditures remained low—under $2 million for FY25—with a notable increment (+51% YoY), supporting scalability without heavy fixed asset burdens [F1]. The table below summarizes key annual financial metrics:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 151 | 89 | 19 | 1792000 | +3411.4% |

| 2024 | -5 | 33 | -8 | 1187000 | +83.8% |

| 2023 | -28 | 8 | -30 | 506000 | +69.3% |

| 2022 | -92 | -57 | -94 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 87 | 27.5 |

| 2024 | 31 | -1.3 |

| 2023 | 7 | -11.4 |

| 2022 | -57 | -37.5 |

Source: SEC companyfacts cache [F1].

(Source: SEC company filings summary [F1])

Platform Evolution: Drivers Behind Subscriber and Revenue Gains

Central to Life360's rapid revenue expansion is its scalable mobile platform offering family safety services under a freemium model converting free users into paying subscribers organized within 'Circles'—groups defined by users for sharing location and safety data [S1]. At FY25-end, Monthly Active Users neared approximately 95.8 million while paying Circles reached roughly 2.8 million, reflecting YoY growth of about +20% and +26%, respectively—a manifestation of successful user acquisition, retention, and monetization strategies leveraging strong network effects [N1][S1].

Subscription revenue spiked approximately 33% YoY in FY25 reaching nearly $370 million, driven by volume growth plus a ~7% uplift in Average Revenue Per Paying Circle (ARPPC)—attributable to pricing optimizations introduced since mid-2024 alongside enhanced tiered premium features encompassing location coordination, driving safety alerts, digital protection layers, and emergency assistance capabilities [S18][S8].

Continued investment in product innovation fuels member retention; unit economics benefit from efficient acquisition costs amplified by word-of-mouth effects supported by targeted paid marketing spend focused on broader international adoption campaigns [S1]. Maintaining this balance between scale and profitability is critical given the competitive landscape for family-focused tech solutions.

Hardware and Software Synergy: Expanding the Ecosystem with Tile and Pet GPS

Life360's differentiated stance owes partly to its mix of software platforms harmonized with proprietary hardware devices—specifically Tile trackers acquired previously and the newly launched Life360 Pet GPS tracker debuting October 2025 [S1]. Although total hardware revenue dipped marginally (~10%) to roughly $51.8 million due mainly to promotional discounts impacting margins despite a reported +7% increase in shipped units, these devices enhance platform stickiness via real-world applications enabling location monitoring beyond people—extending safety assurance to belongings and pets alike [F1][S9].

The Tile Bluetooth network creates powerful indirect network effects whereby installed devices assist crowd-sourcing location scanning worldwide—forming an expansive mesh increasing device findability beyond individual device range—a feature tough for newer entrants without scaled ecosystems to replicate effectively [S1]. Lower hardware gross margins (~1%) reflect tariff pressures and competitive pricing designed to maximize long-term subscription-driven lifetime value rather than short-run device profitability alone [S10]. This integration exemplifies Life360 as a full-stack safety technology provider.

Strategic Partnerships: Uber and Hubble Collaborations Enhancing Services

Strategic partnerships broaden service value propositions while opening novel monetization vectors. Life360’s agreement with Uber integrates family travel coordination features improving journey safety through granular location insights shared across family Circles during travel—a collaboration extended significantly through early-2026 as publicized recently [N5][N6][S2]. Such integrations aim not just at feature enhancement but deeper engagement driving incremental subscriptions.

Additionally, Life360 inked a technology exclusivity deal with Hubble Network Inc., facilitating satellite-based tracking solutions augmenting existing cellular/GPS coverage—critical for outdoor safety or remote regions where terrestrial networks falter [S2]. This partnership broadens addressable market segments within family safety tied closely with outdoor recreation or emergency response.

Both partnerships operate under revenue sharing frameworks with inherent execution risks surrounding deployment speed and scaling efficacy; nevertheless they represent strategic bets aligning Life360's core competencies around real-time location intelligence augmented by complementary transport or satellite capabilities.

Navigating Risks: Brand Trust, Competition, and Supply Chain Challenges

Life360's moat includes its trusted brand leveraged by nearly 96 million members globally; however that reputation requires ongoing stewardship against privacy/regulatory scrutiny (with continuing regulatory inquiries disclosed) as well as exposure given heightened consumer sensitivity around data protection within geolocation services industries [S1][S7][S29].

Competitive threats are salient particularly on hardware fronts where better-capitalized global firms contest device market shares compelling Life360 to maintain innovation pace amid pricing pressures while optimizing cost structures linked directly to sole contract manufacturing relationships with Jabil based overseas—a concentration risk monitored through supplier diversification efforts though not yet fully mitigated per filings [S4][S11].

Other operational risks encompass execution challenges related to new business strategy rollouts including emerging partnership deals or international expansions where compliance landscapes differ widely causing potential delays or added cost burdens.

Capital Allocation Dynamics: Strong Cash Flow, Minimal Capex, Return on Equity

Financial stewardship is evidenced by operating cash flow generation reaching nearly $88.6 million in FY25 compared with $32.6 million prior year—underscoring leverage benefits derived from scale alongside margin expansions from subscription pricing elasticity [F1][S16]. Capital expenditures remain lean at approximately $1.79 million representing minor investments mostly allocated toward internally developed software projects central for future platform evolution maintaining low fixed asset intensity characteristic for software-first companies.

Equity base expanded aligned with profitability turning positive allowing an estimated return on equity around 27.5%, signaling effective use of shareholder capital alongside a solid current ratio above six evidencing considerable liquidity headroom supporting working capital needs without over-leveraging balance sheet strength [F1][S13][S15]. No dividends or share repurchase programs disclosed indicating reinvestment focus predominates growth initiatives.

Future Outlook: Monitoring Member Growth, Monetization, Product Innovation

Management expects continued Paying Circle expansion powered by sustained member acquisition plus enhancements planned around new subscription tiers targeting broader family life stages beyond core offerings like Kids & Pets monitoring elevating platform relevance across demographic lifecycles [N1][N4][S1].

Incremental ARPPC gains are likely supported by diversified monetization including advertising partnerships yielding rising 'other' revenues surged nearly +90% YoY last cycle reflecting traction from ad placements integrated into platform experiences alongside expanded data analytics sales leveraging anonymized consumer insights under longer-term agreements such as renewed deal extending five years with Placer.ai data partner [F1][S22]. Geographic international expansion remains a watch point as marketing efforts intensify globally demanding careful cost-benefit balancing.

Success factors will include execution effectiveness of technological roadmaps tied closely with partner collaborations like Uber/Hubble plus maintaining brand trust amidst evolving privacy landscapes essential for sustaining subscriber loyalty given growing competition inside family safety tech sector as well as accelerating hardware entrants.

This analysis focuses strictly on publicly filed factual evidence without investment recommendation intent; observed performance milestones highlight Life360’s impressive operational transformation aided by integrated services harnessing subscription scale combined with hardware adjuncts leveraged through strategic partnerships—all while vigilantly managing credit/liquidity profiles amid industry-specific regulatory risks common among location-based consumer technology firms.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments