Medalist Diversified REIT’s Transition to DST Sponsorship and Taxable Status Challenges Growth and Profitability

The company revoked its REIT status, initiates a DST program to build fee income, while grappling with legacy portfolio pressures and rising financing costs.

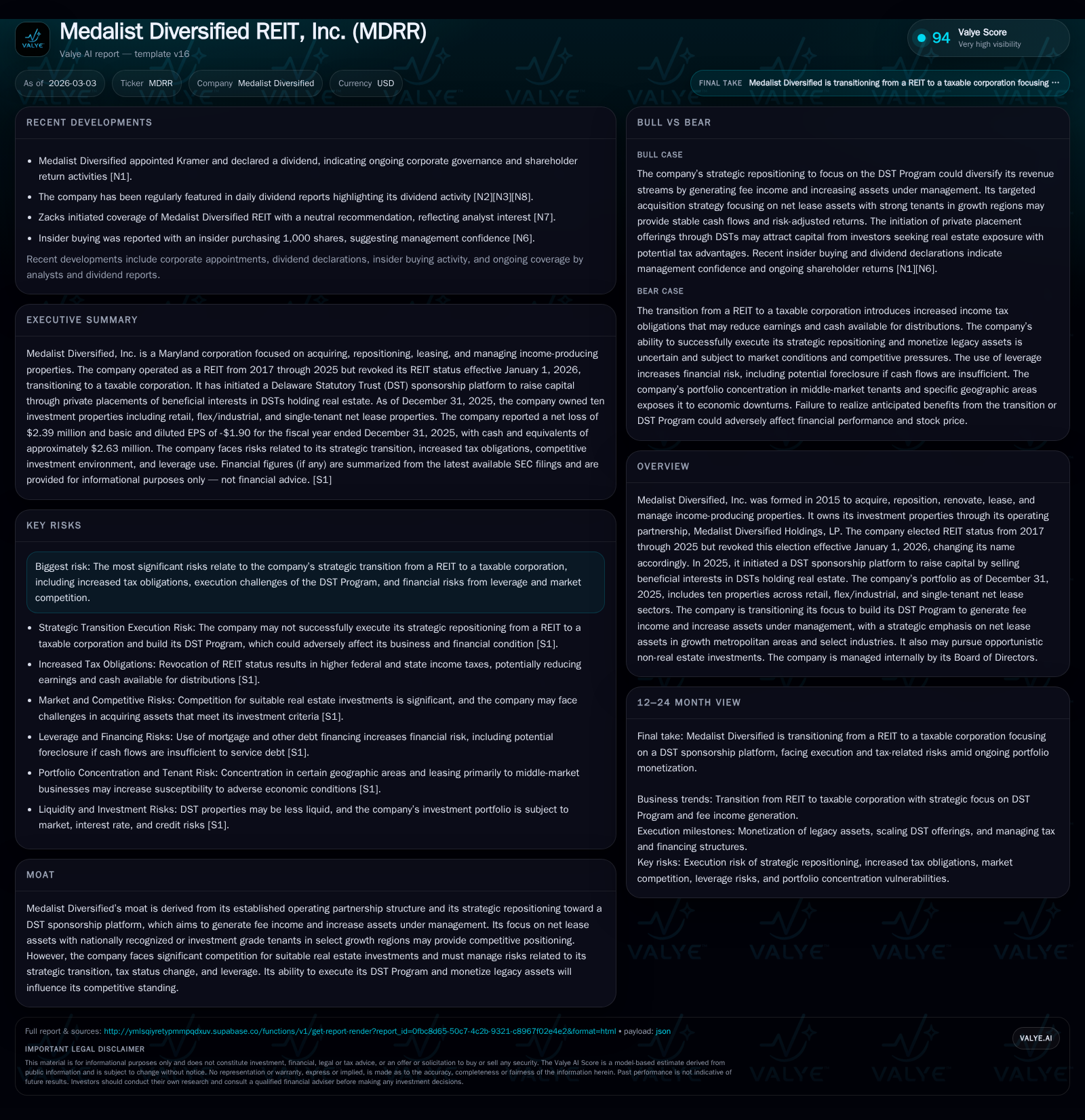

Medalist Diversified REIT, Inc. (MDRR) has undergone a significant strategic shift by revoking its REIT election effective 2026 and focusing on building a Delaware Statutory Trust (DST) sponsorship platform. This transition is aimed at generating recurring fee income and growing assets under management through the sale of DST interests in net lease real estate assets concentrated in select growth markets. However, the company has faced sharply declining operating income and net losses in recent years, reflecting ongoing challenges in repositioning its portfolio, elevated corporate expenses, and increased tax obligations from its loss of REIT status. Financing risks remain elevated due to rising interest rates and leverage which could constrain acquisitions and cash available for distributions. Careful deployment of capital alongside successful monetization of legacy assets will be critical to unlocking value in this evolving business model.

Company Background and Historical Performance

Founded in 2015 as Medalist Diversified REIT, Inc., the company initially positioned itself as a real estate investment trust engaged in acquiring, renovating, leasing, and managing income-producing properties [S1]. Through its operating partnership structure — Medalist Diversified Holdings LP — the company built a small portfolio of ten real estate properties primarily segmented into retail, flex/industrial, and single-tenant net lease (STNL) assets by the end of 2025 [S1][S23].

Between its inception and late 2025, Medalist elected to be taxed as a REIT, an election yielding favorable tax treatment by avoiding corporate income tax if certain requirements are met. However, its historical financials reflect considerable volatility: operating income rose sharply from negative territory in FY2022 (-$1.41m) to approximately $3.7 million in FY2024 before collapsing to just under $0.55 million in FY2025 [F1]. Net losses ballooned heavily over the same period with a -$4.77 million loss in FY2022 narrowing momentarily then widening again markedly to a -$2.39 million loss last year [F1].

Operating cash flow exhibited positive trends but diminished in FY2025 relative to prior years ($1.53m versus $1.80m), illustrating some resilience at the operational level despite profitability challenges [F1]. Capital expenditures have been curtailed significantly — down over 50% compared to prior cycles — possibly signaling asset optimization or reductions consistent with strategic recalibration efforts [F1]. Equity on the balance sheet compressed dramatically starting from over $17 million in FY2022 down to just under $9.43 million last reported [F1].

Table: Medalist Diversified Annual Financial Snapshot

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | 1530751 | 1 | -8779.1% |

| 2024 | 0 | 1796137 | 4 | +100.6% |

| 2023 | -5 | 104013 | -1 | +4.2% |

| 2022 | -5 | 1194626 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($) | ROE% |

|---|---|---|---|

| 2025 | 140788 | -25.3 | |

| 2024 | 32467 | 0.2 | |

| 2023 | 383665 | 286543 | -37.1 |

| 2022 | 1309180 | 286543 | -27.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures were not explicitly disclosed; YoY growth computed when applicable.

Strategic Transition and Future Growth Prospects

In mid-2025 Medalist began a strategic pivot by launching a Delaware Statutory Trust (DST) sponsorship program intended to raise capital through private placements exempt from SEC registration via selling beneficial interests holding real estate investments [S1][S17]. The initial acquisition associated with this initiative was a strategically located Tesla facility in Pensacola contributed into a DST vehicle subsequent to purchase [S1][S17]. This program aims at shifting the company’s revenue base toward recurring fee income derived from increasing assets under management rather than relying solely on property ownership returns.

Effective January 1st, 2026 Medalist formally revoked its REIT election converting into a taxable C Corporation structure [S1][S17]. This transition allows more operational flexibility including pursuing selective asset sales from the legacy portfolio to fund growth capital for the DST program but increases corporate tax obligations materially compared to when it operated as a REIT [S16][S28]. Additionally there are risks surrounding execution timing and market reception which could delay or undermine anticipated benefits.

Going forward the company intends concentrated investments primarily into net lease assets with high-credit or nationally recognized tenants situated in faster-growing US metropolitan regions such as parts of the Southeast states (including Florida), Mountain states and California—known for their demographic expansion and robust commercial activity [S17]. Sectoral emphasis targets retail (likely necessity-based), medical-related facilities which tend to demonstrate resilient demand profiles post-pandemic trends, as well as single-tenant industrial/warehouse properties which parallel broader supply chain logistics growth [S17]. Opportunistic non-real estate investments such as equity stakes or crypto assets also remain within discretional consideration though more limited.

This new focus balances asset management with fee generation but also introduces competition from larger institutional players targeting similar leases/net lease product types along with execution risk inherent to transitioning strategic models and market cyclicality [S24][S22]. Furthermore compounding uncertainty is the still elevated interest rate climate prompting higher debt servicing costs that may constrain acquisition capacity or necessitate larger equity raises dilutive to current shareholders or reduce distributions available [S25][S16].

Capital Allocation & Returns Analysis

Dividend distribution sustainability appears uncertain amid shifting taxation regimes; while historically dividends were paid consistently during earlier years there has been marked retrenchment post-REIT disqualification leading into FY2025 where dividends were not declared explicitly [F1][N1][S26]. Management indicates intent for quarterly dividends based on distributable cash flow but caveats remain around funding from operations vs proceeds from borrowings or equity issuances which may reduce total shareholder return further [S9][S11][S26].

The company has returned capital via share buybacks sporadically though shrinking amounts reflect tight liquidity priorities given operational losses and redeployment toward new DST initiatives [F1]. Return on equity based on latest fiscal year data stands negative near -25%, reflecting recent unprofitability although operating cash flow remains positive supporting cautious optimism for rebalancing financial health if operating conditions stabilize post-transition [F1].

Leverage remains pivotal yet risky: mortgage loans with embedded covenants expose Medalist to potential foreclosures if cash flows falter; interest-only periods inflate balloon maturity risk raising default potential; rising rates amplify expense burdens; lender controls could restrict rental revenue usage upon covenants breach impacting flexibility; "bad boy" carve-out guarantees potentially impose contingent liabilities on defaults complicating debt servicing scenarios further [S4][S6][S7][S8][S12][S16][S19][S25]. Hedging strategies exist but cannot fully shield against volatility given market fragmentation across commercial mortgage markets currently reeling from tighter credit conditions especially for smaller operators [S20][S13].

Risk Profile Summary

Medalist's core risks stem from:

- The operational challenge of successfully executing the pivot out of REIT status including managing elevated tax expenses that compress distributable earnings [S16][S28].

- Liquidity stresses heightened by dependence on timely execution of DST capital raises amid competitive fundraising environments subject to macroeconomic headwinds including inflationary pressures increasing cost structures [S14][S22].

- Market risk related to underlying real estate portfolio concentration primarily within mid-market tenants which are more vulnerable during economic downturns impacting occupancy rates or leasing renewals unfavorable terms limiting rental growth potential [S14]

- Substantial leverage amplifies exposure to rising rate environments increasing refinancing risk including loan covenant breaches triggering lender controls/foreclosure hazards adding pressure on overall financial flexibility [S16][S19]

- Execution risks that DST offerings generate sufficient fee income covering overhead costs while simultaneously liquidating legacy assets without material write-downs or market valuation impairments detrimental to NAV per share metrics affecting investor sentiment [N1][S23]

- Operational dependency on third-party platforms means elevated cybersecurity vulnerabilities potentially disrupting tenant relations or financial systems causing reputational harm and loss of investor confidence [S24]

What To Watch / Milestones

No formal forward guidance has been issued publicly post-transition but key observations include monitoring:

- Progression rate of DST interest sales volumes – performance against private offering targets will indicate success scaling fee income streams.

- Asset disposition velocity and pricing relative to balance sheet carrying values – successful deleveraging coupled with accretive sales would support valuation re-ratings.

- Quarterly operating results tracking reconstitution of profitability post-restructuring measured through improving operating income margins.

- Dividend reinstatement frequency/size aligned with sustained positive distributable cash flow reflecting financial health improvements.

- Leverage ratios trending downward or stable amidst refinancing efforts demonstrating risk mitigation capabilities.

- Credit environment changes affecting borrowing cost stability particularly short term adjustable loans vulnerability exposed by higher interest rates.

Continued scrutiny should also be placed on any regulatory developments influencing DST structures or taxation policies potentially impacting Medalist’s emerging business model profitability beyond current assumptions.

Conclusion

Medalist Diversified’s transformation from a traditional REIT into a taxable corporate entity focused on leveraging its DST sponsorship platform represents both an opportunity for differentiated pivot toward scalable asset management fees but carries significant near-term execution complexity amplified by financing challenges within current macroeconomic conditions. Historical financial volatility combined with tightening liquidity underscores substantial operational risk ahead amid structural changes requiring adept capital management and disciplined asset rotation strategies. Market attention should center on how rapidly Medalist can grow fee-bearing DST AUM without sacrificing remaining legacy portfolio value while navigating evolving debt constraints caused by creditor protective measures amidst elevated interest rate dynamics.

This analysis is intended solely for informational purposes based on public filings and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments