Mobile-health Network Solutions' Turnaround Efforts in Telehealth and AI Infrastructure Expansion

MNDR strives to overcome recurring losses by enhancing its telemedicine platform and pursuing AI data center acquisitions.

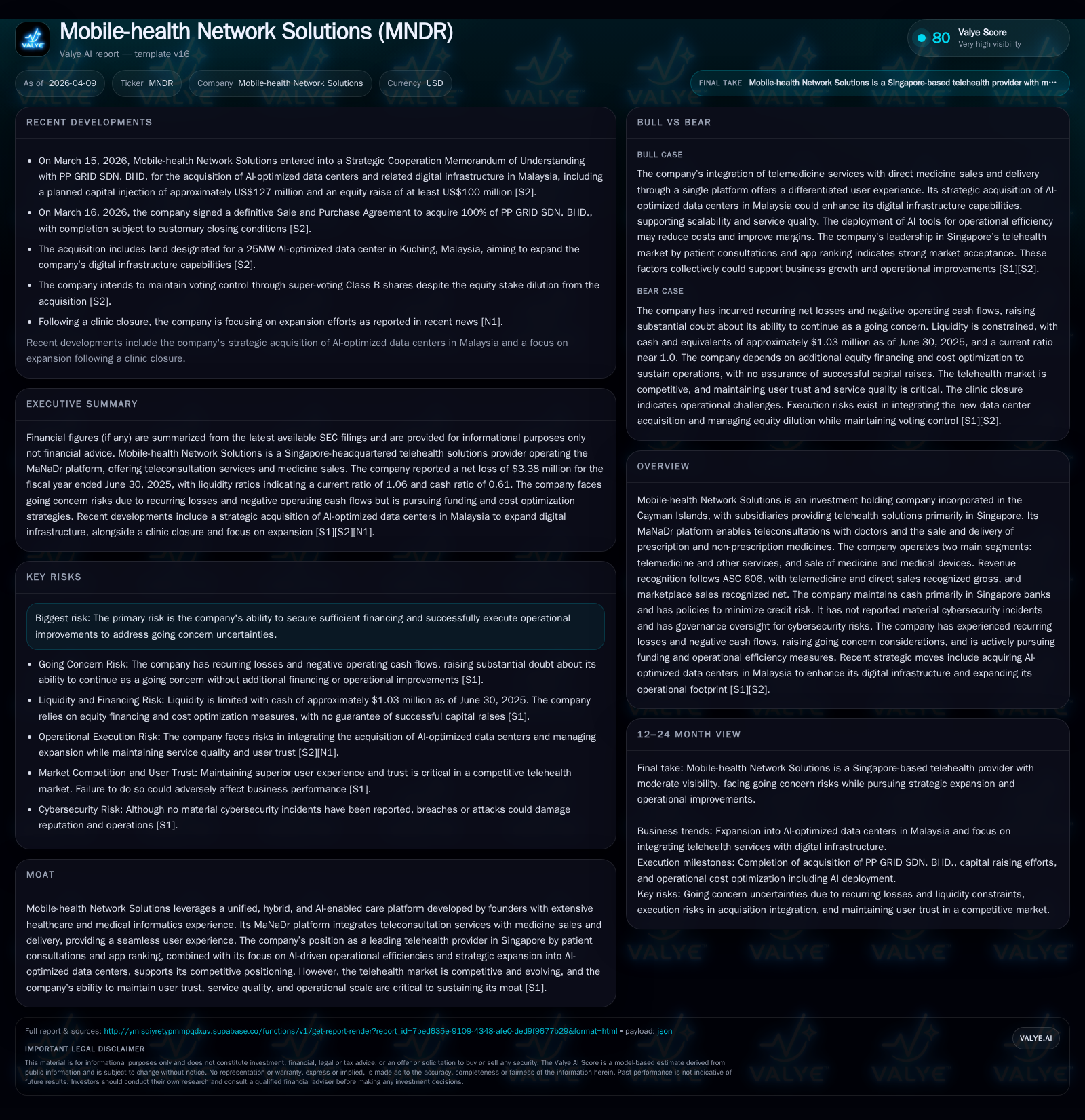

Mobile-health Network Solutions has faced significant revenue volatility and continued operating losses while maintaining a leading position in Singapore’s telehealth market. After a revenue surge in FY2024 followed by a steep decline in FY2025, MNDR is shifting strategic focus toward AI-optimized data centers through a major acquisition and capital injection, aiming to support platform scalability and operational efficiency. Liquidity remains tight with ongoing going concern risks, prompting active financing efforts alongside cost optimization and technology investments.

Financial Trends and Performance Drivers: Historical Overview

Mobile-health Network Solutions (MNDR) experienced volatile financial performance from FY2023 through FY2025 influenced by telehealth demand fluctuations and marketplace dynamics within Singapore's telehealth sector. Revenue increased sharply by 77.4% to approximately $13.97 million in FY2024 before declining 45.3% to $7.65 million in FY2025 [F1]. This pattern aligns with the company's disclosure of differing revenue recognition methods under ASC 606 — gross recognition for telemedicine and direct sales versus net recognition for marketplace transactions — impacting top-line comparability across years [S1].

Despite lower revenues in FY2025, MNDR reduced its net loss substantially by 78.3%, from -$15.6 million to -$3.38 million, driven by aggressive cost containment measures including a 61.2% reduction in salary expenses and a 45.8% decrease in selling, general & administrative expenses (SG&A). Gross profit declined proportionally (-49.6%) yet remained positive at $1.28 million [F1][S1]. Operating cash flow remained negative at -$4.36 million but improved by nearly 32% year-over-year, while capital expenditures halved to just over $63K reflecting prudent liquidity management [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -3 | -4 | 63140 | +78.3% |

| 2024 | -16 | -6 | 134211 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | -4 | -129.3 |

| 2024 | 7 | -7 | -376.9 |

Source: SEC companyfacts cache [F1].

*Note: Net income for FY2024 repeated due to formatting.

Revenue Recognition Nuances: Telemedicine vs Marketplace Segments

MNDR operates two primary segments: "Telemedicine and other services" and "Sale of medicine and medical devices." Under ASC 606 revenue recognition standards detailed in filings [S1][S10][S15], revenues from direct teleconsultations and medicine sales are recognized on a gross basis reflecting full transaction amounts before third-party costs are deducted. In contrast, marketplace transactions where MNDR facilitates third-party services or product sales are recognized net of amounts paid out to service providers.

This dual recognition framework results in differing margin profiles: direct telemedicine sales typically yield higher gross margins but may entail greater upfront costs related to clinical staffing or platform investment; marketplace revenues offer scalable volume growth but lower margins due to pass-through arrangements.

The MaNaDr platform integrates these segments with AI-enabled enhancements aimed at improving operational efficiency and user experience — critical factors underpinning user trust amid competitive pressures [S1]. Expanded offerings including prescription medicines contribute to customer retention though monetization remains sensitive to pricing constraints and regulatory developments.

Operational Challenges: Cost Management Amid Market Pressures

Cost discipline has been central to MNDR's partial turnaround amid high labor costs for healthcare professionals and skilled tech staff within Singapore’s competitive labor market [S1]. The company’s marked SG&A reductions contrast with necessary investments into AI tools intended to optimize operations while limiting reliance on costly human resources.

Salary expenses fell over 60%, potentially reflecting restructuring following recent clinic closures [N1] but must be balanced carefully against maintaining service quality and cybersecurity commitments—no material incidents reported but ongoing board-level oversight maintained [S1]. Technological infrastructure upgrades remain vital for sustaining customer loyalty and capacity scaling.

Strategic Expansion: Acquisition of AI-Optimized Data Centers

In March 2026 MNDR entered definitive agreements to acquire PP GRID SDN BHD (PPG), operator of two AI-optimized data centers in Malaysia supporting expansion of the MaNaDr platform [S2]. The transaction involves approximately MYR500 million (~US$127 million) capital injection led by PPG’s sole shareholder receiving a controlling equity stake (65%), while MNDR’s founders maintain voting control via super-voting Class B shares.

This acquisition aims to strengthen backend infrastructure facilitating scalable AI-driven care capabilities such as personalized algorithms and predictive logistics—key competitive advantages outlined by management [S2][S1]. Regional digital infrastructure presence also supports geographic diversification beyond Singapore with potential cost synergies through proprietary hosting.

Completion depends on customary closing conditions including land use rights transfer for a proposed Kuching site designated for a new 25MW facility—highlighting execution risks balanced against transformative growth potential.

Balance Sheet Snapshot & Going Concern Considerations

As of June 30, 2025 MNDR reported current assets slightly exceeding current liabilities resulting in a modest current ratio near 1.06—a narrow liquidity cushion indicating tight working capital management [F1][S29]. Cash totaled approximately $1.03 million compared with prior periods showing partial improvement yet insufficient for sustained self-funding.

Long-term liabilities include amounts due officers plus growing lease obligations related to facilities or equipment leases [S3]. The auditor’s report includes an explanatory paragraph expressing substantial doubt about MNDR's ability to continue as a going concern given recurring losses (-$3.38 million net income), persistent negative operating cash flow (-$4.36 million), and pressing needs for additional financing initiatives [S1][F1].

Management is actively pursuing equity raises through At-the-Market offerings plus private placements while advancing cost reduction strategies—crucial yet uncertain measures.

Currency risk arises as operations primarily transact in SGD while reporting currency is USD; most cash held locally benefits from deposit insurance coverage up to S$100K mitigating concentration risk associated with local banks [S15][S19].

Capital Allocation History & Shareholder Returns

MNDR has not paid dividends consistent with ongoing losses but conducted share repurchases totaling US$6.6 million completed by FY2023 under buyback programs aimed at managing equity base size strategically without improving free cash flow given persistent negative cash generation profiles [F1][S23].

Capital expenditures were curtailed sharply from about US$134K in FY2024 down to just over US$63K in FY2025—reflecting cautious investment amid liquidity constraints potentially deferring broader technology initiatives except those related to acquisition commitments underway [F1].

Future capital decisions will likely prioritize infrastructure scale-up via newly acquired data centers alongside selective innovation within core platforms.

Outlook & Key Milestones Ahead

Investors should monitor:

- Completion status of PPG acquisition including regulatory approvals relating to Malaysian land use rights for planned data center projects [S2]

- Progress toward independently raising at least US$100 million critical for financing acquisition plus organic growth funding needs [S2]

- User engagement trends following recent clinic network closures indicating demand resilience or vulnerabilities amid regional competition dynamics [N1]

- Quarterly operational updates focusing on cash flow improvements or margin enhancements linked to AI infrastructure integration efficiencies [N1][S3]

- Ongoing foreign exchange impact given SGD/USD exposure coupled with Singapore-centric operations influencing reported earnings volatility risk profile [S15]

Cybersecurity governance remains essential as management emphasizes continuous oversight ensuring platform reliability which underpins user trust crucial for sustainable growth trajectories.[S1]

This analysis is based solely on publicly available SEC filings and recent disclosures without offering investment advice or price forecasts. Readers should consider inherent risks related to MNDR's turnaround execution including capital raising success amid competitive healthcare markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments