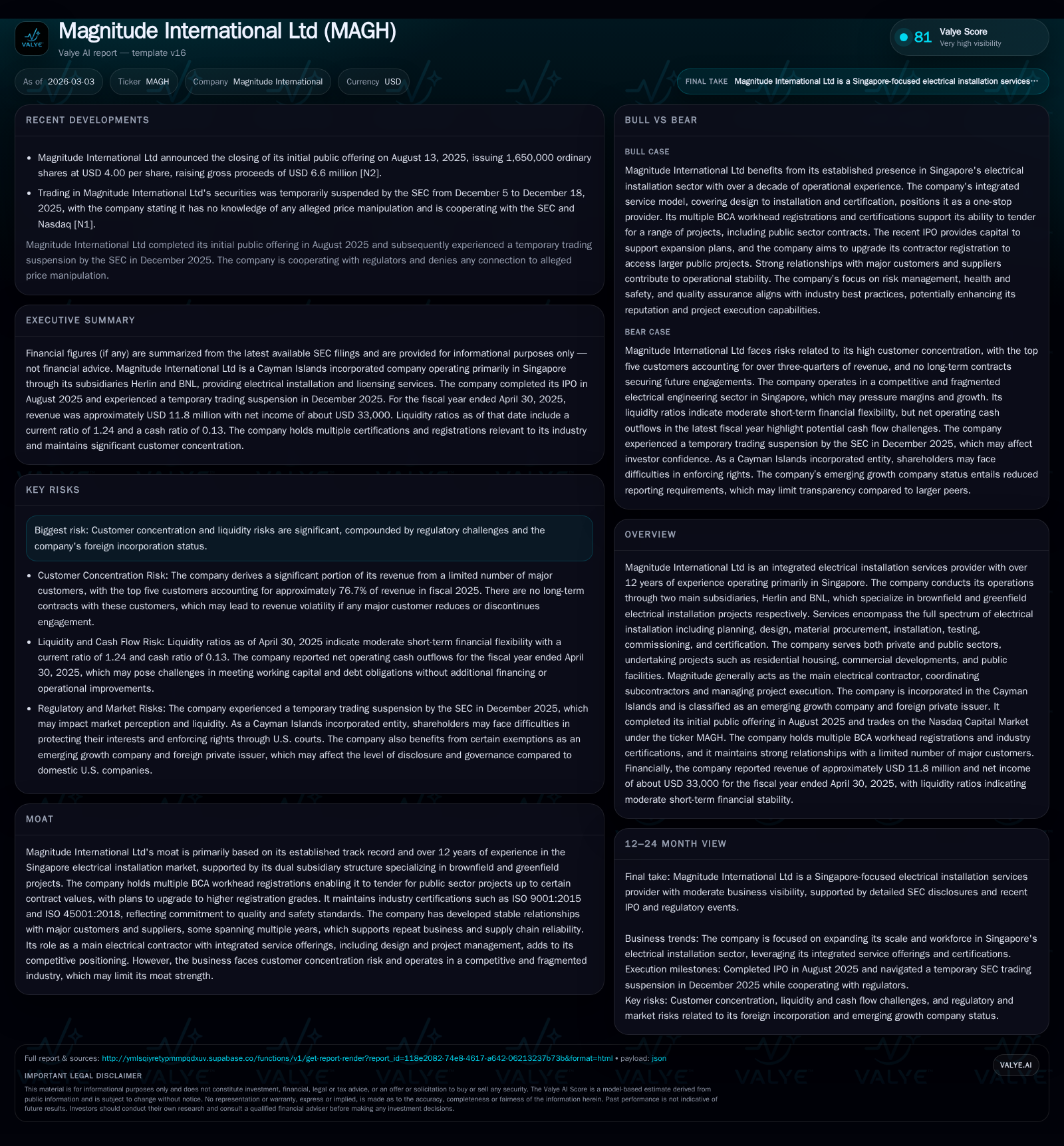

Magnitude International Faces Revenue Decline Amid Customer Concentration and Liquidity Management

The company exhibits significant reliance on a limited customer base, experiencing a revenue drop in FY2025 alongside moderate leverage and working capital pressures.

Magnitude International Ltd, a Singapore-based electrical installation specialist, reported a revenue decrease to approximately USD 11.8 million in FY2025 from USD 18.5 million in FY2024. This decline was driven mainly by reduced greenfield and brownfield project activity. The top five customers accounted for about 77% of revenue in FY2025, reflecting notable client concentration risk. The company maintains liquidity supported by cash holdings of around USD 0.58 million and borrowings near USD 1.79 million, backed by CEO personal guarantees. Operating cash flow turned negative in FY2025 due to upfront project costs and retention payment schedules. Future growth depends on customer diversification and upgrading regulatory certifications to access larger public sector contracts.

Company Overview

Magnitude International Ltd specializes in electrical installation services within Singapore's competitive market. The Group operates primarily through subsidiaries focusing on brownfield (Herlin) and greenfield (BNL) electrical projects, providing comprehensive services encompassing planning, design, procurement, installation, testing, commissioning, and certification mainly for residential developments [S1].

Founded in 2012 by CEO Mr. Lim Say Wei—who personally guarantees certain secured borrowings—the company had around 64 employees as of April 30, 2025 [S1], [S20].

Historical Financial Performance

The table below summarizes key financial metrics over the past three fiscal years ending April 30:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Revenue figures are approximate conversions from SGD where applicable; net income reflects a steep decline despite relatively stable borrowing levels.

In FY2023-24, growth was fueled by increased project activity but offset by rising costs for copper cables and labor which constitute over 80% of costs [S1]. The subsequent FY2025 revenue drop mainly resulted from lower greenfield/brownfield project revenues falling from approximately S$22.8 million to S$11.9 million coupled with a higher proportion of lower-margin ad hoc services.

Net profit correspondingly fell from over S$2 million (USD 1.5 million) to under S$50 thousand (USD 33 thousand), indicating margin compression.

Customer Concentration and Contractual Dynamics

Magnitude’s revenue remains highly concentrated: the top five customers accounted for about 87.9%, 85.5%, and 76.7% of total revenue for fiscal years ending April 30, 2023 through 2025 respectively [S16]. The largest single customer’s contribution declined from roughly 70% in FY2023 to about 31% in FY2025 but still represents a substantial dependency.

Contracts are typically tender-based without long-term agreements; progress payments follow work certification with retention sums withheld up to one year post-completion, constraining immediate cash inflows [S24], [S10].

Liquidity Profile and Capital Structure

Cash and cash equivalents totaled approximately USD 0.58 million as of April 30, 2025 according to filings [F1]. Operating cash flow was negative at around USD -0.69 million that year due to upfront costs for materials procurement and performance bond collateral requirements affecting working capital.

Bank borrowings stood near USD 1.79 million at fiscal year-end bearing fixed and variable interest rates between approximately 2.25% to over 7%, secured by CEO personal guarantees and keyman insurance policy pledges [S11]. Lease liabilities remained steady at roughly USD half a million related primarily to office facilities.

No dividends were declared or paid during FY2025; prior years showed conservative dividend payouts aligned with earnings availability reflecting prudent capital management amidst uncertain growth prospects.

Industry Context and Competitive Positioning

Singapore’s mechanical and electrical contracting sector is highly regulated with over 2,200 registered contractors competing intensely for projects under strict safety standards [S1]. Only a subset hold higher-grade BCA registrations required for large government contracts.

Magnitude currently holds BCA registrations permitting bidding on selected public sector projects below certain value thresholds but aims to upgrade these to compete for larger contracts—a strategic step toward client diversification beyond private residential developments.

ISO certifications such as ISO9001:2015 (quality management) and ISO45001:2018 (occupational health & safety) support operational standards but do not fully offset competitive challenges posed by larger firms with greater resources.

Outlook and Risks

Future growth depends on successful expansion of public sector project bids through upgraded BCA registration status alongside continued efforts to reduce client concentration risk.

Key risks include intense price competition leading to margin pressure; volatility in raw material costs especially copper; working capital constraints due to payment terms; lack of long-term contract visibility; dependence on major customers; and reliance on majority shareholder financial support given personal loan guarantees [S16].

Being incorporated in the Cayman Islands may also pose governance complexities outside Singapore.

Monitoring Points

- Progress on BCA registration upgrades enabling access to higher-value public tenders.

- Diversification beyond top five customers reducing concentration risk.

- Stabilization or improvement in operating cash flow indicating better working capital management.

- Changes in borrowing structures or refinancing activities affecting liquidity flexibility.

- Margin recovery through improved pricing power or reduced reliance on low-margin ad hoc services.

- Regulatory or labor market developments impacting execution costs or timelines.

This analysis is based on data extracted from SEC filings up through March 2026 combined with validated numeric facts without speculative forecasts or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments